Every few weeks, a new renewable energy tender enters the market. One day it is a solar project. The next week it is a battery energy storage system (BESS) tender. Then comes a pumped hydro energy storage (PHES) project, a round-the-clock renewable energy bid, or a hybrid power tender combining solar, wind and storage. If you regularly follow the power and renewable energy sector, you would have noticed that tenders are no longer just about setting up a solar plant and selling electricity. The Renewable energy tender models in India have become more complex. New terms such as EPC, BOO, RTC, FDRE, BESS-as-a-Service, PHES-as-a-Service, reverse auction and greenshoe option are becoming common across bid documents. These structures may look like technical paperwork, but they decide who builds the project, who owns it, how developers recover their investments and how utilities procure power. In many ways, renewable energy tender models in India are now shaping the future of the country’s clean energy market.

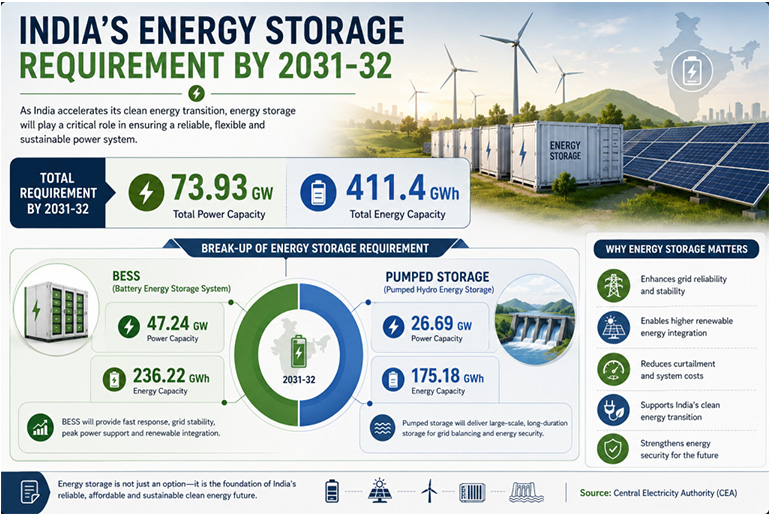

India’s renewable energy capacity is growing quickly and it is also getting ready to deploy energy storage on a large scale. With the CEA estimating that India will need 73.93 GW and 411.4 GWh of total energy storage by 2031/32, this will create an opportunity for new types of energy storage technologies, including pumped storage and battery energy storage systems.

As renewable energy projects become larger and more storage-intensive, renewable energy tender models in India are also evolving to meet new grid requirements.

Why Renewable Energy Tender Models in India Are Changing

A decade ago, most utility-scale solar tenders followed a relatively simple structure. Developers bid tariffs, won projects and supplied electricity through long-term power purchase agreements. The market today looks very different.

Solar and wind power are growing rapidly across the country. India experienced a historic, record-breaking year. As of March 2026, India’s total installed Renewable Energy capacity stands at a massive 275 GW (with solar making up roughly 55% of that mix). The government is also targeting 500 GW of non-fossil fuel capacity by 2030.

To support this growth, the Ministry of New and Renewable Energy (MNRE) had earlier announced a bidding trajectory of 50 GW of renewable energy tenders every year from FY24 to FY28. But adding renewable capacity is only one part of the challenge. Solar power is available during the day. Wind generation changes with weather conditions. Power demand, however, continues throughout the day and night. This is one reason why storage has become a major part of new renewable energy procurement. As a result, renewable energy tender models in India are moving beyond standalone solar projects towards integrated structures involving storage, flexibility and firm power delivery.

Let’s Decode the Most Common Renewable Energy Tender Models in India

If you come across the renewable energy tenders regularly, you will come across a few business models repeatedly.

EPC Model

The EPC (Engineering, Procurement, and Construction) project model is the most commonly used model in the renewable energy industry. The EPC contractor has responsibility for designing and constructing the project (including sourcing all necessary materials). The original owner (developer) remains the owner of the facility after completion. EPC contracts are widely used in solar parks, government projects and utility-owned renewable energy plants. Many state utilities and public sector companies continue to use EPC contracts for solar and storage deployment because they retain ownership of the asset after commissioning.

BOO Model

BOO stands for Build, Own and Operate. This is currently one of the most common renewable energy tender models in India. Under the BOO structure, the developer invests in the project, owns the asset and operates it during the contract period. Revenue comes through power purchase agreements or service contracts. Power Purchase Agreements and Service contracts are how revenue is created. Most Utility-Scale Solar Wind and Battery Storage Projects are purchased (awarded) from SECI tenders via the BOO framework. Developers benefit from visibility of revenue over the long term by using the BOO method, and Utilities can reduce capital expenditure (cost) at the start (upfront).

BOOT Model

BOOT refers to Build, Own, Operate and Transfer. In this model, the developer owns and operates the project for a fixed period before transferring ownership to the procuring agency. Although BOOT is widely used in infrastructure sectors, it is less common in utility-scale renewable energy projects in India.

DBFO Model

DBFO stands for Design, Build, Finance and Operate. Here, the developer takes responsibility for project design, financing, construction and operations. The model is more common in transmission infrastructure and large public-private infrastructure projects but is increasingly discussed in energy storage and transmission-linked renewable projects.

How Reverse Auctions Changed India’s Renewable Energy Market

One of the biggest changes in renewable energy tender models in India came through tariff-based competitive bidding. Earlier, renewable projects often operated under feed-in tariffs fixed by regulators. Today, most large renewable energy projects are awarded through reverse auctions. In a reverse auction, developers compete by offering the lowest tariff. The lowest eligible bidder generally wins the project.

SECI has played a major role in popularizing this mechanism. SECI awarded a total of over 73.8 gigawatts (GW) of renewable energy capacity as of May 2025; this includes solar, wind, and hybrid projects. The use of a reverse auction process has led to significant reductions in the solar tariff rate, which has resulted in accelerated development of renewable energy projects across India. Increased competition resulting from these auctions has put pressure on project economics, requiring developers to make technology selection, finance, and execution decisions that optimise project results.

Storage Is Creating New Renewable Energy Tender Models in India

Energy storage is changing the way renewable energy tenders are designed. Earlier, storage was treated as a separate asset. Today, storage is increasingly becoming part of renewable energy projects themselves. This shift has led to the emergence of entirely new renewable energy tender models in India.

BESS-as-a-Service

Battery Energy Storage System as a Service is becoming a widely used method. BESS developers build, own and run battery storage systems. Utilities or project owners do not directly buy the battery asset and instead pay for battery storage service for a long-term contract. This helps utilities avoid large upfront costs while getting access to storage capacity. There have been a number of recent tenders for battery storage that used service-based procurement frameworks with viability gap funding and long-term service agreements.

PHES-as-a-Service

The latest example comes from NTPC Renewable Energy Limited (NTPC REL). The company recently invited bids for 2,000 MW and 12,000 MWh of pumped hydro energy storage capacity under a PHES-as-a-Service model. Under this structure, developers will build, own, operate and maintain the pumped storage projects while NTPC REL will use the storage capacity as a service for 25 years.

The model is attracting attention because pumped hydro projects require large investments and long development timelines. So, instead of owning the assets, utilities can have storage services via long-term agreements, and the developers manages the project ownership and operations.

Energy Storage Service Agreements

Behind these service models lies the Energy Storage Service Agreement (ESSA). These agreements define how storage capacity is made available, performance obligations, charging arrangements and payment structures.

As battery and pumped storage deployments increase, ESSAs are becoming an important part of renewable energy tender models in India.

RTC and FDRE Projects Change Procurement Strategies

The renewable energy market is no longer limited to stand-alone generation projects. Utilities want power when they want it, not just when it’s sunny or windy.This has led to the rise of RTC and FDRE projects.

Round-the-Clock Renewable Energy Projects

RTC projects combine multiple technologies to provide continuous power supply.A typical RTC project may include:

- Solar power

- Wind power

- Battery storage

- Pumped hydro storage

The objective is to maintain high availability throughout the day.These projects are becoming important for utilities seeking dependable renewable energy supply without relying heavily on conventional thermal generation.

Firm and Dispatchable Renewable Energy Projects

FDRE projects take this concept a step further. Developers must supply power according to a predefined schedule. To achieve this, they often combine solar, wind and storage assets. MNRE has already issued bidding guidelines for FDRE projects involving renewable energy systems integrated with storage. Many industry experts view FDRE as one of the most important developments in renewable energy procurement because it focuses on reliability rather than only capacity addition.

Tender Terms Every Renewable Energy Professional Should Know

As renewable energy tender models in India become more advanced, several procurement terms are appearing frequently in bid documents.

Greenshoe Option

A greenshoe option allows the procuring agency to increase project allocation beyond the original tender size. For example, a 1,000 MW tender may include a greenshoe option of 500 MW. This means the final allocation can increase to 1,500 MW without launching a fresh tender. The provision offers flexibility when bidder interest is high and additional capacity is required.

Bucket Filling Methodology

Storage tenders increasingly use bucket filling mechanisms. Suppose an agency requires 2,000 MW of storage capacity. Developers submit bids with different capacities and prices. Projects are then selected from the lowest-priced bids until the required capacity is fully allocated.

Viability Gap Funding

Viability Gap Funding (VGF) is government financial support provided to improve project economics. VGF has become particularly important for battery storage projects, where capital costs remain relatively high.The mechanism helps accelerate deployment while reducing financial risk for developers.

ISTS Waiver

ISTS refers to the Inter-State Transmission System. Transmission charge waivers have played a major role in improving project viability for large renewable energy developments. Many developers consider ISTS benefits while evaluating project locations and bidding strategies.

The Agencies Driving Renewable Energy Tender Models in India

Several organisations are shaping renewable energy procurement across the country.

SECI

The Solar Energy Corporation of India remains the largest renewable energy implementing agency in the country. The organisation conducts competitive bidding for solar, wind, hybrid, RTC and FDRE projects. As of May 2025, SECI had awarded over 73.8 GW of renewable energy capacity.

NTPC REL

NTPC Renewable Energy Limited has become increasingly active in renewable energy and storage procurement. Its recent 2,000 MW pumped hydro storage service tender highlights the growing importance of long-duration energy storage.

NHPC and SJVN

Both companies are expanding their renewable energy portfolios through solar, storage and hydro-linked projects. They are also playing a larger role in tendering and project development activities.

State Utilities

State discoms are increasingly procuring renewable energy with storage rather than standalone solar power. This trend is expected to continue as power demand patterns become more complex.

Where Renewable Energy Tender Models in India Are Heading

The next phase of renewable energy growth will not be defined only by solar capacity additions. It will be shaped by how renewable energy, storage and grid flexibility work together. Battery storage projects are becoming larger. Pumped hydro projects are returning to the spotlight. Hybrid projects are becoming more common. Tender documents are also becoming more sophisticated as developers and utilities look for new ways to balance cost, reliability and long-term performance.At the same time, challenges remain. Transmission constraints, project delays and unsold renewable energy capacity continue to affect the market. Industry reports have also pointed to growing volumes of awarded projects awaiting power purchase agreements and transmission readiness. Yet the direction is becoming clear.

A decade ago, renewable energy tenders were mainly about building solar plants and discovering the lowest tariff. Today, renewable energy tender models in India are increasingly focused on storage, flexibility, dispatchability and long-term grid support. The language of tenders is changing because the power system itself is changing. And as solar, BESS and PHES projects become more interconnected, the business frameworks behind these projects will play an even bigger role in determining how India’s clean energy transition moves forward.