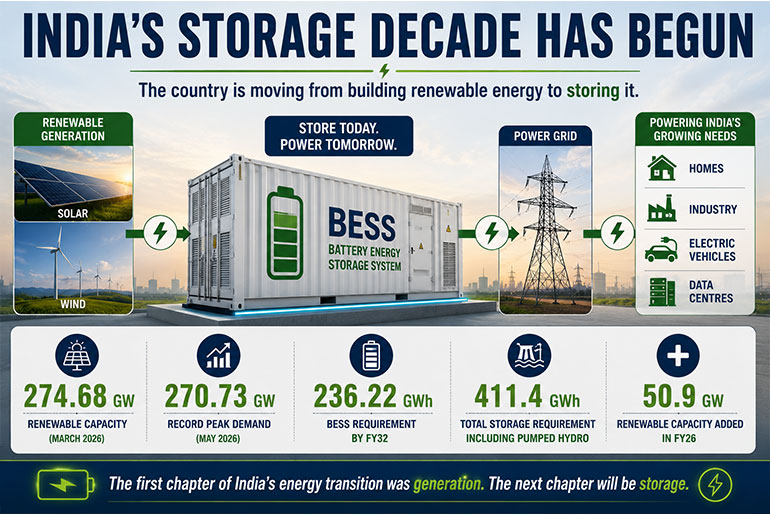

At 7:30 PM on a summer evening, India’s solar power miracle begins to disappear. Across the country, solar generation starts fading just as electricity demand surges. Homes, industries, electric vehicles, data centres and digital infrastructure continue drawing power long after the sun has set. The challenge is no longer generating renewable energy. The challenge is making it available whenever the grid needs it. India added a record 50.9 GW of renewable energy capacity in FY26, taking its total renewable energy capacity to 274.68 GW. Yet every new solar park and wind project is reinforcing a reality that policymakers, utilities and developers can no longer ignore: renewable energy without storage cannot deliver the flexibility required by a rapidly modernizing economy.

This is where Battery Energy Storage Systems are rewriting the rules of the power sector.

Once viewed as a supporting technology, BESS is rapidly emerging as the backbone of renewable integration, grid stability, energy security and industrial electrification. From utility-scale storage projects and gigafactory investments to advanced battery chemistries, intelligent energy management systems and recycling infrastructure, an entirely new energy ecosystem is taking shape.

What has begun is far more than a race to manufacture batteries. It is a race to shape the future architecture of India’s power system. The storage decade has begun. The only question now is:

Who Will Lead the BESS Race?

India’s Storage Inflection Point : The Moment Storage Became Non-Negotiable

India’s renewable energy story has entered a new phase. For more than a decade, India’s clean energy transition was defined by a single objective: build renewable capacity at scale. The strategy worked. By March 2026, the country’s installed renewable energy capacity had reached 274.68 GW, cementing India’s position as the world’s third-largest renewable energy market. But success has created a new challenge.

The question is no longer how much renewable energy India can generate. The question is how reliably it can deliver that power when the sun isn’t shining and the wind isn’t blowing.

The pressure is already visible. In May 2026, India’s peak power demand touched a record 270.73 GW, driven by economic growth, rising cooling needs, urbanization, digital infrastructure, electric mobility and industrial electrification. At the same time, utilities are increasingly shifting from intermittent renewable procurement to round-the-clock and firm dispatchable power, creating a growing need for grid flexibility.

Recognizing this shift, the Central Electricity Authority projects India will require 236.22 GWh of Battery Energy Storage System (BESS) capacity by 2031-32, alongside pumped hydro storage, taking the country’s total storage requirement to 411.4 GWh.

The challenge extends far beyond renewable integration. AI-driven data centres, semiconductor manufacturing, green hydrogen projects and EV charging networks are all expected to intensify demand for reliable power. This is why Battery Energy Storage Systems are no longer viewed as a supporting technology. They are rapidly becoming the infrastructure layer that connects renewable generation with reliability, flexibility and energy security.

The first chapter of India’s energy transition was about building renewable capacity. The second chapter will be about storing it. And that is precisely where the battle for BESS leadership begins.

The Policy War: Who Will Scale Fastest?

If battery technology forms the engine of India’s storage revolution, policy is providing the fuel. Over the past three years, India’s Battery Energy Storage System (BESS) market has evolved from a technology opportunity into a policy-driven infrastructure sector. Through Viability Gap Funding (VGF), Energy Storage Obligations (ESO), renewable-plus-storage tenders and transmission incentives, policymakers are actively creating the foundations of a long-term storage market.

The biggest catalyst has been the VGF mechanism. After initially supporting 13.2 GWh of storage capacity, the Ministry of Power approved a second VGF tranche worth ₹5,400 crore in 2025 to support an additional 30 GWh of BESS projects. The scheme is expected to unlock investments of nearly ₹33,000 crore, significantly improving the economics of utility-scale storage deployment.

Yet subsidies alone will not define the next phase of growth.

The more important shift is the emergence of structural demand. Renewable-plus-storage procurement, co-located storage projects and Energy Storage Obligations are steadily embedding batteries into India’s power planning framework. As utilities move towards firm and dispatchable renewable power, storage is transitioning from a supplementary asset to a core grid requirement.

At the same time, evolving market mechanisms are expanding the value of storage beyond simple energy shifting. Ancillary services, grid balancing, peak demand management and energy arbitrage are creating multiple revenue streams that can strengthen project viability and attract private investment.

The policy momentum continues to accelerate. Policymakers are reportedly evaluating a new VGF framework worth nearly ₹15,000 crore that could support more than 112 GWh of storage capacity across batteries, pumped hydro and emerging technologies.

For companies competing in India’s BESS market, the message is clear. The next generation of market leaders may not simply be those with the largest factories or the lowest costs. They may be the companies that align most effectively with India’s evolving storage policies, procurement mechanisms and grid modernization agenda.

In the race for BESS leadership, policy is no longer supporting the market.

It is shaping it.

As India rapidly expands utility-scale Battery Energy Storage System deployment, what key policy reforms, market mechanisms, and regulatory frameworks will be most critical in determining the future leadership of the BESS sector?

Hiren Pravin Shah, Founder & MD and CEO – Replus Engitech, said, “India’s BESS leadership will be shaped by how quickly storage moves from pilot-scale adoption to a bankable, grid-integrated asset class. Policy support is already moving in the right direction through VGF, storage obligations and transmission-related incentives, but the next priority is market depth. BESS needs clearer revenue visibility across peak shifting, ancillary services, capacity support and renewable firming. Tender design must also balance cost with safety, performance and lifecycle guarantees. The sector cannot be built only on the lowest tariff. Leadership will come from countries and companies that combine policy certainty, strong technical standards, domestic manufacturing and disciplined project execution.”

Praveen Kumar Powar, Head Plant Operations, JSW Energy, said, “India’s leadership in the Battery Energy Storage System (BESS) sector will depend not only on rapid deployment but also on building a strong domestic manufacturing ecosystem. While India has already established a clear demand trajectory through the Energy Storage Obligation (ESO), Viability Gap Funding (VGF) schemes, and large-scale utility tenders, the next phase of growth will require targeted policy interventions that create a level playing field for Indian manufacturers.

A key priority is the introduction of an Approved List of Battery Manufacturers (ALBM), similar to the highly successful ALMM framework implemented in the solar sector. The combination of ALMM, Production Linked Incentive (PLI) schemes, and supportive procurement policies enabled India to emerge as one of the world’s largest solar module manufacturing hubs. A similar framework for BESS would encourage domestic investment, ensure quality and reliability standards, and create long-term confidence for manufacturers.

In addition, government support mechanisms such as Viability Gap Funding (VGF) should be linked to the use of locally manufactured BESS systems. Public funds should not inadvertently support imported finished products when significant domestic manufacturing capacity is being established. Restricting VGF benefits to projects utilizing India-manufactured BESS, similar to domestic content and localization requirements adopted in other strategic sectors, would accelerate capacity creation, encourage private investment, generate employment, and strengthen the domestic supply chain.

Another critical requirement is a rational customs duty structure that promotes value addition within India. Currently, imported finished BESS products enjoy a significant cost advantage over domestically assembled systems, discouraging investments in local manufacturing. A phased increase in duties on fully assembled BESS products, while maintaining concessional duties on cells and key components that are not yet manufactured at scale in India, would support the development of a competitive domestic industry.

Equally important is the need for clarity around the implementation of the MOOWR scheme and similar duty deferment mechanisms. While these schemes were originally designed to promote manufacturing and exports, their use for importing and supplying finished BESS products into the domestic market can create an uneven competitive landscape for Indian manufacturers who are investing in local assembly, testing, integration, and workforce development. Clear policy guidelines are therefore necessary to ensure that such schemes support genuine domestic manufacturing and align with the objectives of Make in India and Aatmanirbhar Bharat. If not addressed, such practices risk discouraging domestic investments and undermining the development of a self-reliant BESS manufacturing ecosystem.

India is expected to require over 236 GWh of battery storage capacity by 2031-32, representing a substantial economic and industrial opportunity. With the right combination of ALBM, localization-linked VGF support, calibrated customs duties, clear regulatory frameworks, and quality standards, India can replicate the success achieved in solar manufacturing and establish itself as a global hub for BESS production, innovation, and exports.”

The Chemistry War: Which Technology Will Dominate?

Every major industrial revolution has been shaped by a defining technology battle. For Battery Energy Storage Systems (BESS), that battle is increasingly being fought at the chemistry level.

The stakes are enormous. According to the International Energy Agency (IEA), battery storage is now the world’s fastest-growing power technology. Global battery storage deployments reached 108 GW in 2025, a 40% increase over the previous year, with installed capacity growing more than eleven-fold since 2021. The question is no longer whether storage will scale, but which technologies will dominate that growth.

For now, Lithium Iron Phosphate (LFP) has emerged as the undisputed market leader. The IEA estimates that nearly 90% of global battery storage deployments now rely on LFP chemistry, driven by its lower costs, longer cycle life and superior thermal stability compared with alternative lithium-ion technologies. As utilities increasingly prioritize safety, reliability and lifecycle economics, LFP has become the benchmark technology for grid-scale applications.

Yet history suggests that technology leadership rarely remains uncontested.

Sodium-ion batteries are rapidly emerging as one of the most closely watched challengers. Unlike lithium-based systems, sodium-ion batteries rely on more abundant raw materials and offer the potential to reduce exposure to critical mineral supply constraints. The technology has already begun moving beyond research laboratories, with CATL recently securing its first major 60 GWh sodium-ion energy storage agreement, while the IEA has identified 2026 as a potentially pivotal year for commercialization.

Meanwhile, solid-state batteries continue attracting global investment due to their potential to improve energy density and safety, while flow batteries are gaining attention for long-duration storage applications where discharge duration is often more important than energy density.

For India, however, the chemistry race extends beyond performance metrics. Storage systems must withstand high temperatures, demanding operating conditions and rapidly expanding renewable energy deployment. As a result, battery management systems, thermal management, safety architecture and lifecycle optimization may prove just as important as cell chemistry itself.

The future BESS race may therefore not be won by a single battery technology. Instead, leadership could belong to the companies capable of translating chemistry innovation into scalable, bankable and grid-ready energy storage solutions.

In the first phase of the storage revolution, the battle was about deployment.

The next phase may be decided by chemistry.

As the global energy storage industry evolves rapidly, how do you see next-generation battery chemistries and storage technologies reshaping the competitiveness, scalability, and long-term economics of BESS deployments?

Hiren Pravin Shah, Founder & MD and CEO – Replus Engitech, said, “ The next phase of BESS will not be defined by one chemistry alone. Lithium-ion will continue to play a major role, especially where energy density, response time and supply maturity matter. At the same time, chemistries such as sodium-ion, LFP improvements and long-duration storage technologies will become important for specific use cases. The real competitiveness will come from matching the right chemistry to the right application. For India, this is especially relevant because storage systems must perform across heat, dust, grid fluctuations and varied duty cycles. Strong BMS, EMS, thermal design and local engineering will decide lifecycle economics as much as cell chemistry.

Praveen Kumar Powar, Head Plant Operations, JSW Energy, said, “The global BESS industry is moving beyond a phase where lithium-ion alone defines competitiveness. The next decade will be shaped by application-specific storage technologies rather than a one-technology-fits-all approach.

Currently, LFP chemistry has become dominant for utility-scale deployments because of its safety profile, thermal stability, and cost advantage. However, as renewable penetration increases and grid operators demand longer discharge durations, we will see increasing diversification of storage technologies.

In my view, the future competitiveness of BESS will be influenced by four major parameters:

- Thermal Runaway and Safety.

- lifecycle economics,

- raw material availability,

- and energy density optimization for specific applications.

Technologies such as sodium-ion batteries are becoming highly relevant for stationary storage because they reduce dependency on lithium and critical minerals. While energy density may currently be lower, their long-term cost structure and supply-chain sustainability could make them highly attractive for grid-scale applications.

Similarly, solid-state batteries may significantly improve safety and energy density, but commercial scalability and manufacturing economics still require maturity before mass deployment in utility storage.Beyond electrochemical storage, I see strong long-term potential in:

- flow batteries for long-duration applications,

- hybrid storage architectures,

- hydrogen-integrated energy storage,

- and thermal storage systems for industrial applications.

However, one important industry reality is that technology success is not determined only in laboratories. It is determined on factory floors and at project sites.

Many advanced chemistries face challenges in:

- process repeatability,

- yield stabilization,

- thermal management,

- supply-chain maturity,

- and field reliability under real operating conditions.

From a manufacturing leadership perspective, scalability is the true differentiator. The industry leaders will be those capable of industrializing advanced technologies while maintaining cost competitiveness, quality consistency, and operational reliability at giga-scale production levels.

The next phase of BESS evolution will therefore be a combination of chemistry innovation and manufacturing excellence.”

India’s Manufacturing & Investment Race

While policy is creating demand and technology is driving innovation, long-term leadership in the BESS sector will ultimately depend on manufacturing capability.

The Central Electricity Authority projects India will require 236.22 GWh of battery storage capacity by 2031-32, creating a massive opportunity across cell manufacturing, battery packs and system integration. To support this transition, the Government of India launched the ₹18,100 crore Advanced Chemistry Cell (ACC) Production-Linked Incentive scheme, targeting 50 GWh of domestic cell manufacturing capacity and attracting investments of nearly ₹45,000 crore.

The response has been significant. Reliance, Amara Raja, JSW, Exide and other players have announced large-scale battery manufacturing plans, while strategic partnerships are helping accelerate access to advanced cell technologies and production expertise.

Yet manufacturing capacity alone will not guarantee success. Critical mineral access, component supply chains, technology partnerships, skilled talent and recycling infrastructure will all play a crucial role in determining competitiveness.

The next phase of the race will be defined not by announcements, but by execution. The companies that successfully translate investment commitments into operational capacity and resilient supply chains will be best positioned to capitalize on India’s growing storage opportunity.

In the battle for BESS leadership, manufacturing is no longer just an industrial objective—it is a strategic advantage.

The Economics of Storage

For years, the biggest challenge facing Battery Energy Storage Systems was cost. Today, that equation is changing rapidly.

According to BloombergNEF’s 2025 Battery Price Survey, average lithium-ion battery pack prices fell to a record low of $108/kWh, while battery packs designed for stationary storage dropped to just $70/kWh—the lowest-cost battery segment globally. As battery prices decline, the economics of storage are improving across utility-scale applications.

The impact is already visible in India. According to the Institute for Energy Economics and Financial Analysis (IEEFA), standalone BESS tariffs discovered in 2025 fell to as low as ₹1.48 lakh/MW/month for two-hour systems. Meanwhile, India’s cumulative energy storage tender pipeline expanded from 6.8 GW in 2018 to more than 90 GW by 2025, reflecting the rapid transition of storage from pilot projects to mainstream infrastructure.

However, falling battery prices tell only part of the story.

The real shift lies in revenue stacking. Modern BESS projects can generate value through renewable energy firming, peak demand management, energy arbitrage, ancillary services and frequency regulation. This ability to monetize multiple grid services is steadily improving project bankability and investor confidence.

As storage deployment accelerates, project economics are increasingly being evaluated through lifecycle performance, Levelized Cost of Storage (LCOS) and long-term revenue potential rather than upfront capital costs alone. With costs continuing to decline and revenue opportunities expanding, the BESS race or BESS is rapidly evolving from a support technology into a bankable energy infrastructure asset.

As Battery Energy Storage Systems move toward large-scale commercial deployment, what major economic factors and business models will be most critical in improving project viability, accelerating adoption, and ensuring long-term profitability across the BESS ecosystem?

Hiren Pravin Shah, Founder & MD and CEO – Replus Engitech, said, “Project viability will depend on how storage earns value through multiple channels. A BESS asset should not be seen only as a capital cost attached to renewable power. It can support peak demand, frequency response, grid balancing, renewable firming, energy arbitrage and distribution-level reliability. Business models will therefore need to move towards stacked revenues and long-term service-based contracts. Financing will improve when developers, utilities and lenders have confidence in performance guarantees, degradation assumptions, safety standards and replacement planning. India’s BESS market will scale faster if economics are built around lifecycle value, not only upfront price.

Praveen Kumar Power, Head Plant Operations, JSW Energy, said, “As BESS deployments move toward large-scale commercialization, project viability will increasingly depend on business model innovation rather than only battery cost reduction.

Earlier, the industry’s focus was heavily centered on capex economics. Today, investors are evaluating the complete lifecycle value proposition — including performance guarantees, degradation behavior, operational efficiency, and revenue stacking capability.

One of the most critical economic factors will be the reduction in Levelized Cost of Storage (LCOS). This will improve through:

- better manufacturing scale,

- localization,

- higher energy efficiency,

- optimized thermal management,

- and improved battery lifecycle performance.

However, in real commercial deployments, the biggest game changer will be revenue diversification.

A sustainable BESS project in the future will likely combine multiple income streams such as:

- Peak demand management,

- Renewable integration support,

- Ancillary grid services,

- Capacity markets,

- Energy trading,

- Transmission optimization.

This multi-service utilization model is essential because standalone arbitrage economics are often insufficient for long-term profitability.

I also believe Energy Storage-as-a-Service (E SaaS) models will gain momentum. Many industrial and utility customers prefer performance-based contracts instead of heavy upfront capex investment. This creates opportunities for long-term recurring revenue models supported by strong O&M capabilities and digital monitoring platforms.

Another major factor will be bankability and investor confidence. Large-scale projects require:

- predictable performance warranties,

- robust safety validation,

- strong EPC execution capability,

- reliable after-sales service ecosystems.

From my operational experience, one important aspect often overlooked is plant execution efficiency. Manufacturing productivity, automation maturity, quality control systems, and supply chain planning directly influence the final economics of BESS projects.

In the coming years, the industry will move from a “battery supply business” to a complete energy infrastructure business. Companies that can integrate technology, manufacturing, digital intelligence, lifecycle service, and grid understanding into one ecosystem will create sustainable long-term profitability.

Ultimately, the future leaders in BESS will not be identified only by installed capacity, but by their ability to deliver reliable, economically optimized, and scalable energy storage solutions across the entire lifecycle”

Recycling & Critical Minerals

Every battery deployed today will eventually become a source of tomorrow’s raw materials.

As India accelerates its energy transition, securing long-term supplies of lithium, nickel, cobalt and other critical minerals is emerging as one of the biggest challenges facing the Battery Energy Storage System (BESS) ecosystem. While much of the global conversation has focused on mining and refining, policymakers are increasingly viewing recycling as a strategic pillar of energy security.

Recognizing this challenge, the Government of India launched the National Critical Mineral Mission (NCMM), allocating ₹16,300 crore through FY31 to strengthen critical mineral value chains. A key component of the mission is a dedicated ₹1,500 crore Critical Mineral Recycling Incentive Scheme aimed at developing domestic recycling capacity for lithium-ion batteries, e-waste and industrial scrap.

Why Recycling Suddenly Matters

- India is projected to require 236.22 GWh of BESS capacity by FY32.

- Demand for lithium, nickel and cobalt is expected to rise sharply as battery deployment accelerates.

- Recycling can reduce import dependence while creating a domestic source of critical minerals.

- Black mass recovery is emerging as a strategic industry segment within the battery value chain.

The opportunity is significant. Under the recycling incentive scheme, the government is targeting the recovery of critical minerals from spent lithium-ion batteries and electronic waste while supporting the development of urban mining infrastructure. In April 2026, 58 companies were declared eligible under the scheme, highlighting growing industry interest in battery recycling and material recovery.

At the centre of this emerging ecosystem lies black mass—the material recovered from end-of-life batteries that contains valuable metals such as lithium, nickel and cobalt. Rather than treating used batteries as waste, recyclers increasingly view them as future resource reservoirs capable of feeding critical materials back into the manufacturing cycle.

Companies such as Lohum and Attero are already expanding their recycling and critical mineral recovery capabilities, while advances in recovery technologies are helping improve material extraction rates and commercial viability.

The Next Competitive Frontier

Future leaders participating in BESS race may need to master:

- Lithium recovery

- Black mass processing

- Battery-grade material refining

- Second-life battery applications

- Circular supply-chain integration

Critical mineral security

As battery deployment scales, circularity is becoming a competitive advantage rather than a sustainability initiative. The companies that successfully recover, refine and reintroduce critical minerals into the manufacturing cycle may strengthen supply-chain resilience, improve resource security and reduce long-term costs across the energy storage ecosystem.

In the next phase of India’s storage journey, leadership may depend not only on who manufactures batteries—but on who can bring their materials back to life.

Smart Storage & Grid Intelligence

The next battle in the BESS race may not be fought inside the battery cell—it may be fought inside the software controlling it.

As renewable penetration rises and power systems become increasingly complex, intelligent energy management is emerging as a critical differentiator. The International Energy Agency estimates that global electricity consumption from data centres could approach 945 TWh by 2030, driven largely by artificial intelligence and digital infrastructure. Managing these increasingly dynamic power flows will require smarter storage systems capable of responding in real time.

Modern BESS assets are already evolving beyond simple charge-and-discharge functions. AI-enabled Energy Management Systems (EMS), advanced Battery Management Systems (BMS) and predictive analytics platforms can optimize battery performance, extend asset life and maximize revenues across multiple value streams, including energy arbitrage, ancillary services and peak demand management.

Meanwhile, grid-forming inverters are attracting growing attention for their ability to support voltage and frequency stability in renewable-heavy power systems. As conventional thermal generation gradually declines, these technologies are expected to play an increasingly important role in maintaining grid reliability.

The next frontier could be Virtual Power Plants (VPPs), where thousands of distributed energy resources operate as a single coordinated asset. While still at an early stage in India, VPPs are already gaining traction globally as utilities seek greater flexibility and grid resilience.

As battery technologies become increasingly standardized, competitive advantage may shift toward the intelligence layer that sits above the hardware. In the future, the companies leading the BESS race may not simply build better batteries—they may build smarter ones.

Who Will Actually Lead the BESS Race?

After examining policy evolution, chemistry innovation, manufacturing expansion, storage economics, recycling ecosystems and grid intelligence, one conclusion becomes increasingly clear: India’s BESS race is unlikely to produce a single winner.

Instead, leadership is emerging across multiple strategic battlegrounds, each of which could prove decisive in shaping the future of the country’s energy storage ecosystem.

The Ecosystem Builder: Reliance Industries

If future leadership is determined by value-chain control, Reliance enters the race as one of the strongest contenders. The company is commissioning a 40 GWh battery gigafactory at Jamnagar with a roadmap that could eventually reach 100 GWh. More importantly, Reliance is building an integrated ecosystem that spans battery materials, cell manufacturing, energy storage systems, renewable energy and recycling.

While several players are building factories, Reliance is attempting to build an entire storage economy under one roof. Its biggest challenge will be execution, but its ecosystem ambition remains unmatched.

The Most Balanced Domestic Contender: Amara Raja

If Reliance represents ambition, Amara Raja represents execution. Through its Telangana Giga Corridor, the company is building 16 GWh of cell manufacturing and 5 GWh of battery pack capacity while simultaneously leveraging decades of battery manufacturing experience.

Unlike many emerging players that are still translating announcements into assets, Amara Raja has already operationalized battery pack manufacturing and secured global technology partnerships. Few domestic companies currently score as consistently across manufacturing, deployment readiness, chemistry strategy and policy alignment.

The Infrastructure & Storage Deployment Leader: JSW Energy

The future leader of the BESS market may not necessarily manufacture the most batteries. It may be the company that owns and operates the most storage infrastructure.

This is where JSW Energy stands apart. The company has secured major utility-scale storage projects, including a 500 MW/1,000 MWh standalone BESS project from SECI, while simultaneously expanding its broader energy storage portfolio toward 40 GWh by 2030.

As India’s renewable energy capacity expands, storage asset ownership and grid integration could become as important as battery manufacturing itself.

The Future Manufacturing Challenger: Agratas

Backed by the Tata Group, Agratas is emerging as one of the largest battery manufacturing bets in the country. Its 20 GWh Sanand facility, combined with a 40 GWh UK gigafactory, gives it a manufacturing vision exceeding 60 GWh.

Unlike some competitors, Agratas is still in the build-out phase, but few companies possess similar long-term industrial backing. If manufacturing scale becomes the defining factor of India’s battery future, Agratas will remain a serious contender.

The Storage Intelligence & Integration Specialist: Replus Engitech

As storage systems become increasingly sophisticated, software, integration and operational intelligence may prove just as important as battery manufacturing.

Replus represents this pathway. The company is expanding its battery manufacturing capacity from 1 GWh to 6 GWh while simultaneously deploying utility-scale storage projects, including a 250 MWh project for Hero Future Energies. Its strengths lie in energy management systems, battery analytics, thermal management and storage integration.

If the future BESS race shifts toward performance optimization rather than manufacturing scale alone, Replus could emerge as one of the industry’s most influential technology-led players.

The Solar-to-Storage Integrator: Waaree Energies

Waaree’s advantage lies in its ability to connect two of India’s fastest-growing industries—solar and storage.

Waaree has announced ambitious battery manufacturing plans, including a 16 GWh integrated lithium-ion gigafactory in Andhra Pradesh and a broader 20 GWh cell and battery-pack manufacturing strategy. In 2026, it secured a major 350 MW/1,400 MWh BESS EPC contract, demonstrating that its ambitions extend beyond manufacturing into deployment and execution.

As renewable-plus-storage projects become increasingly common, Waaree’s integrated solar-to-storage model could become a powerful competitive advantage.

The Pure-Play BESS Specialist: GoodEnough Energy

While conglomerates are building broad energy ecosystems, GoodEnough Energy is pursuing a different strategy—focus.

The company commissioned a 7 GWh BESS manufacturing facility in Noida and plans to expand to more than 25 GWh within the next few years. Unlike diversified energy companies, every major strategic decision at GoodEnough revolves around storage.

That specialization could become increasingly valuable as India’s BESS market matures and customers seek dedicated storage expertise.

The Verdict

The defining characteristic of India’s BESS race is that every major contender is pursuing a different route to leadership.

Reliance is betting on ecosystem integration.

Amara Raja is betting on balanced execution.

JSW Energy is betting on storage infrastructure ownership.

Agratas is betting on manufacturing scale.

Replus is betting on storage intelligence.

Waaree is betting on renewable-plus-storage integration.

GoodEnough is betting on specialization.

The eventual winner may not be the company with the largest factory, the biggest balance sheet or even the highest deployment pipeline. Leadership is more likely to emerge at the intersection of manufacturing scale, technology innovation, project execution, software intelligence, policy alignment and ecosystem integration.

What began as a race to build batteries is rapidly evolving into a contest to shape the future architecture of India’s power system. The companies that successfully combine these capabilities will not simply lead the BESS market race—they may help define the next decade of India’s energy transition.