What ALMM List-II Means for India’s Solar Cell Industry

For years, India’s solar industry had one clear goal — install capacity as fast as possible. Cheap imports helped in this. Project costs came down. The Solar parks expanded rapidly. Developers chased aggressive commissioning timelines. India became one of the world’s fastest-growing renewable energy markets. But somewhere along the way, another question quietly became bigger. What happens if a country builds one of the world’s largest solar programs while depending heavily on imported solar cell equipment?

That question now sits at the center of India’s clean energy policy. The Ministry of New and Renewable Energy’s recent decision to refuse a blanket extension for mandatory ALMM List-II solar cell compliance beyond June 1, 2026 is not just another regulatory update. It is a strong policy signal. The government has made it clear that India’s next phase of solar growth will not be driven only by capacity addition. It will also be driven by manufacturing self-reliance.

The decision has effectively divided the solar industry into two camps.

On one side are project developers and EPC companies worried about supply constraints, higher costs, and project delays. On the other are domestic manufacturers who believe strict enforcement is necessary if India genuinely wants to reduce import dependence and build a globally competitive solar manufacturing ecosystem.

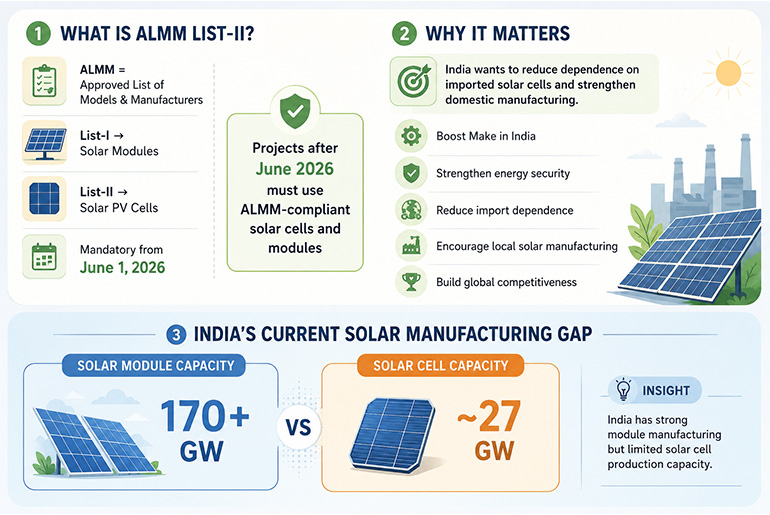

At the center of this debate is ALMM List-II.

And suddenly, a technical compliance requirement has turned into one of the most important industrial policy discussions in India’s renewable energy sector.

To understand why this matters so much, one must first understand what ALMM actually means.

For years, India remained heavily dependent on imported solar cells and modules, especially from China. While the country emerged as a major solar deployment market, the manufacturing side of the industry struggled to keep pace.

The Approved List of Models and Manufacturers (ALMM) framework was introduced to change that equation.

ALMM List for Solar Modules and Solar Cells

ALMM List-I focuses on approved solar modules, while ALMM List-II covers approved solar PV cells. Under the latest implementation timeline, projects commissioned after June 1, 2026 will be required to use both ALMM-compliant modules and ALMM-compliant solar cells.

In simple terms, the government now wants projects to increasingly rely on approved domestic manufacturing ecosystems rather than imported supply chains.

That sounds straightforward in policy language. In reality, however, the industry situation is far more complicated.

India’s solar sector is currently passing through an unusual transition phase. The country has significantly expanded module manufacturing capacity over the past few years. Industry estimates suggest India’s solar module manufacturing capacity has now crossed 170 GW, while solar cell manufacturing capacity still remains significantly lower at around 27 GW, with several new integrated facilities under development.

But solar cell manufacturing capacity still remains much lower.

Most industry estimates place India’s current solar cell manufacturing capacity in the range of 25 GW to 35 GW annually, depending on operational utilization levels and project commissioning schedules.

This gap between module capacity and cell capacity has become the biggest concern for developers.

Many project developers argued that while India’s manufacturing ambitions are understandable, domestic cell availability may still not be sufficient to support smooth project execution at the required scale.

Several stakeholders had therefore requested the government to provide a blanket extension for ALMM List-II implementation.

Their concerns were not entirely unreasonable. India’s renewable energy sector is currently handling massive project pipelines across utility-scale solar, commercial and industrial projects, open access projects, and rooftop installations. Delays in equipment availability can affect financing timelines, PPAs, commissioning schedules, and project economics.

Many developers also pointed toward ongoing geopolitical disruptions and logistics uncertainties. The Ministry itself referred to the Office Memorandum issued by the Department of Expenditure under the Ministry of Finance on April 29, 2026, which treated the ongoing West Asia situation as a war-like condition. The communication advised that project deadline extensions should be considered on a case-by-case basis rather than through blanket policy relaxations.

For developers, this created another layer of uncertainty. Freight routes, shipping timelines, and international supply chains have already witnessed multiple disruptions over the past few years. From the COVID-19 pandemic to Red Sea shipping risks and global commodity volatility, energy developers across the world have learned how vulnerable clean energy supply chains can become. But while developers pushed for flexibility, domestic manufacturers argued exactly the opposite.

According to manufacturers, India cannot keep delaying solar cell localization measures if it seriously wants to become a global clean energy manufacturing hub. Industry players say the country cannot continue depending heavily on imported solar cells while simultaneously aiming to build a self-reliant renewable energy ecosystem.

This argument carries significant weight. Over the past few years, the government has announced large Production Linked Incentive (PLI) schemes to encourage domestic solar manufacturing, particularly solar cell manufacturing and integrated facilities covering wafers, solar cells, and modules. Multiple Indian companies have already committed billions of rupees toward expanding domestic solar cell production capacities as part of India’s broader clean energy manufacturing push.

Several firms expanded aggressively after the government repeatedly signaled its intention to strengthen domestic manufacturing protection mechanisms for solar cells and related supply chains. For manufacturers, another blanket extension would have sent the wrong message to investors who have already invested heavily in local solar cell manufacturing capacity. Many believe policy inconsistency is one of the biggest reasons India historically struggled to build large-scale manufacturing ecosystems in sectors dominated by global imports. According to industry stakeholders, repeated delays in enforcing solar cell localization requirements could weaken confidence among companies investing in India’s domestic solar cell ecosystem.

This time, however, the government appears determined not to repeat that cycle.

And that is where the bigger geopolitical story begins.

The global solar industry today is deeply linked to China.

China dominates almost every major segment of the solar manufacturing supply chain, including polysilicon, wafers, solar cells, and modules. In several segments, Chinese companies control more than 80 percent of global manufacturing capacity, especially in solar cells and upstream materials.

Over the last decade, China achieved this dominance through scale, aggressive investments, integrated supply chains, strong state support, and manufacturing efficiency.

The result was simple. Chinese solar cells and solar equipment became cheaper than almost everyone else’s. Countries across the world, including India, rapidly expanded renewable energy installations using imported Chinese solar cells and modules because they significantly reduced project costs. But the global mood around manufacturing has started changing.

The COVID-19 pandemic exposed how dangerous excessive supply-chain concentration could become. Shipping disruptions, container shortages, raw material volatility, and geopolitical tensions forced governments everywhere to rethink industrial dependence on imported solar cells and clean energy equipment.

The United States responded with manufacturing-linked clean energy incentives under the Inflation Reduction Act. Europe started discussing strategic industrial autonomy in clean technologies. Several countries began examining ways to localize critical energy infrastructure, including solar cells and battery supply chains.

India’s solar policy shift must be viewed within this larger global transition.

Solar cells and solar panels are no longer being treated merely as energy equipment. Increasingly, they are being viewed as strategic infrastructure tied to national energy security.

Ganesh Moorthi, Chief Technology Officer, Luminous Power Technologies“The implementation of the Domestic Content Requirement (DCR) mandate from June 1 marks a significant step towards strengthening India’s solar manufacturing ecosystem and advancing the vision of a self-reliant renewable energy sector. The move is expected to accelerate investments across the solar value chain, improve supply-chain resilience, and create long-term opportunities for domestic manufacturers. It will also encourage healthy competition while driving greater focus on R&D, technology innovation, and quality enhancement across the industry.While the industry may witness some near-term supply constraints around DCR-compliant cells for rooftop solar during the initial phase of implementation, continued government support for domestic manufacturing can help accelerate capacity expansion, strengthen supply availability, and enable a smoother transition for the sector.At Luminous Power Technologies, we have consistently aligned our growth strategy with India’s clean energy ambitions. As a company fully committed to the ‘Make in India’ vision, all our inverters, batteries, and solar panels are manufactured domestically across our manufacturing facilities. Our upcoming manufacturing facilities in Odisha, including an advanced energy storage plant and a solar cell manufacturing facility, further reinforce our commitment to strengthening India’s domestic solar ecosystem and reducing import dependence.We believe the DCR framework will play a pivotal role in driving innovation, enhancing quality standards, strengthening energy security, and enabling sustainable long-term growth for the sector.”

For India, the concern is particularly important because the country has some of the world’s most ambitious renewable energy targets.

India aims to achieve 500 GW of non-fossil fuel capacity by 2030. Solar energy is expected to contribute a major share of this expansion.

But policymakers now appear to believe that large-scale renewable deployment without domestic manufacturing strength could create long-term strategic vulnerability.

This thinking explains why the government chose policy certainty over short-term flexibility.

The message from MNRE is becoming increasingly clear: India’s clean energy transition cannot remain permanently dependent on imported supply chains.

At the same time, the Ministry also appears aware that an abrupt transition could disrupt ongoing projects and damage investor confidence.

That is why the government stopped short of rejecting all relief measures completely.

Instead of providing blanket relaxation, MNRE has allowed project-specific extensions on a case-by-case basis.

Projects where substantial progress has already been made — including land acquisition, financial closure, connectivity arrangements, approval of electrical drawings, or module delivery — may still receive appropriate time extensions after assessment by an expert committee.

This approach reflects a balancing strategy.

The government wants to protect manufacturing policy credibility while also avoiding unnecessary disruption for projects already under execution.

A dedicated portal developed by the National Institute of Solar Energy (NISE) will now allow developers to submit claims for extensions along with supporting documentation.

This selective approach attempts to separate genuine execution challenges from broad industry-level delay requests.

Still, the broader industry impact of the decision is likely to remain significant.

Over the next few years, India’s solar market may witness stronger demand for domestically manufactured solar cells, greater investment in integrated manufacturing facilities, and accelerated localization across upstream supply chains.

The policy may also encourage more companies to invest in backward integration, including wafer and polysilicon manufacturing over the long term.

However, short-term pressure cannot be ruled out.

Why Solar Cells Matter Beyond Solar Projects

Domestic solar cell prices could remain relatively elevated during the transition phase. Developers may continue facing execution pressure until local manufacturing scales further. Certain project timelines could witness delays as supply chains adjust to the new compliance environment.

But governments often accept short-term friction when pursuing larger industrial goals.

And this is no longer only about solar.

India is increasingly applying the same strategic thinking across multiple clean energy sectors.

The battery industry is witnessing localization pushes under Advanced Chemistry Cell (ACC) PLI schemes. Green hydrogen policies are encouraging domestic electrolyzer manufacturing. Energy storage systems are gradually moving toward local value addition frameworks.

Across sectors, the direction appears similar.

India wants to avoid replacing fossil fuel import dependence with clean energy equipment import dependence.

That may ultimately become one of the defining industrial policy themes of the next decade. The debate around ALMM therefore goes far beyond one deadline or one compliance requirement. It reflects a deeper transition inside India’s clean energy strategy itself. For years, success in renewable energy was measured mainly through installed capacity numbers. Now another metric is becoming equally important — how much of that infrastructure India can manufacture domestically.

That shift will shape future investment decisions, supply-chain structures, manufacturing economics, and competitive dynamics across the renewable energy sector.

The solar industry may remain divided in the short term.

Developers will continue demanding smoother implementation pathways. Manufacturers will continue pushing for stronger enforcement and policy consistency.

But one thing is becoming increasingly clear.

India’s renewable energy ambitions are now closely tied to manufacturing ambition.

And with its latest ALMM decision, the government has made it evident that it is willing to defend that direction — even if it creates temporary discomfort for parts of the industry.