India’s energy transition is not just being powered by innovation—it is being quietly reshaped by what happens after the battery dies. As electric mobility accelerates and storage systems expand, a parallel industry is rising with equal urgency: battery recycling. Yet, beneath the optimism lies a complex interplay of timing, technology, and trust.

To navigate this labyrinth of “urban mining,” we bring together a vanguard of industry titans. Nitin Gupta sheds light on the digital formalization of fragmented networks; Gaurav Dolwani explores the strategic paradox of building capacity for a future peak; Vishal Gupta discusses the vital preparation of systems before the “EV cohort” retires; and Manikumar Uppala challenges us to view recycling not as waste management, but as a sophisticated materials-refining business.

Together, their insights reveal an industry building ahead of its own supply, navigating fragmented collection systems, and confronting the realities of economics and scale. At its core, battery recycling is no longer a downstream activity—it is emerging as a strategic lever in India’s quest for resource security and circularity.

As policies evolve and technologies mature, the race is already underway. The leaders, however, will not be those who simply scale—but those who integrate, adapt, and anticipate.

Read on as industry voices decode the challenges, opportunities, and the road ahead for India’s battery recycling ecosystem.

India is rapidly building battery recycling capacity, but large-scale battery waste generation is still evolving. Do you see a gap between capacity creation and actual feedstock availability?

Nitin Gupta, Co-founder and CEO, Attero, said, “There is a short-term mismatch, but it is expected. Capacity is being built ahead of peak volumes because recycling infrastructure takes time to scale, while battery waste follows a lag of 3-7 years. India is projected to generate 5-6 lakh tonnes of used lithium-ion batteries annually by 2030, rising to over 2 million tonnes by 2035. In the interim, feedstock comes from three sources: early EV retirements, consumer electronics, and manufacturing scrap. The real challenge is not availability, but channelisation. A significant portion of material still flows through informal networks, which limits utilisation of formal capacity. Attero has addressed this through platforms like Selsmart and MetalMandi, which help bring dispersed material into formal systems, improving utilisation of recycling capacity.”

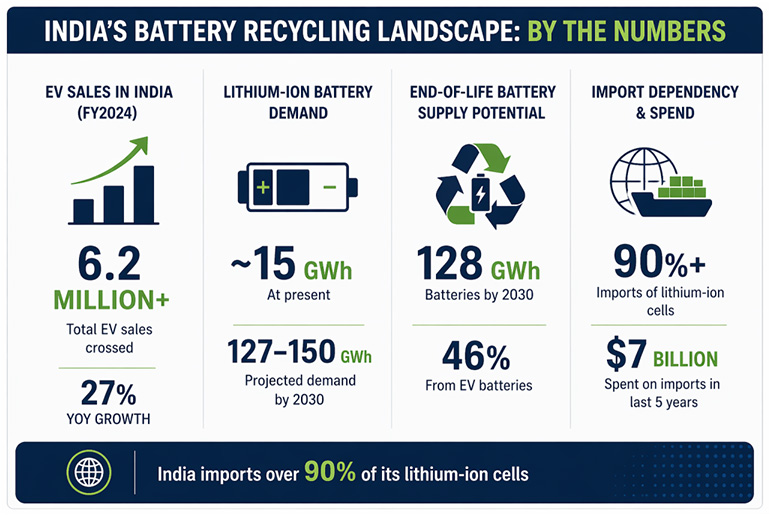

Gaurav Dolwani, CEO at LICO Materials, said, “India’s EV transition is accelerating rapidly. By the end of FY2025, cumulative EV sales crossed 6.2 million units, with over 2 million vehicles sold in the year alone—a 27% year-on-year increase. In parallel, lithium-ion battery demand stands at ~15 GWh annually and is projected to surge to 127–150 GWh by 2030. On the supply side, an estimated 128 GWh of end-of-life batteries will become available for recycling by 2030, with EV batteries contributing 46% of this volume.

However, the timing of this opportunity is critical. Most EVs being sold today will reach end-of-life only over the next 5–6 years, meaning the real wave of EV battery recycling feedstock will peak between 2028 and 2032. For recyclers, this creates a strategic paradox: capacity must be built now, but feedstock at scale will come later.

At LICO, this gap was anticipated early. Our Bengaluru facility, designed as a zero-liquid-discharge, zero-waste operation, currently operates at 17,500 metric tons annually, with expansion to 30,000 tons planned by 2028, aligned with the expected surge in battery returns. In the interim, we rely on a diversified sourcing strategy: manufacturing scrap from cell producers, end-of-life consumer electronics, EV OEM’s, and global sourcing partnerships across key markets. As global trends indicate, manufacturing scrap will remain the dominant recycling feedstock until the next decade, making early diversification essential for long-term viability.”

Vishal Gupta, Co-founder & CTO, MaxVolt Energy Industries Limited, said, “There is an absolutely visible gap today. This can be seen as a classic case of infrastructure moving ahead of supply. In anticipation of future demand driven by EV adoption and energy storage systems, the recycling capacities are being strengthened. However, the volume of end-of-life batteries is still relatively low. Most lithium-ion batteries in India are yet to complete their lifecycle. However, this is a temporary imbalance. Over the next 3-5 years, the early EV cohorts will eventually retire. This gives rise to the feedstock availability. The real opportunity lies in preparing systems today, so we are not caught unprepared tomorrow.”

Manikumar Uppala, Co-Founder and Chief of Industrial Engineering, Metastable Materials, said, “Yes, there is a gap between capacity creation and feedstock availability, but it is mostly misunderstood and can often be overstated. As a country, India is building recycling capacity ahead of waste availability, anticipating demand, which is understandable in an emerging circular industry. It takes a long time to build processing infrastructure, but battery waste generation is tied to deployment cycles which are now beginning to mature. It is the industry’s near-term challenge due to underutilization of assets.

The real issue is not really the existence of a gap, but how companies respond to it. If plants are being set up to process end of life EV batteries only, will definitely struggle. If the systems they are deploying can handle mixed inputs like manufacturing scrap, consumer electronics, black mass and recover materials across the spectrum, they can absorb this growing phase.

While some may see capacity creation as premature, it is accurate as without building infrastructure, the country would face more serious bottlenecks when volumes scale suddenly. So, the current phase is more about system learning and stabilizing process, developing the workforce and supply chain formation.”

With EPR regulations and policy push in place, how prepared is the ecosystem—collection, logistics, and traceability—to support efficient battery recycling at scale?

With EPR regulations and policy push in place, how prepared is the ecosystem—collection, logistics, and traceability—to support efficient battery recycling at scale?

Nitin Gupta, Co-founder and CEO, Attero, said, “The regulatory framework is well defined, especially with EPR, but execution is still evolving. Collection and logistics remain fragmented, and traceability is not yet fully enforced. A significant share of batteries still moves through informal channels. This is where digital platforms are becoming critical. Selsmart addresses consumer and enterprise collection with doorstep pickup and transparent pricing, while MetalMandi formalises sourcing from aggregators and scrap dealers by bringing price discovery and traceability into the system. For EPR to deliver at scale, such models need to expand alongside stronger enforcement and digital tracking.”

Gaurav Dolwani, CEO at LICO Materials, said, “India’s policy framework for battery recycling is among the most comprehensive globally. The Battery Waste Management Rules, 2022, introduced Extended Producer Responsibility (EPR), making OEMs, importers, and sellers accountable for end-of-life battery management. Clear recycling targets—70% by FY25, 80% by FY26, and 90% from FY27 create a strong compliance roadmap. Recent amendments have further strengthened the system through mandatory QR-based traceability, a digital CPCB EPR portal, and a transparent credit registry. Financially, the government has reduced input costs by exempting customs duty on battery waste and critical minerals, while also launching targeted incentives under the National Critical Mineral Mission. The mandate to incorporate recycled content into new batteries scaling to 20% by FY31 creates long-term structural demand.

However, a gap persists between policy intent and on-ground execution. Nearly 70–80% of battery waste still flows through the informal sector, where unsafe recycling practices lead to material loss and environmental damage. Collection networks remain fragmented, and reverse logistics for EV batteries are still evolving.

At LICO, through the Clappia app, together with our reverse logistics network, we enable safe battery transport and provide OEMs with end-to-end, real-time visibility into the entire battery lifecycle through a fully transparent, traceable system.”

Vishal Gupta, Co-founder & CTO, MaxVolt Energy Industries Limited, said, “The policy intent is strong, but execution is still under the development phase. The collection networks are fragmented, while informal channels still dominate a large portion of battery disposal. The traceability is improving through digital registries and EPR compliance frameworks, especially for lithium-ion batteries. However, it is not seamless. Logistics is another challenge due to safety concerns and high transportation costs. The ecosystem needs tighter integration between manufacturers, recyclers, and collection partners. It also needs stronger enforcement to bring informal players into the formal loop.”

Manikumar Uppala, Co-Founder and Chief of Industrial Engineering, Metastable Materials, said, “Policy intent is ahead of execution. The Battery Waste Management Rules (2022) have created a clear compliance structure but it will take a while for the associated ecosystem such as reverse logistics, traceability systems, and collection networks to develop. Currently, EPR is more of a compliance obligation and there is a shadow certificate market, sort of decoupled from actual recycling economics, distorting incentives. India also lacks a standardised nationwide battery take back infrastructure. Traceability is completely underdeveloped and without battery level tracking, the system cannot distinguish formal recycling from informal recycling leakage. Scaling recycling will remain constrained by material visibility and flow till these are actually solved.”

Can recycling realistically reduce India’s dependence on imported critical minerals, or will it remain a supplementary solution in the near term?

Nitin Gupta, Co-founder and CEO, Attero, said, “In the near term, recycling will complement imports, but its strategic role will expand quickly. Attero’s technology, based by over 47 global patents, is designed to recover high-purity lithium, cobalt, nickel, and rare earth elements, making recycled materials suitable for direct use in manufacturing. As battery volumes scale, urban mining can supply a meaningful share of India’s critical mineral demand. The advantage is not just supply security, but also lower carbon intensity compared to primary extraction. Over time, recycling will move from being a supplementary source to a core component of domestic material supply chains.”

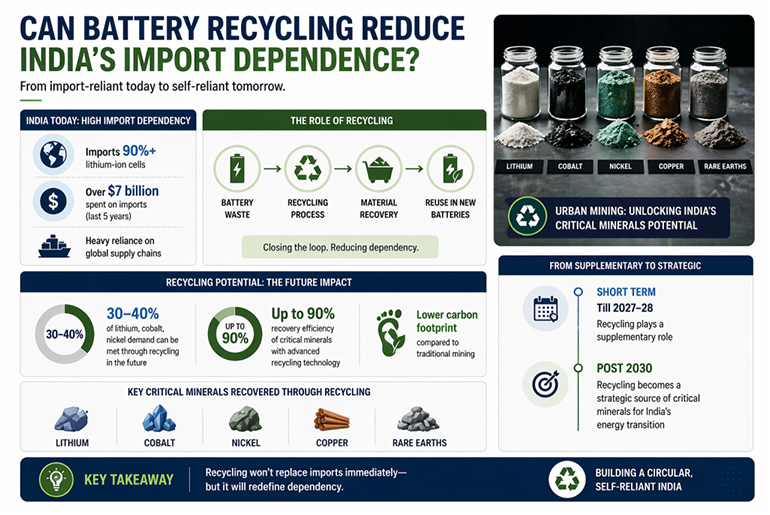

Gaurav Dolwani, CEO at LICO Materials, said, “Recycling will play a dual role in India’s energy transition, but its impact is strongly time dependent. In the near term, up to 2027–28, it remains a supplementary solution. The current EV fleet is still young, and end-of-life battery volumes are not yet large enough to significantly offset imports. However, this dynamic shifts sharply from the late 2020s, making the post-2030 trajectory critical for today’s investment decisions.

India’s dependence on imports underscores the urgency. India imports more than 90% of its lithium-ion cells and virtually all critical battery minerals, with over $7 billion spent on Chinese LIB imports over the past five years. China controls 70 to 90% of global battery cell manufacturing and is responsible for nearly 85% of global battery cell production. As demand for lithium and other key materials accelerates exponentially this decade, this reliance becomes a strategic vulnerability.

Recycling begins to materially change this equation in the early 2030s. Estimates suggest that domestic recycling could supply 30–40% of lithium, cobalt, and nickel demand, with even higher recovery efficiencies for metals such as copper and aluminum. Over the long term, recycling has the potential to become a cornerstone of India’s resource security.

At LICO, we recover up to 90% of critical materials from end-of-life lithium-ion batteries and feed them back into cell manufacturing. With regulatory mandates requiring recycled content in new batteries, recycling is set to evolve from a supplementary pathway to a structurally essential pillar of India’s battery ecosystem.”

Gaurav Dolwani, CEO at LICO Materials, said, “Recycling will not be confined to replacement in the near term, it will be more supplementary. India is experiencing a growing demand for critical minerals like lithium, cobalt, and nickel. This makes recycling an important aspect. Over time, as battery volumes increase, urban mining through recycling can significantly offset import dependency. It might not be an immediate substitution, but it is a step towards building a circular economy that reduces vulnerability in the long run.”

Manikumar Uppala, Co-Founder and Chief of Industrial Engineering, Metastable Materials, said, “In the near term, it will be a supplementary solution. Recycling, while it won’t replace imports, it will reshape dependency. India’s current installed capacity of waste batteries is too small to offset primary minerals export, but it must be noted that recycling is the only domestic source of critical minerals, scalable in a meaningful manner within this decade. Mining timelines are long but recycling infrastructure is relatively quicker to deploy and improves with volume. Moreover, recycling reduces marginal import dependence, not absolute dependence. Even with a 20 to 30% substitution, at scale it materially changes supply security, price exposure and geopolitical risk. What we should realistically work towards is particle domestic circularity, from complete import dependence, and that shift is gradual and structurally significant.”

What are the biggest technological and economic challenges in achieving high-efficiency, commercially viable battery recycling in India today?

Nitin Gupta, Co-founder and CEO, Attero, said, “The main challenge is handling variability. Different battery chemistries require different recovery processes, which increases technological complexity. Attero has addressed this through sustained R&D and a strong intellectual property base, enabling recovery efficiencies exceeding 98% with 99.9% purity. On the economic side, feedstock aggregation remains a constraint, especially with informal channels offering faster payouts. This is where platforms like MetalMandi help improve price transparency and sourcing efficiency. Commercial viability ultimately depends on combining advanced technology with reliable, traceable feedstock and consistent industrial-scale operations.”

Gaurav Dolwani, CEO at LICO Materials, said, “One major issue is handling different battery chemistries, especially the growing use of LFP (Lithium Iron Phosphate). While India uses chemistries like NMC, LCO, LFP, and NCA, LFP is becoming more common because it is cheaper and safer. However, due to its lower-value material composition and absence of cobalt, it often falls short of meeting OEM performance and recovery expectations for recyclers. Developing efficient processes that work across all chemistries remains a key challenge.

Recovery efficiency is another important factor. Industry averages are around 75–80%, but better processes and smarter sorting can significantly improve this. Advanced technologies help increase recovery rates and improve the quality of extracted materials. The next step is hydrometallurgy, which can recover 95–99% of materials and produce battery-grade outputs.

On the business side, there are two main challenges. First, the business requires significant working capital to meet storage, safety, and compliance requirements. Second, the absence of long-term buying agreements makes the sector difficult to raise capital. However, upcoming regulations on recycled content are expected to create steady demand and make recyclers an essential part of the battery supply chain.”

Vishal Gupta, Co-founder & CTO, MaxVolt Energy Industries Limited, said, “On the technology front, achieving high recovery rates with cost efficiency is still a challenge. Processes like hydrometallurgy offer better yields but require significant investment and operational expertise. Battery chemistry diversity further complicates standardization. Economically, the biggest hurdle is viability. We have to deal with low feedstock volumes, high logistics costs, and fluctuating commodity prices impact margins. Until scale improves and supply chains stabilize, profitability will remain under pressure for many players.”

Manikumar Uppala, Co-Founder and Chief of Industrial Engineering, Metastable Materials, said, “The constraints are consistency, flexibility and profitability. Firstly, chemistry variability is a fundamental challenge. All emerging chemistries require different processing pathways and plants must be designed to handle this variability. Pre-processing gaps like safe dismantling, black mass consistency also directly impact downstream yields and safety. On the economic side, commodity price volatility creates unastable revenue assumptions, recycling economics are tied to lithium or cobalt, the prices of which can swing significantly. There is also a fixed capital that has to be deployed to set up a functioning plant whereas feedstock availability can fluctuate as well as different types of feedstock being used creates utilisation risk.”

Looking ahead, what will define leadership in India’s battery recycling space—technology, scale, partnerships, or policy alignment?

Nitin Gupta, Co-founder and CEO, Attero, said, “Leadership will be defined by integration across the value chain. Technology ensures recovery efficiency and output quality, scale drives economics, and partnerships secure feedstock. Attero’s approach has been to combine these with digital platforms such as Selsmart and MetalMandi, which address different parts of the supply chain, from consumers to aggregators. This integration allows better traceability, consistent material flows, and higher recovery outcomes. As the industry matures, leadership will depend on the ability to deliver manufacturing-grade materials at scale while maintaining compliance and supply reliability.”

Gaurav Dolwani, CEO at LICO Materials, said, “Leadership in battery recycling depends on four elements.

- Technology: High recovery rates and battery-grade output are non-negotiable. If recovered material doesn’t meet the purity standards required by gigafactories, it won’t sell. Advanced hydrometallurgy, with recovery rates of 95–99%, is emerging as the key differentiator between professional recyclers and basic processors.

- Feedstock: Reliable access to battery feedstock and assured offtake agreements depend on long-term trust. Strong relationships with OEMs and cell manufacturers ensure a steady supply of input and demand for recycled materials. India should look beyond and become a processor for the world.

- Scale: Expanding capacity without secured supply and demand can destroy value. Smart growth is aligned with actual market demand, especially as EV battery volumes increase over time.

- Policy: Regulations such as EPR and recycled-content mandates are enablers. Companies built around compliance will outlast informal players.”

Vishal Gupta, Co-founder & CTO, MaxVolt Energy Industries Limited, said, “Leadership will be defined by a combination of all four, but partnerships will be the real differentiator. Technology and scale are essential, but without strong upstream (OEMs, EV companies) and downstream (material buyers) collaborations, growth will be limited. Policy alignment will act as an enabler, ensuring compliance and incentives. The companies that build integrated ecosystems will emerge as leaders in this space.”

Manikumar Uppala, Co-Founder and Chief of Industrial Engineering, Metastable Materials, said, “All of these will influence leadership to some extent. Neither scale nor technology in isolation, but overall position in the value chain and control over material flows will also matter. First feedstock security for any manufacturing business to survive. Hence agreements with OEMs, energy storage operations, industrial users will define that edge. Output quality will determine margin structure, here is where technology will speak. Companies that can supply directly into the battery supply chain will operate in a fundamentally different economic tier. Technology, collection, partnerships and policy, all need to be integrated. The market will reward those who treat recycling as a materials refining business, not waste management.”