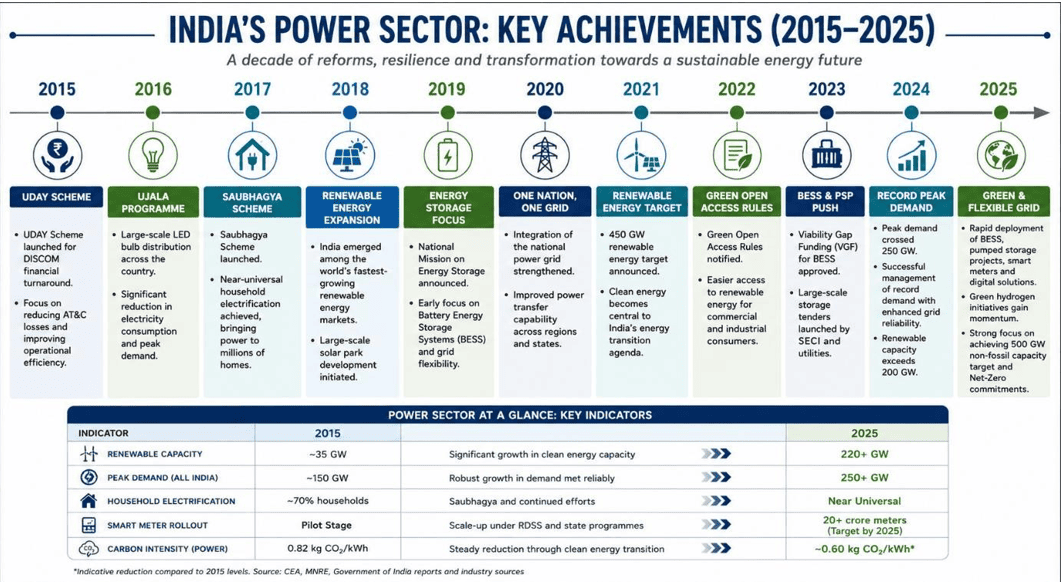

Today, India stands shoulder to shoulder with the world’s leading economies, driven by its rapid development trajectory and decisive policymaking. The power sector has played a pivotal role in this transformation, serving as a key enabler of growth across industries, agriculture, healthcare, infrastructure, and the broader economy. A reliable and expanding power system has been instrumental in supporting India’s development ambitions and strengthening its position on the global stage.

Over the past decade, India has emerged as a key player in the global energy transition through its focus on clean energy, energy security, and sustainable development. The country has made significant progress in expanding renewable energy capacity, improving electricity access, and advancing its climate commitments, including achieving several Nationally Determined Contribution (NDC) targets ahead of schedule.

Driven by the vision of Viksit Bharat and its commitment to achieving Net Zero emissions by 2070, India continues to strengthen its energy sector through policy reforms, large-scale renewable energy deployment, and investments in emerging technologies, laying the foundation for a reliable, resilient, and sustainable energy future.

India’s energy transition is not limited to expanding generation capacity alone. Over the past several years, the country has been pursuing a balanced approach that prioritizes energy transition, affordability, sustainability, and energy security simultaneously. In May 2026, India’s peak electricity demand crossed 270 GW, a figure that reflects only the demand connected to the national grid and excludes captive power generation. This highlights the rapidly growing electricity requirements of the country and underscores the importance of ensuring long-term energy security.

India’s energy transition is not limited to expanding generation capacity alone. Over the past several years, the country has been pursuing a balanced approach that prioritizes energy transition, affordability, sustainability, and energy security simultaneously. In May 2026, India’s peak electricity demand crossed 270 GW, a figure that reflects only the demand connected to the national grid and excludes captive power generation. This highlights the rapidly growing electricity requirements of the country and underscores the importance of ensuring long-term energy security.

There is no doubt that India has made remarkable progress in expanding its renewable energy capacity and increasing clean energy generation. The country continues to broaden its renewable energy footprint across all possible sectors and geographies. However, considering the pace at which electricity demand is growing, there is a pressing need to accelerate these efforts further. While significant attention has been devoted to augmenting generation capacity, the broader challenges associated with transmission infrastructure, demand-side management, and the utilization of renewable energy during non-solar hours require equal focus.

India today possesses substantial generation capacity and is well-positioned to achieve its ambitious renewable energy goals. Various policy measures, including mandatory Renewable Purchase Obligations (RPOs), financial incentives, and subsidies for renewable energy developers, have contributed significantly to the growth of the renewable energy sector. However, the expansion of transmission infrastructure has not progressed at the same pace. While renewable energy generation continues to increase, the ability to efficiently evacuate and deliver this power to end consumers remains a critical challenge. Strengthening transmission networks and enhancing grid flexibility will therefore be essential for maximizing the benefits of renewable energy deployment.

Addressing these challenges requires a combination of technological and policy interventions. Solutions such as Battery Energy Storage Systems (BESS), agrivoltaics, Demand Side Management (DSM), Demand Response (DR), Demand Flexibility (DF), and energy efficiency measures can play a crucial role in improving grid reliability and optimizing energy utilization.

Among these solutions, energy storage is likely to be one of the most important enablers of India’s clean energy future. While achieving the target of 500 GW of non-fossil fuel capacity is increasingly feasible, ensuring that this energy is available when required is equally important. Renewable energy generation, particularly solar power, is inherently variable and may not coincide with periods of peak demand. Battery Energy Storage Systems can bridge this gap by storing excess renewable energy generated during off-peak periods and supplying it during high-demand hours.

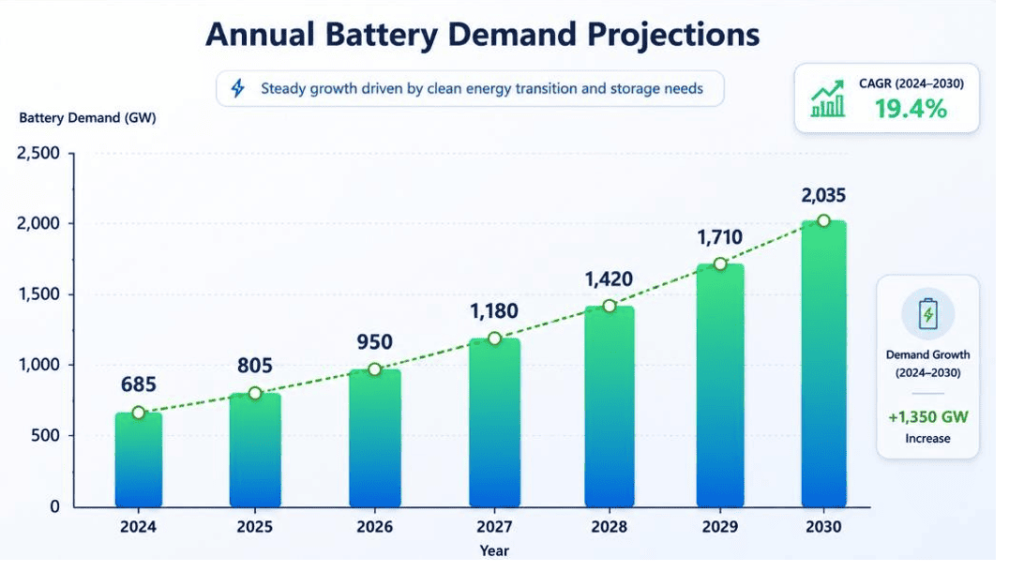

The importance of storage becomes even more evident during peak demand periods when electricity prices tend to rise significantly. In the absence of adequate storage capacity, distribution utilities often have to procure power from electricity markets at substantially higher prices to meet consumer demand. Such purchases increase the overall cost of power procurement and eventually place a financial burden on consumers. Therefore, large-scale deployment of energy storage systems, alongside investments in transmission infrastructure and demand-side solutions, will be critical for ensuring a reliable, affordable, and sustainable power system as India advances towards its long-term energy transition goals. Energy storage systems (ESSs) offer a solution for this intermittency by storing surplus energy during peak production and releasing it when demand increases. Energy storage technologies, especially Battery Energy Storage System (BESS) have shown remarkable technological improvements over the last decade resulting in a sharp decrease in costs. Therefore, BESS is now an integral part of the energy planning framework. As a consequence of this, coupled with the growth of electric vehicles (EVs), demand for batteries is projected to grow over three-fold by 2030.

Lithium-ion: The current dominant technology

Lithium-ion: The current dominant technology

The dominance of LIBs is primarily due to its favourable characteristics, including high energy and power density, higher voltage, higher coulombic efficiency, high cycle life, low self-discharge rates. The technology particularly benefits from its versatility and potential to be deployed across a range of scales, from kW to MW. As a result, it is well suited for use in both EVs and grid-scale storage1. Due to these advantages, coupled with the growing demand for batteries for EVs, global manufacturing capacities for LIBs have grown rapidly in recent years, which in turn has driven down prices significantly. As depicted in the figure below, lithium-ion pack costs have fallen by ~80% between 2013 and 2023, which has helped scale their deployment globally2.

LIBs have been integral to the uptake of BESS over the past decade. However, there are several concerns surrounding the technology and its supply chain Geopolitical Concentration of Material Reserves and Processing Facilities

Lithium is a critical mineral for the global energy transition, particularly for Battery Energy Storage Systems (BESS), and its demand is expected to increase significantly in the coming years. However, lithium reserves and processing capacities are highly concentrated in a few countries. As of 2023, Australia, Chile, and China accounted for nearly 90% of global lithium production, while China alone processed around 60% of the world’s lithium and dominated graphite processing for lithium-ion batteries. This concentration poses supply chain risks arising from geopolitical tensions, natural disasters, trade disruptions, and cost fluctuations. These concerns are expected to intensify as global lithium demand grows from 130 kt in 2022 to an estimated 600–1,300 kt by 2030.

Recognizing these risks, several countries are taking steps to secure critical mineral supply chains. For example, the United Kingdom’s Critical Minerals Strategy, launched in 2022, focuses on strengthening domestic production, diversifying import sources, and promoting the efficient use of critical minerals such as lithium, graphite, cobalt, and nickel. Such initiatives highlight the growing importance of building resilient and diversified supply chains to support the global energy transition.

Comparative Assessment of Sodium-Ion and Lithium-Ion Battery Technologies

| Parameter | Lithium-ion Batteries | Sodium-Ion Batteries | Significance |

| Energy Density (Wh/Kg) | 80 – 300 | 100 – 170 | Applications requiring batteries with compact form factors, such as long-haul EVs, may not be suited for SIBs. |

| Suitable Storage Duration (Hours) | 0 – 6 | 2 – 6 | SIBs are not suited for short storage duration applications such as frequency response. |

| Cycle Life (Number of cycles) | 2,000 –

6,500 |

3,500 –

6,000 |

The comparable cycle life of SIBs makes them well suited for repeated charging and discharging. |

| Round Trip Efficiency (%) | 92 – 97 | 80 – 85 | Lower round trip efficiency means greater energy losses during battery

operations. However, improvements are |

| expected for SIBs with further research and development (RCD). | |||

| Calendar Life (Years) | 10 – 15 | 10 – 15 | Comparable calendar life for SIBs

means they can operate for around the same number of years as LIBs. |

| Depth of Discharge (DoD) (%) | 80 | 100 | 100% DoD is a significant benefit,

allowing SIBs to be transported at 0% charge, improving safety. |

| Self-

discharge Rate (%/Day) |

0.1 | 0.1 | The comparable self-discharge rate makes SIBs equally suited for long-duration storage applications. |

Cost Comparison-

| Battery Technology | Global Unit Cost

($/kWh), Year 2022 |

Global Unit Cost ($/kWh), Year 2030 Projected | LCOS

(INR/kWh), Year 2022 |

LCOS

(INR/kWh), Year 2030 |

| SIB | 77 (£60)

(Cell) |

40 (£31) (Cell) | 5.4 (£0.05)

(India) |

4.3 (£0.04)

(India) |

| LIB | 128 (£101)

(Cell) |

47.8 (£37.8)

(Cell) |

4-hr: 7.0 (£0.06)

(India)10-hr: 5.9 (£0.05) (India) |

4-hr: 4.5 (£0.04)

(India)10-hr: 3.5 (£0.03) (India) |

Recommendations for India

1. Promote Sodium-Ion Batteries (SIBs) for Grid-Scale Storage

- Prioritize SIB deployment in stationery and grid-scale energy storage applications where energy density is less critical and cost, safety, and scalability are more important.

2. Reduce Dependence on Critical Minerals

- Encourage SIB adoption to reduce reliance on imported lithium, cobalt, and other critical minerals, thereby improving India’s energy security and supply-chain resilience.

3. Strengthen Domestic Manufacturing

- Leverage existing lithium-ion battery manufacturing infrastructure for SIB production, enabling faster commercialization and reducing capital investment requirements.

4. Increase RsD Investments

- Support research focused on improving energy density, round-trip efficiency, battery management systems (BMS), advanced materials, and manufacturing processes for sodium-ion batteries.

5. Develop a Domestic SIB Supply Chain

- Establish an indigenous ecosystem for raw materials, components, cell manufacturing, and recycling to reduce import dependency and create a resilient battery value chain.

6. Target Applications Where SIBs Have Comparative Advantage

- Focus on grid balancing, renewable energy integration, resource adequacy, transmission congestion relief, and distribution upgrade deferral rather than long-range EVs and consumer electronics.

7. Create Policy and Financial Incentives

- Extend PLI-like incentives, viability gap funding, and demonstration project support specifically for sodium-ion battery technologies and manufacturing.

8. Support Pilot and Demonstration Projects

- Deploy SIB-based pilot projects with DISCOMs, transmission utilities, and renewable energy developers to validate performance under Indian operating conditions.

9. Establish Standards and Testing Frameworks

- Develop technical standards, safety protocols, certification mechanisms, and performance benchmarks for sodium-ion battery systems.

10. Align SIB Deployment with India’s Growing Storage Demand

- Integrate SIBs into India’s projected battery storage requirement of around 61G GWh by 2030, particularly for the rapidly expanding grid-scale storage segment.

Strategic Recommendation

India should adopt a dual-battery strategy, where Lithium-Ion Batteries continue to serve high-energy-density applications such as long-range EVs, while Sodium-Ion Batteries are promoted for grid-scale energy storage and other stationary applications, thereby enhancing energy security, reducing critical mineral dependence, and lowering storage costs.

About The Author-

Jayant Manohar Joshi is a Senior Analyst at the Power Foundation of India (Ministry of Power, Government of India), where he works on energy transition, climate finance, power sector planning, and policy research. He holds a Master of Technology in Energy Management and has professional experience in energy efficiency, industrial decarbonization, greenhouse gas inventory development, power system modeling, and sustainable energy policy. His areas of expertise include energy storage systems, demand-side management, renewable energy integration, climate finance, and least-cost power system optimization using PLEXOS. He has contributed to several national-level studies on energy efficiency, carbon management, industrial emissions, and power sector planning.

Jayant has been actively involved in developing policy recommendations, conducting impact assessments, supporting regulatory analysis, and advancing India’s clean energy transition through research and stakeholder engagement. His work focuses on building a reliable, affordable, and sustainable energy ecosystem aligned with India’s long-term development and climate goals.

- 1 Why does lithium-ion dominate the battery market today? | Council on Energy, Environment, and Water (CEEW) | June 2021

- 2 Lithium-ion battery pack prices hit record low of $139/kWh | BloombergNEF | November 2023