Every morning, sunlight falls with equal generosity on the salt deserts of Gujarat and the sprawling industrial parks of Jiangsu. Photons do not recognise borders. Under standard test conditions, the sun delivers nearly the same intensity of energy to every nation. Nature, it would seem, is perfectly democratic.

Industry, however, is not.

Over the past two decades, one country has succeeded in transforming this universally available resource into a formidable industrial engine. China did not merely embrace solar energy; it built an entire manufacturing ecosystem around it. From polysilicon and wafers to solar cells, modules and manufacturing equipment, the country systematically integrated every layer of the value chain, eventually emerging as the undisputed factory of the global energy transition.

Today, according to the International Energy Agency (IEA), China dominates more than 80 per cent of global solar manufacturing capacity across most stages of the supply chain, while accounting for over 95 per cent of global wafer production and a significant majority of polysilicon output. In many ways, the world’s solar revolution has been manufactured in China.

India’s journey has followed a different path.

For much of the last decade, India emerged as one of the world’s fastest-growing solar markets, prioritising deployment over manufacturing. Gigawatt-scale solar parks transformed landscapes across Rajasthan, Gujarat and Karnataka, while ambitious policy interventions positioned renewable energy at the centre of the country’s energy strategy. As of 31 May 2026, India’s cumulative installed solar capacity stood at 157.05 GW, according to the Ministry of New and Renewable Energy (MNRE), making the country one of the world’s leading solar markets.

Yet, beneath these impressive deployment figures lies a more complex industrial reality.

India may have become a global success story in solar adoption, but manufacturing leadership remains a work in progress. Domestic module manufacturing capacity under the Approved List of Models and Manufacturers (ALMM) has expanded to nearly 194 GW, while domestic solar cell manufacturing capacity stands at around 31 GW, exposing a significant mismatch between module assembly capability and core component availability.

As nations race to decarbonise their economies, a new geopolitical contest is unfolding—one that is not merely about generating clean electricity, but about controlling the industrial architecture that powers the energy transition. For India, which is targeting 500 GW of non-fossil fuel capacity by 2030, building a resilient domestic manufacturing ecosystem is no longer optional.

The question, therefore, is no longer whether India can install enough solar capacity.

The more consequential question is this:

Can India transform itself from one of the world’s largest consumers of solar technology into one of its most influential manufacturers?

The answer will determine not only the future of India’s solar industry, but also the country’s industrial competitiveness, energy security and strategic autonomy in an increasingly electrified world.

Two Nations, One Sun, Different Outcomes

| Indicator (2026) | India | China |

| Cumulative Installed Solar Capacity | 157.05 GW | 1,080+ GW |

| Annual Solar Module Manufacturing Capacity | ~194 GW | >1,000 GW |

| Solar Cell Manufacturing Capacity | ~31 GW | ~850 GW+ |

| Wafer Manufacturing Capacity | Nascent | >95% Global Share |

| Global Solar Manufacturing Share | Emerging Hub | Dominant Global Leader |

Sources: MNRE, IEA, industry estimates, ALMM updates, BloombergNEF, JMK Research.

The 20-Year Head Start

- 2005: China begins large-scale investments in solar manufacturing, supported by aggressive industrial policies and export-led growth.

- 2010: Chinese manufacturers rapidly expand across the value chain, building integrated manufacturing ecosystems and achieving significant economies of scale.

- 2015: China establishes dominance in upstream segments, particularly wafers and polysilicon, while global competitors struggle to match pricing and scale.

- 2020: India intensifies efforts towards manufacturing self-reliance through initiatives such as Atmanirbhar Bharat, Production Linked Incentive (PLI) schemes and import duty measures.

- 2026: India emerges as one of the fastest-growing solar manufacturing destinations globally, but continues to face challenges in upstream integration and supply-chain localisation.

This timeline reveals a crucial truth: India’s challenge is not merely catching up with today’s China. It is attempting to bridge a manufacturing gap created by nearly two decades of sustained industrial policy, ecosystem development and technological leadership.

This is precisely why the race, though unequal, has only just begun.

PLI: India’s Manufacturing Catalyst

India’s attempt to bridge the manufacturing gap with China is being driven by one of the country’s most ambitious industrial interventions—the Production Linked Incentive (PLI) Scheme for High Efficiency Solar PV Modules.

Launched in phases with a cumulative outlay of ₹24,000 crore, the scheme seeks to create an integrated domestic manufacturing ecosystem spanning polysilicon, wafers, cells and modules. Unlike earlier incentives focused primarily on module assembly, the PLI programme rewards deeper backward integration and the adoption of high-efficiency technologies.

Under the two tranches of the scheme, companies such as Reliance Industries, Waaree Energies, Tata Power Solar, Adani Infrastructure, Indosol Solar, Avaada Electro, ReNew, JSW Neo Energy and Grew Energy have secured allocations to establish large integrated manufacturing facilities across the country.

According to MNRE, the scheme is expected to support the creation of nearly 48 GW of fully or partially integrated solar manufacturing capacity, significantly strengthening India’s domestic supply chain and reducing import dependence in critical upstream segments.

While execution remains the next major challenge, the PLI programme has already altered industry sentiment. It has accelerated investments, encouraged vertical integration and signalled India’s intent to evolve from a solar deployment market into a globally competitive manufacturing destination.

For many industry observers, the PLI scheme may ultimately be remembered as the policy intervention that marked the beginning of India’s solar manufacturing era.

THE STRUCTURAL CHASM: Overbuilding the Shell, Missing the Core

For years, India’s solar success story has been measured in gigawatts installed. More recently, it has also been measured in gigawatts manufactured. Factory announcements, expansion plans and production-linked incentives have collectively transformed the country into one of the world’s fastest-growing solar manufacturing destinations.

At first glance, the numbers appear impressive.

According to the latest update of the Ministry of New and Renewable Energy’s (MNRE) Approved List of Models and Manufacturers (ALMM) List-I, India’s enlisted solar module manufacturing capacity has surged to 193.89 GW as of May 2026. Just five years ago, the country had less than 20 GW of ALMM-listed module capacity.

The rapid expansion reflects both investor confidence and the government’s determined push towards self-reliance in renewable energy manufacturing.

However, beneath this remarkable growth story lies a structural imbalance that could define the next phase of India’s solar journey.

India has become exceptionally good at building the outer shell of the solar value chain—the module. The challenge lies in manufacturing its heart.

Modules vs Cells: The Great Imbalance

While India’s ALMM-listed module manufacturing capacity stands at nearly 194 GW, domestic solar cell manufacturing capacity remains significantly lower at around 31.14 GW. In simple terms, the country possesses module manufacturing capacity that is more than six times larger than its cell manufacturing capability.

The imbalance becomes even more pronounced when internal industry dynamics are considered. Industry estimates suggest that nearly 28.58 GW of India’s total cell capacity is earmarked for captive consumption by vertically integrated manufacturers, leaving only about 2.56 GW available in the open market for standalone module manufacturers.

This mismatch has emerged as a major challenge following the implementation of ALMM List-II on June 1, 2026, which mandates the use of domestically manufactured and approved solar cells in a large segment of government-backed and subsidised projects. While the policy is expected to strengthen domestic manufacturing, it has simultaneously exposed the sector’s most critical bottleneck—the limited availability of domestic cells.

Industry bodies have warned that immediate enforcement, without adequate domestic cell supply, could lead to shortages, higher module prices and project delays, while also risking stranded investments for standalone manufacturers.

The challenge, however, is not merely quantitative—it is also technological. India’s module ecosystem has rapidly shifted towards TOPCon technology, yet domestic production of advanced TOPCon cells continues to lag demand.

The result is a paradox: India has mastered module assembly, but its manufacturing core remains under construction.

The Technology Trap

India’s solar manufacturing story is no longer merely a race of scale; it is increasingly becoming a race of technology. As manufacturers rapidly expand capacities, they are also confronting a critical challenge—ensuring that today’s investments do not become tomorrow’s stranded assets.

The domestic market has already pivoted decisively towards n-type TOPCon (Tunnel Oxide Passivated Contact) technology, now considered the industry benchmark due to its higher efficiencies, lower degradation rates and compatibility with existing manufacturing lines. According to industry estimates, nearly 172 GW of India’s approved module manufacturing capacity is based on TOPCon technology. However, domestic TOPCon cell manufacturing capacity stands at only around 9.6 GW, exposing a significant technology mismatch.

Yet, TOPCon itself may only be an intermediate step. Globally, manufacturers are increasingly investing in next-generation technologies such as HJT, Back Contact (BC) and perovskite-silicon tandem cells, the latter demonstrating laboratory efficiencies exceeding 30 per cent.

For Indian manufacturers, the challenge is not merely catching up—but staying ahead of an evolving technology curve.

Where does India genuinely compete with China today—and where does the gap remain largest?

Avinash Hiranandani, Vice Chairman & Managing Director, RenewSys India Private Limited, said, “India has made remarkable progress over the last decade. We are no longer just an installation market; we are building a credible manufacturing ecosystem across modules, cells and critical components. Indian manufacturers have demonstrated that they can produce world-class products meeting global quality and reliability standards.

Where we compete effectively today is in engineering capability, product quality, process excellence, and increasingly in manufacturing scale. India also benefits from a strong domestic market, a skilled engineering workforce, and a policy environment that is encouraging local manufacturing.

However, the largest gap remains upstream. China has spent more than two decades building an integrated ecosystem that spans polysilicon, ingots, wafers, equipment manufacturing, specialty chemicals and advanced materials. These industries create significant cost efficiencies and supply-chain resilience. India has begun this journey, but developing these upstream capabilities will require sustained investment, technology partnerships, and long-term policy support.

Ultimately, manufacturing leadership is not determined by one factory or one company—it is built through a complete industrial ecosystem.”

India’s Climb vs China’s Terawatt Monopoly

For all the momentum surrounding India’s solar manufacturing ambitions, a simple comparison with China reveals the scale of the challenge ahead.

Over the past two decades, China has systematically built an industrial ecosystem that spans every stage of the solar value chain—from raw materials and manufacturing equipment to finished modules and exports. India, by contrast, is still in the early stages of developing a deeply integrated manufacturing base.

The result is an industrial asymmetry that extends far beyond gigawatts.

India vs China: The Solar Manufacturing Reality (2026)

| Manufacturing Stage | India | China | Strategic Dependency |

| Solar Modules | ~193.89 GW ALMM-listed capacity | >1,000 GW manufacturing capacity | India is increasingly self-sufficient in module assembly and is emerging as an export hub. |

| Solar Cells | ~31.14 GW approved capacity | ~850 GW+ capacity | Significant domestic shortfall; ALMM List-II implementation is testing supply availability. |

| Wafers | Nascent / Limited capacity | ~96.6% of global production | India remains heavily dependent on imported wafers. |

| Polysilicon | Very limited commercial capacity | ~93.2% of global production | The deepest manufacturing gap and the foundation of China’s dominance. |

| Manufacturing Equipment | Largely imported | Global manufacturing leader | India remains dependent on imported production lines and critical process equipment. |

Manufacturing Equipment Largely imported Global manufacturing leader India remains dependent on imported production lines and critical process equipment.

The numbers tell an important story. India has successfully built scale in module manufacturing, but the country’s presence becomes progressively weaker as one moves upstream. China, meanwhile, has consolidated dominance precisely in these upstream segments, allowing it to capture a disproportionate share of the industry’s economic value.

Where Does Every Rupee Go?

For years, India has celebrated solar deployment milestones. Yet, in manufacturing, the more important question may be: Who captures the value behind every solar project?

A typical utility-scale solar project can be visualised as a value chain rather than a single product.

The highest value addition and technological intensity reside in the upstream stages—particularly polysilicon, wafers and advanced cell manufacturing. These are also the segments overwhelmingly dominated by China. According to the International Energy Agency (IEA), China controls more than 80 per cent of global manufacturing capacity across most stages of the solar supply chain, with its share in polysilicon, ingots and wafers approaching 95 per cent.

India, on the other hand, has built significant strengths in module assembly, project development, engineering, procurement and construction (EPC), and increasingly, system integration. However, a large portion of the value embedded in upstream materials and components continues to accrue outside the country.

In other words, while India is deploying solar at scale, a substantial share of the industrial value chain still resides elsewhere.

This distinction matters because manufacturing leadership is not merely about producing more panels. It is about capturing more value.

The Cost Equation: Why China Still Wins on Price

China’s dominance in solar manufacturing is not simply the result of lower labour costs. It is the outcome of a deeply integrated industrial ecosystem built over two decades.

- First, scale matters. Chinese manufacturers operate giga-scale facilities that significantly reduce per-unit production costs through economies of scale. Many individual Chinese companies today possess capacities larger than the entire manufacturing base of several countries.

- Second, China benefits from vertical integration. Manufacturers often control the entire value chain—from polysilicon and wafers to cells and modules—allowing them to optimise costs, minimise supply disruptions and improve margins.

- Third, low-cost financing and robust infrastructure have historically supported rapid expansion. Preferential credit access, efficient logistics networks and manufacturing clusters further enhance competitiveness.

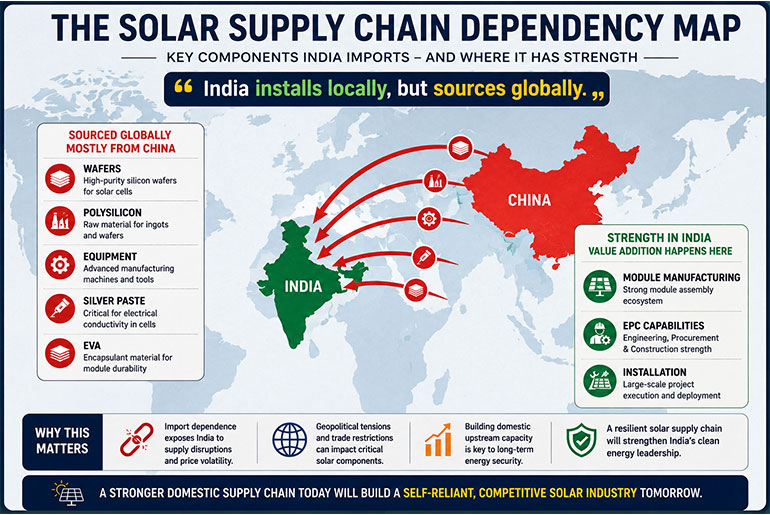

Finally, the proximity of suppliers producing glass, EVA, silver paste, backsheets and equipment creates powerful ecosystem efficiencies.

India has made significant progress in module manufacturing, but narrowing the cost gap will require not just more factories, but a deeper, integrated manufacturing ecosystem.

The Missing Pieces in India’s Solar Puzzle

India’s solar ambitions are increasingly constrained not by demand, but by industrial depth.

The Wafer Gap

If solar modules are the face of the industry, wafers are its hidden foundation.

Today, India remains overwhelmingly dependent on imported wafers, with domestic manufacturing capacity still at a nascent stage. China, by contrast, accounted for nearly 96.6 per cent of global wafer production in 2024, making it the undisputed leader in one of the most critical segments of the solar value chain.

The absence of large-scale domestic wafer manufacturing creates vulnerabilities ranging from supply disruptions to price volatility.

The Polysilicon Challenge

Polysilicon sits at the very root of the solar manufacturing pyramid.

However, producing solar-grade polysilicon is highly capital-intensive, energy-intensive and technologically demanding. While India is beginning to witness early investments in this segment, commercial-scale capacities remain limited. China currently produces more than 93 per cent of the world’s polysilicon, underscoring the enormity of the challenge facing new entrants.

Dependence on Manufacturing Equipment

Even when Indian companies establish manufacturing facilities, much of the production equipment—including cell lines, wafering tools, metallisation equipment and automation systems—is imported, primarily from China.

This means that manufacturing self-reliance and equipment self-reliance are not necessarily the same.

The Materials Ecosystem Deficit

A globally competitive solar industry requires far more than cells and modules.

Critical inputs such as:

• Silver paste

• EVA encapsulants

• Solar glass

• Backsheets

• Junction boxes

• Speciality chemicals

continue to witness varying degrees of import dependence.

China’s advantage lies not merely in scale, but in the existence of a tightly integrated industrial ecosystem where suppliers, manufacturers, equipment providers and logistics networks operate in close proximity.

The Capital Question

Solar manufacturing is among the most capital-intensive industries in the clean energy sector.

A fully integrated manufacturing ecosystem spanning polysilicon to modules demands billions of dollars in investments, long gestation periods and policy certainty extending well beyond electoral cycles.

India’s challenge, therefore, is not simply to build factories.

It is to build an ecosystem.

India’s Emerging Champions: Building the Foundations of Manufacturing Leadership

India’s solar manufacturing ambitions are no longer confined to policy announcements. Across the country, a new generation of manufacturers is steadily expanding capacities, investing in advanced technologies and deepening integration across the value chain.

Companies such as Waaree Energies, Premier Energies and Vikram Solar have emerged as major module manufacturers, while simultaneously scaling domestic cell production and strengthening their global market presence. RenewSys, India’s first integrated manufacturer of solar PV modules and key components, has played a pioneering role in localising critical parts of the value chain, including encapsulants and backsheets.

Meanwhile, Adani Solar is pursuing large-scale vertical integration spanning cells and modules, while Tata Power Solar, one of the country’s oldest solar manufacturers, continues to expand its integrated manufacturing capabilities alongside utility-scale project execution.

Together, these companies represent more than individual corporate success stories. They signify the early contours of an ecosystem that could underpin India’s transition from a major solar market to a globally competitive manufacturing hub.

What lessons from China’s manufacturing journey can India realistically adopt?

Avinash Hiranandani, Vice Chairman & Managing Director, RenewSys India Private Limited, said, “China’s biggest success was not simply lower manufacturing costs—it was consistency of industrial policy and ecosystem development. Investments were made across the entire value chain rather than focusing only on finished products.

India can certainly adopt that approach while building its own strengths. Long-term policy stability is essential because manufacturing investments have horizons of ten to twenty years. Infrastructure, logistics, research institutions, equipment manufacturing, and supplier development all need to evolve together.

Equally important is a relentless focus on productivity and continuous technology upgrades. Solar manufacturing is an industry where technology evolves rapidly, and companies must constantly invest in efficiency improvements.

India does not need to replicate China; it needs to build a manufacturing model suited to its own strengths, leveraging its engineering talent, innovation capabilities, and growing domestic demand.”

THE REGULATORY CRUCIBLE

ALMM: Catalyst or Constraint?

India’s solar manufacturing ambitions are being shaped not only on factory floors, but also in policy corridors. At the centre of this transformation lies the Approved List of Models and Manufacturers (ALMM) framework—arguably the most significant industrial policy intervention in India’s solar sector since the launch of the National Solar Mission.

For policymakers, ALMM is a strategic tool to reduce import dependence, ensure quality and strengthen domestic manufacturing. For industry, however, it has triggered a critical debate: Can localisation mandates move faster than the ecosystem itself?

Decoding ALMM List-I and List-II

Introduced by the Ministry of New and Renewable Energy (MNRE), the ALMM framework comprises two pillars. List-I, notified in March 2021, covers approved solar PV modules and mandates their use in government-backed and subsidised schemes, including PM Surya Ghar, with the objective of ensuring quality, traceability and domestic manufacturing.

The more disruptive ALMM List-II covers solar PV cells. Although the first list of approved cell manufacturers was issued in July 2025, mandatory use of ALMM-listed domestic cells came into effect on June 1, 2026, requiring eligible projects to procure approved domestically manufactured cells.

The policy signal is clear: India intends to move beyond module assembly and deepen localisation across the value chain.

Policy Meets Market Reality

Yet, policy ambition and market preparedness are not always aligned.

As of May 2026, India’s ALMM-listed module manufacturing capacity stood at nearly 193.9 GW, while domestic cell capacity remained at only about 31 GW. Industry bodies have repeatedly warned that immediate implementation of ALMM List-II could create supply shortages, increase costs and delay project execution, particularly for standalone module manufacturers reliant on open-market procurement.

With a large share of domestic cell output consumed by vertically integrated players, concerns over stranded investments and market concentration have intensified. Despite these concerns, MNRE has maintained that there will be no blanket extension beyond the June 1 deadline.

The friction highlights a broader reality: localisation is not merely a regulatory exercise—it is an ecosystem challenge.

The Cost of Not Manufacturing

India may well achieve its target of 500 GW of non-fossil fuel capacity by 2030. But what happens if upstream components continue to be imported?

Dependence on imported wafers, polysilicon and critical manufacturing equipment exposes the country to supply disruptions, geopolitical tensions, price volatility and trade disputes. Recent frictions, including China’s challenge to India’s solar tariffs at the World Trade Organization (WTO), underscore how closely industrial policy and energy security are intertwined.

In the clean energy era, energy security and manufacturing security are increasingly inseparable.

LESSONS FROM THE DRAGON

What India Can Learn from China’s Rise

China’s rise as the world’s undisputed solar manufacturing powerhouse was neither accidental nor instantaneous. It was the outcome of nearly two decades of deliberate industrial planning, sustained policy support, massive capital deployment and relentless scale expansion. While India cannot—and perhaps should not—replicate the Chinese model in its entirety, there are valuable lessons embedded within China’s journey.

The objective is not imitation.

It is intelligent adaptation.

Lesson 1: Industrial Policy Must Outlast Political Cycles

China’s solar success has been underpinned by long-term policy consistency, sustained financial support and robust infrastructure development. Such stability enabled manufacturers to invest confidently across the value chain. India has taken significant steps through the PLI scheme, BCD, ALMM and Atmanirbhar Bharat, but the industry still seeks greater long-term policy visibility. In manufacturing, certainty itself is a powerful competitive advantage.

Lesson 2: Manufacturing Must Grow Alongside the Market

China did not wait for domestic demand to mature before building manufacturing capacity; it expanded both simultaneously. India, by contrast, first emerged as a major solar deployment market, crossing 157 GW of installed solar capacity by May 2026, while manufacturing depth—particularly in upstream segments—remains uneven. The next phase of India’s solar journey must ensure that deployment and manufacturing grow in parallel, with gigawatts installed increasingly matched by gigawatts manufactured.

Lesson 3: In Solar Manufacturing, Scale Wins

The solar industry is fundamentally a scale business. China’s manufacturers invested aggressively in giga-scale facilities, enabling lower costs, process efficiencies and global competitiveness. Today, some Chinese companies individually operate capacities larger than the manufacturing base of entire countries. While India’s ALMM-listed module capacity is approaching 194 GW, long-term competitiveness will require scale not only in modules, but also across wafers, cells, ancillary materials and equipment. Building large, technologically advanced manufacturing clusters will therefore be critical.

Lesson 4: Vertical Integration Creates Resilience

China’s dominance extends far beyond module manufacturing because it controls almost every stage of the solar value chain—from polysilicon and ingots to wafers, cells and finished modules. This vertical integration enables lower costs, stronger supply-chain resilience, faster technology transitions and improved competitiveness. India’s manufacturing ecosystem, by contrast, remains strongest at the module assembly stage, while significant dependence persists in wafers, polysilicon and manufacturing equipment. Bridging these upstream gaps will be critical to India’s long-term manufacturing competitiveness.

Lesson 5: Global Leadership Requires an Export Mindset

China’s solar industry was built not only for domestic consumption but also for global markets.

Export orientation enabled Chinese companies to achieve economies of scale, continuously improve product quality and diversify revenue streams.

As trade patterns shift and global supply chains seek diversification beyond China, India has an opportunity to position itself as an alternative manufacturing destination.

However, achieving this ambition will require globally competitive costs, advanced technologies, stringent quality standards and strong trade partnerships.

The future may belong not merely to manufacturers serving India, but to manufacturers serving the world from India.

What India Must Avoid

Learning from China does not mean replicating every aspect of its journey.

India possesses distinct economic, demographic and resource realities that demand a uniquely Indian manufacturing strategy.

Avoid Resource-Intensive Growth at Any Cost

Solar manufacturing expansion must remain aligned with resource efficiency, particularly in water and energy consumption.

Build a Circular Economy from the Start

Unlike earlier manufacturing revolutions, India has the opportunity to integrate recycling, material recovery and end-of-life management into the solar ecosystem from the outset.

Do Not Separate Solar from Storage

The future of renewable energy will increasingly depend on integrated solar-plus-storage systems rather than standalone generation assets.

Invest in Innovation, Not Just Capacity

Long-term competitiveness will require domestic research and development capabilities in advanced cell architectures, materials and manufacturing technologies.

The lesson is clear: India should not seek to become another China.

It should seek to become the world’s first truly sustainable, resilient and future-ready solar manufacturing ecosystem.

If you were advising policymakers, what three interventions would most accelerate India’s rise as a global solar manufacturing hub?

Avinash Hiranandani, Vice Chairman & Managing Director, RenewSys India Private Limited, said, “India has already demonstrated that it can manufacture world-class solar products. The next phase of growth, however, requires strengthening the entire manufacturing ecosystem. Developing upstream capabilities in wafers, polysilicon, solar glass, specialty chemicals, and equipment will be essential to reduce import dependence and build long-term resilience.

Equally important is improving logistics infrastructure. High logistics costs impact global competitiveness, so investments in efficient ports, multimodal transport, and faster movement of goods can significantly enhance India’s manufacturing advantage.

Finally, sustained investment in innovation and skill development will be critical. As manufacturing becomes increasingly technology-driven, India’s ability to foster indigenous R&D and build a highly skilled workforce will determine its long-term leadership in the global solar industry.”

THE DECADE OF DECISION

India’s Solar Future Will Be Decided Now

For all the debates surrounding tariffs, manufacturing capacities and localisation mandates, India’s solar story is ultimately about choices.

The country stands at a historic inflection point. Over the next decade, decisions taken by policymakers, manufacturers, investors and utilities will determine whether India emerges merely as one of the world’s largest consumers of solar technology—or as one of its most influential producers.

The future is not preordained.

It will be manufactured.

Three Possible Futures for India’s Solar Industry

Scenario 1: The Import Nation

In this future, India successfully achieves its renewable energy targets, crossing 500 GW of non-fossil fuel capacity and emerging as one of the world’s largest clean energy markets. Solar installations continue to grow and electricity generation becomes progressively cleaner.

However, manufacturing depth remains limited. While modules are increasingly assembled domestically, critical upstream segments—including polysilicon, wafers, advanced cells and manufacturing equipment—continue to be import dependent. Global supply-chain disruptions, geopolitical tensions and trade disputes therefore continue to expose the sector to uncertainty.

India wins the deployment race, but captures only a fraction of the industrial value.

Scenario 2: The Regional Manufacturing Hub

In this scenario, India builds a strong manufacturing base across modules and cells while gradually expanding into upstream segments. Stable policies, manufacturing clusters and a maturing ancillary ecosystem strengthen competitiveness.

India not only meets domestic demand but also supplies markets across South Asia, the Middle East and Africa, emerging as a credible alternative manufacturing destination in an increasingly diversified global supply chain.

India becomes not merely a market, but a manufacturing hub.

Scenario 3: The Global Solar Superpower

The most ambitious scenario envisions India establishing a fully integrated ecosystem spanning polysilicon, wafers, cells, modules, storage systems and next-generation technologies.

Leveraging its vast domestic market, engineering talent and policy support, India evolves into a globally competitive exporter of solar technologies. Domestic R&D flourishes, companies become technology innovators and solar manufacturing emerges as a strategic pillar of the Indian economy.

The gap with China narrows—not overnight, but steadily.

Solar Without Storage Is No Longer Enough

The next phase of India’s energy transition will not be defined by solar capacity alone.

It will be defined by dispatchability.

As renewable penetration rises, intermittency will increasingly challenge grid operators. Midday solar surpluses and evening demand peaks are already reshaping electricity markets across the world.

The solution lies in integrating generation with storage.

The New Renewable Energy Equation

Solar Generation

↓

Battery Energy Storage Systems (BESS)

↓

Dispatchable Renewable Power

↓

Grid Stability & Flexibility

↓

24×7 Clean Energy

The Ministry of Power has already recognised this shift through ambitious Battery Energy Storage System (BESS) programmes and viability gap funding mechanisms. Industry projections suggest that India’s storage market could witness exponential growth over the coming decade as utilities increasingly seek round-the-clock renewable power solutions.

In many ways, the future of solar manufacturing and the future of energy storage are becoming inseparable.

The countries that master both may well define the next era of the global energy transition.

What Must Happen Next?

For Government

✔ Ensure long-term policy certainty and regulatory stability.

✔ Expand incentives beyond modules to upstream segments such as polysilicon, ingots and wafers.

✔ Accelerate the development of integrated manufacturing clusters and supporting infrastructure.

✔ Strengthen domestic R&D ecosystems and industry-academia collaboration.

For Industry

✔ Pursue greater vertical integration across the value chain.

✔ Invest aggressively in next-generation technologies, including HJT, BC and tandem cells.

✔ Build resilient domestic supply chains for critical materials and components.

✔ Develop export competitiveness alongside domestic market leadership.

For Investors

✔ Look beyond module assembly and fund upstream manufacturing opportunities.

✔ Support emerging segments including manufacturing equipment, advanced materials and recycling.

✔ Recognise solar manufacturing as a long-term strategic industry rather than a short-cycle investment opportunity.

For Utilities and Grid Operators

✔ Prepare grids for high renewable penetration.

✔ Accelerate the deployment of battery energy storage systems and flexible grid infrastructure.

✔ Transition from energy procurement models to reliability-centric planning frameworks.

Can India Challenge China?

India is unlikely to displace China as the world’s dominant solar manufacturing powerhouse in the foreseeable future. China’s leadership rests on nearly two decades of sustained industrial policy, deep vertical integration and unmatched scale across the entire value chain.

However, India does not need to replace China to succeed.

The more realistic and strategically important opportunity lies in establishing itself as the world’s second major solar manufacturing hub—one capable of serving domestic demand while diversifying global supply chains. With a rapidly expanding market, strong policy support, growing investments and an increasingly mature manufacturing ecosystem, India possesses many of the ingredients required for long-term success.

Ultimately, the benchmark for India should not be replacing China, but reducing strategic dependence on it while building a globally competitive, resilient and self-reliant solar manufacturing ecosystem.

The Final Word

The real question is not whether India can install enough solar capacity.

The real question is whether India can capture the industrial value behind every solar panel it deploys.

The sunlight is already here.

The market is already here.

The policy momentum is already building.

What remains uncertain is whether India can convert these advantages into enduring manufacturing leadership.

The next decade will determine whether India merely consumes the energy transition—or manufactures it.