“One thing for sure, the battery market loves to break assumptions and long term/ mid-term forecasts thus remains questionable, let’s all wait and see how 2026 shapes things, so are you ready for 2026? Well, I am! see you on the better side” – I ended by 2025-year end article for Battery Magazine writing this, what happened thereafter has been both overwhelming and underwhelming for the industry at large.

Let’s talk about the global scenario, Lithium carbonate cost, which was rising last year kept rising, in around 6 months’ time the rise with respect to the minimum price of August 2025 has been around 135 – 140%, Li-C cost has overshoot its cost as on Jan 2023 but is still way below the highs of 2022-23. What it has resulted in is the rise on Li-Ion battery cell cost, what around the same time in 2025 was quoted around 35-40 USD/kWh is ranging between 55 – 60 USD/kWh today. With the fear of the same still going higher looming at the backdrop of Chinese VAT export rebates reducing to 0% from 2027. The ever fluctuating and rising dollar price against INR has compounded the effect. To add to this the lead time for procurement has also increased.

How did India progress in the first 6 months of 2026 in this challenging environment? Let’s explore.

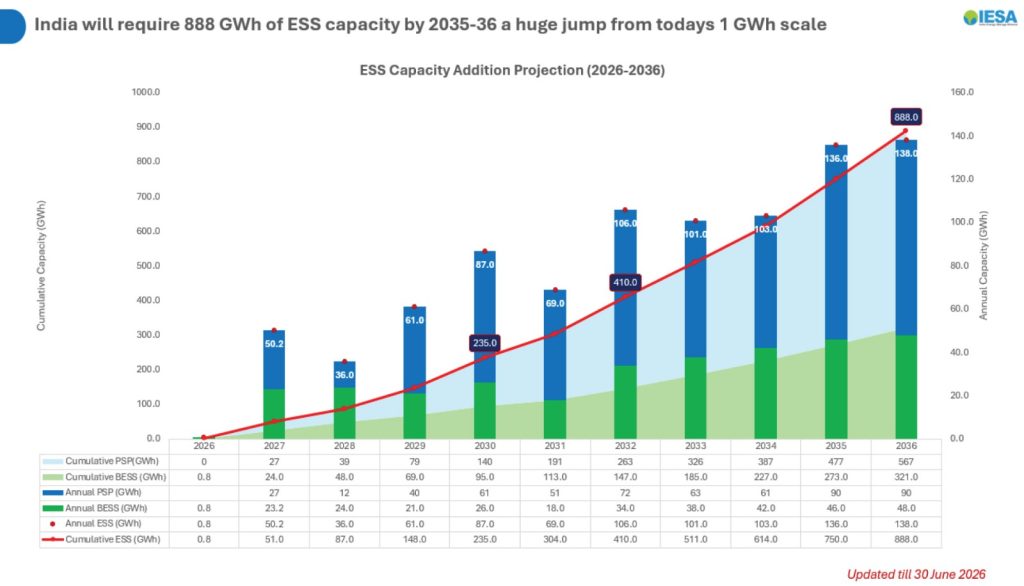

The Generation Adequacy Study by CEA projects to requirement of 888GWh of ESS capacity in the grid by 2035-36, which will entail 80 GW/ 321GWh of BESS and 94 GW/ 567 GWh of PSP. The opportunity for India thus is huge! CERC brought BESS under Tariff framework and introduced DSM rules for PSP and BESS. CEA finalized the Safety regulations for BESS and SECI was made the only nodal agency (REIA) to issue tenders henceforth. What was encouraging to witness is the states being actively bringing out regulations/ policies for BESS. Maharashtra in its RE + BESS Policy forecast requirement of 100 GWh of ESS in the state by 2035-36 with mandatory BESS inclusion at all levels of RE. Rajasthan shared BESS Regulation for the state and Gujarat shared draft norms for separate market for Standalone BESS and FTC of BESS, the state is working on a policy for BESS too.

The Generation Adequacy Study by CEA projects to requirement of 888GWh of ESS capacity in the grid by 2035-36, which will entail 80 GW/ 321GWh of BESS and 94 GW/ 567 GWh of PSP. The opportunity for India thus is huge! CERC brought BESS under Tariff framework and introduced DSM rules for PSP and BESS. CEA finalized the Safety regulations for BESS and SECI was made the only nodal agency (REIA) to issue tenders henceforth. What was encouraging to witness is the states being actively bringing out regulations/ policies for BESS. Maharashtra in its RE + BESS Policy forecast requirement of 100 GWh of ESS in the state by 2035-36 with mandatory BESS inclusion at all levels of RE. Rajasthan shared BESS Regulation for the state and Gujarat shared draft norms for separate market for Standalone BESS and FTC of BESS, the state is working on a policy for BESS too.

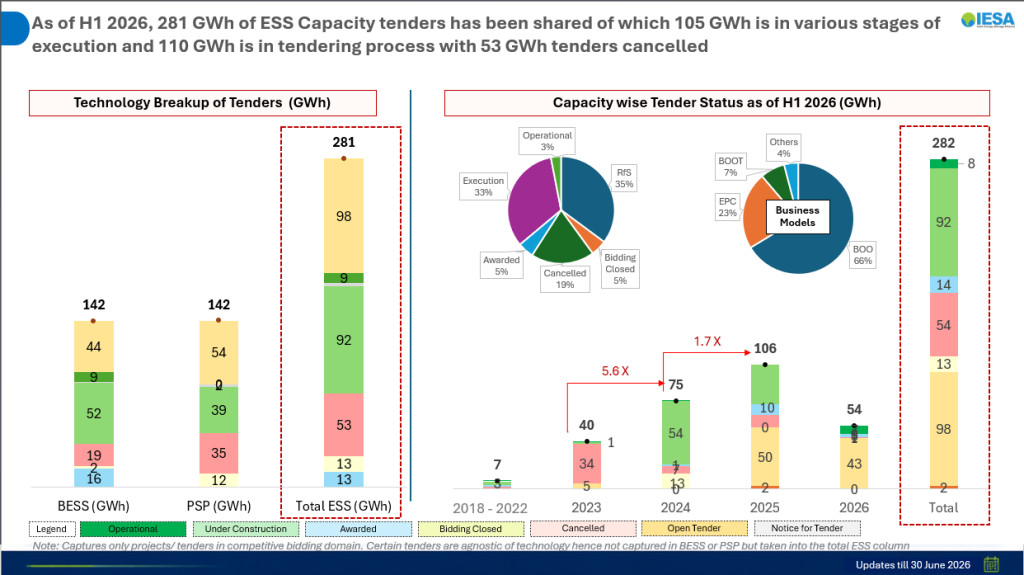

The tendering scene in 2026 has been a bit slow basis of the developments happening and the 2nd VGF tenor ending in March. Jan to June a total of 47 GWh worth of ESS tenders has been floated in India by various tendering agencies, NTPC combines (NTPC, NREL, NGEL) has tendered 22 GWh worth of BESS tenders predominantly under EPC mode. Compared to 2025, the total capacity tendered has been down by 7 GWh, the size of each tender has significantly increased this year with the average capacity of tenders being 1.5 GWh and of 4 hours duration. With MoP discussing on the next phase of VGF, the tendering activity too is expected to increase in second half of 2026.

A total of 17 projects worth of 39 GWh capacity got their tariff approved by respective commissions. With 18 GWh of tenders getting awarded in H1 2026. The tariffs ofcourse were elevated than what we saw in 2025 with 2hrs, 2 cycles ranging on an average to INR 3.35 lacs/MW/month (without VGF). The year started off on a big news Solar + 6 Hours of storage (1 hour continuous) discovering a tariff of INR 3.13/kWh. Overall, the market is showing signs of moving to maturity and more realistic numbers being seen in bids submitted.

Of course a few hiccups in the journey happened too,

the first 6 months of 2026 saw 3 tenders being cancelled after discovery of tariff,

- Telangana cancelled 250 MW/ 500 MWh tender awarded at INR 2.4 – 2.45 lacs/ MW/month,

- WBSEDCL cancelled 250 MW/ 1000 GWh (with greenshoe option of extra 1 GWh) tender awarded at INR 3.47 lacs/MW/month and

- APTEL cancelling MDESCL’s 2000 MW/ 4000 MWh tender awarded at INR 1.65 lacs/MW/month.

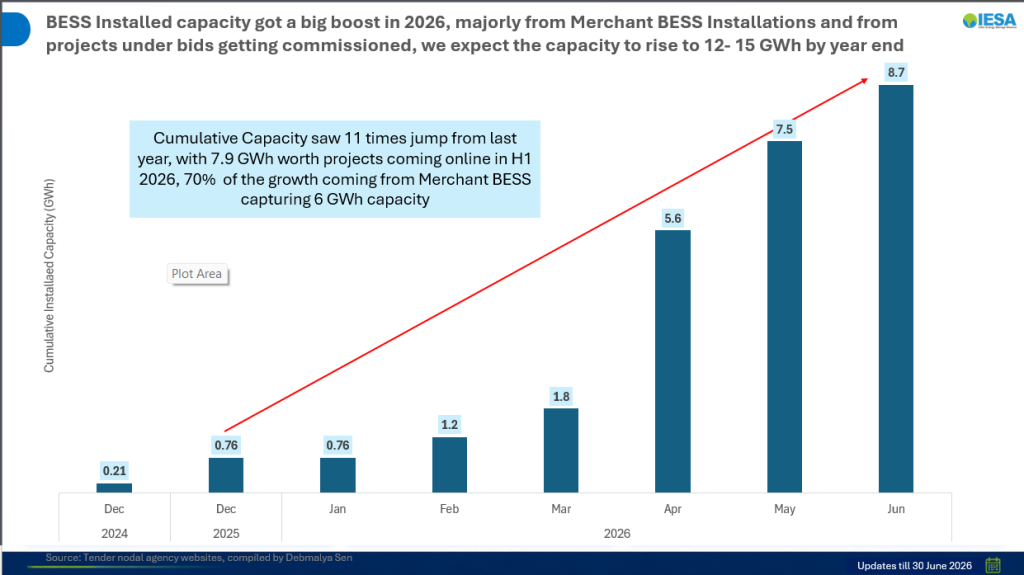

There are enough reasons to celebrate to amidst all these, in December 2025 the total commissioned capacity of BESS projects in India stood at 0.78 GWh (10 projects). That number has seen 11 times jump to 8.7 GWh (18 projects). Of course, a large amount of such projects comes as Merchants to the Grid, with Adani commissioning 3.4 GWh in Khavda (Gujarat), ACME commissioning 3.2 GWh in Bikaner (Rajasthan) and Juniper commissioning 500 MWh of capacity in Rajasthan. A total of 7.1 GWh capacity was added to the Grid in H1 2026 as merchant BESS. This apart L&T commissioned 254 MWh BESS in Bihar, Indigrid along with Ampere hour commissioned 360 MWh for GUVNL (the first under competitive bidding mode). Pace Digitek commissioning 500 MWh for MSEDCL and Kolkata Metro commissioning 6.4 MWh of capacity. With another 2 – 3 GWh in pipeline India is set to cross the 10 GWh mark for BESS by December 2026.

As on date a total of 227 GWh of ESS capacity is tendered (excluding the cancelled capacity) which includes 123 GWh of BESS, out of which 53 GWh of BESS capacity is under execution while 16 GWh is awarded.

As on date a total of 227 GWh of ESS capacity is tendered (excluding the cancelled capacity) which includes 123 GWh of BESS, out of which 53 GWh of BESS capacity is under execution while 16 GWh is awarded.

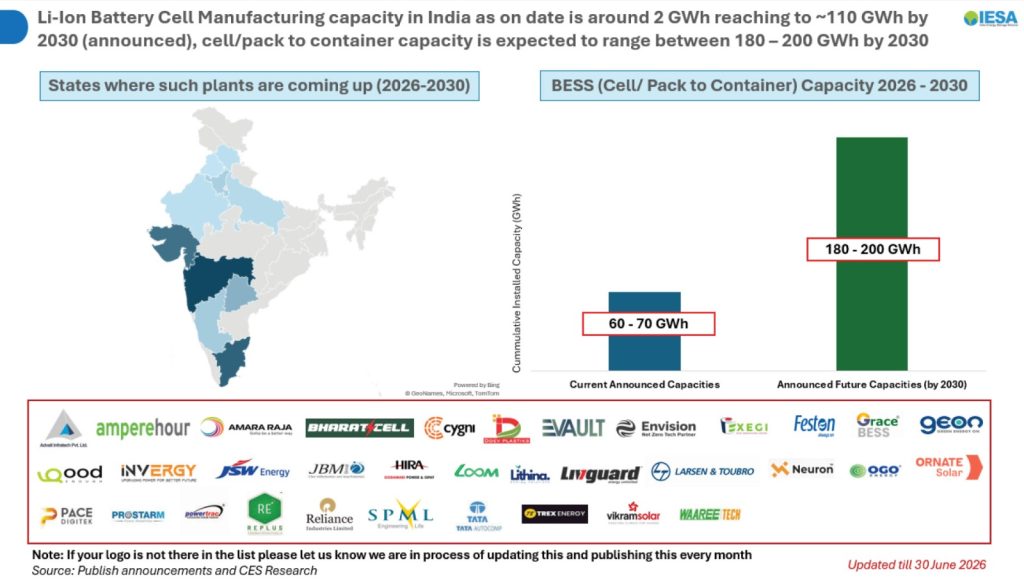

The manufacturing areas of the BESS journey has not been making the right noises, while cell manufacturing in India has been facing its own set of challenges, the pack assembling sector or should I say cell to container sector has picked up with major announcements being made in H1 2026. India’s cell manufacturing capacity at the end of H1 2026 stood at around 4 GWh with around 10 – 13 GWh in construction, pack manufacturing stood at 32 – 37 GWh rising to approx. 100 – 130 GWh by 2030 and container manufacturing stood at 10 – 15 GWh rising to 180 – 220 GWh by 2030. Ministry has been vocal about executing Approved List of Battery Manufacturers (ALBM) and Minimum Local Content (MLC) in the sector with MPPMCL tender also for the first time asking for a 50% MLC for BESS to avail VGF, is it practically possible and is industry ready for this mandate is something which is debated.

The manufacturing areas of the BESS journey has not been making the right noises, while cell manufacturing in India has been facing its own set of challenges, the pack assembling sector or should I say cell to container sector has picked up with major announcements being made in H1 2026. India’s cell manufacturing capacity at the end of H1 2026 stood at around 4 GWh with around 10 – 13 GWh in construction, pack manufacturing stood at 32 – 37 GWh rising to approx. 100 – 130 GWh by 2030 and container manufacturing stood at 10 – 15 GWh rising to 180 – 220 GWh by 2030. Ministry has been vocal about executing Approved List of Battery Manufacturers (ALBM) and Minimum Local Content (MLC) in the sector with MPPMCL tender also for the first time asking for a 50% MLC for BESS to avail VGF, is it practically possible and is industry ready for this mandate is something which is debated.