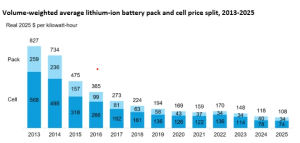

According to BloombergNEF’s 2025 Lithium-Ion Battery Price Survey, lithium-ion battery pack prices have fallen 8% since 2024, reaching a record low of $108 per kilowatt-hour. The decline is driven by continued cell manufacturing overcapacity, intense competition, and a growing shift to lower-cost lithium iron phosphate (LFP) batteries, despite rising battery metal costs.

Battery metal prices rose in 2025, partly due to supply risks at certain Chinese lithium assets and new cobalt export quotas in the Democratic Republic of Congo. However, these increases did not result in higher annual prices for cells or packs. The industry absorbed the impact through greater LFP adoption, long-term contracts, and wider hedging strategies.

China has consistently produced more cells than required for domestic electric vehicle and stationary storage needs, creating intense competition among suppliers. The effect has been most evident in stationary storage, where multiple manufacturers are able to serve the same projects. China’s strong dominance in LFP production has enabled its manufacturers to meet nearly all global demand.

BNEF’s battery price survey covers a range of end uses, including different electric vehicle types and stationary storage projects, each with distinct performance requirements and pricing dynamics. Battery pack prices for stationary storage fell to $70/kWh in 2025, 45% lower than in 2024, marking the sharpest decline across all segments and making stationary storage the lowest-priced segment for the first time. Battery electric vehicle (BEV) packs were the lowest-priced within the transport category at $99/kWh; this was the second year they remained below $100/kWh.

Average LFP battery pack prices across all segments stood at $81/kWh, compared with $128/kWh for nickel manganese cobalt (NMC) packs.

Evelina Stoikou, head of BNEF’s battery technology team and lead author of the report, said: “Cut-throat competition is making batteries cheaper every year. This is an important moment for the industry, as record-low battery prices create an opportunity to lower EV costs and accelerate the deployment of grid-scale storage to support renewables integration around the world.”

The report also highlights regional price differences. China recorded the lowest average battery pack prices at $84/kWh. Prices in North America and Europe were 44% and 56% higher, respectively, due to higher production costs and greater reliance on imported batteries. China saw the largest price decline, down 13% in real terms from 2024, while North America and Europe recorded drops of 4% and 8%. The steeper decline in Europe was driven by changing U.S. policies and tariffs, prompting Chinese companies to redirect exports to Europe and adopt more aggressive pricing strategies.

BNEF expects pack prices to fall again in 2026 as raw material prices face upward pressure but low-cost LFP adoption continues. Longer-term cost reductions are expected through ongoing R&D investment, manufacturing efficiency improvements, and supply chain expansion, along with emerging technologies such as silicon and lithium metal anodes, solid-state electrolytes, new cathode materials, and new cell manufacturing processes.

The full report provides insights on:

- Battery prices across chemistries, regions and segments

- Raw material and battery component price dynamics

- BNEF’s view of global prices in 2026 and beyond

- Key drivers behind price trends this decade

- Public statements and roadmaps from leading industry players

- Impact of tariffs and transport costs on battery prices