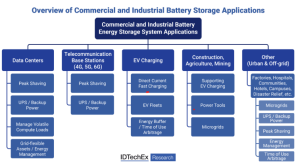

Battery demand for stationary commercial and industrial (C&I) battery energy storage systems (BESS) is expected to rise across multiple industries, including data centers, telecommunication base stations (5G, 6G), electric vehicle (EV) charging, construction, agriculture, mining, and essential sectors such as factories, hospitals, communities, and disaster relief. According to a report presented by IDTechEx, the global C&I BESS market is projected to reach US$21 billion by 2036, driven by applications including uninterruptible power supply (UPS), peak shaving, microgrids, time-of-use arbitrage, grid flexibility, and managing volatile AI compute loads in data centers.

Historically viewed as a niche segment compared to grid-scale and residential battery storage, the C&I BESS market is poised for significant expansion, with demand expected to grow fivefold between 2026 and 2036. Market players will need to adapt as applications evolve and compete with established Li-ion BESS manufacturers such as CATL, BYD, and Tesla. The report draws insights from dozens of primary interviews with C&I BESS stakeholders, highlighting projects, targeted applications, and emerging battery technologies.

Data Center Battery Storage

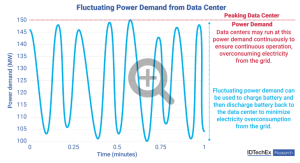

The demand for battery storage in data centers will track power demand to cover critical loads, including servers, storage, and network infrastructure. As hyperscale AI data centers expand, power requirements for UPS will increase, ensuring continuous operation, avoiding data loss, and maintaining service level agreements. Battery storage will also help manage volatile AI compute loads, reducing electricity waste and costs by charging when supply exceeds demand and discharging when demand spikes.

While valve-regulated lead-acid (VRLA) batteries have traditionally supported UPS, Li-ion batteries are increasingly replacing them due to higher cycle life and decreasing costs. However, Li-ion batteries face challenges including degradation and fire risk. Redox flow batteries (RFBs) may be better suited for high-cycle applications, as they offer minimal degradation and non-flammable electrolytes. Longer-duration storage solutions such as RFBs are expected to play a larger role in energy management for growing data centers.

C&I Battery Storage Technologies

Li-ion costs continue to decline, with rising demand in US and Europe driving the development of domestic Li-ion supply chains. Programs such as the 45X Manufacturing Production Tax Credit and the One Big Beautiful Bill Act (OBBBA) are expected to support the production of LFP Li-ion cells domestically. The report provides cost comparisons for US-manufactured LFP cells versus imported Chinese LFP cells, factoring in tax credits and tariffs from 2026 onwards.

Beyond Li-ion, alternative battery technologies including Na-ion, second-life EV batteries, RFBs, and VRLA are also being developed for C&I applications, each with trade-offs in cost, energy density, cycle life, safety, and response time. The report benchmarks these technologies and evaluates their suitability for various C&I use cases.

Market Forecasts

The report provides 10-year forecasts (2025–2036) for global C&I BESS markets, including demand by GWh and market value by region and application. Data center-specific BESS forecasts are included by GW per region, alongside cost analyses and component breakdowns for Li-ion C&I BESS.

Over 30 company profiles are included, covering major Li-ion BESS manufacturers and developers of alternative technologies such as RFBs, Na-ion, second-life EV batteries, VRLA, and zinc-based batteries. The report includes primary research insights on projects, strategic agreements, and technology adoption trends.

This comprehensive report highlights the evolving commercial and industrial battery storage market, tracking technology trends, costs, regional developments, and forecasts for the next decade across multiple critical applications.