The Solar Industry is changing so fast that yesterday’s “advanced technology” already feels old today. A few years ago, PERC solar modules were considered the future. Today, the conversation has moved toward TopCon, HJT and Perovskite — three technologies racing to define the next decade of solar power.

But this is not just a technology battle.

It is a battle of manufacturing scale, energy security, cost control, efficiency, policy support and global dominance. Somewhere between laboratories, gigafactories and government policies, the future of solar energy is quietly being rewritten.

And India? India is no longer standing at the sidelines. It is enterning the race and planning to win the Solar Race. The country is rapidly building domestic solar manufacturing capacity under schemes such as ALMM, PLI and DCR, while companies aggressively invest in advanced module and solar cell technologies. From rooftop solar to utility-scale parks, the industry is entering a completely new phase.

The real question now is simple:

Which solar technology will actually dominate the next decade?

The End of the PERC Era

PERC technology was the first technology widely used by the Global Solar Industry but it was cheaper, reliable and easy to manufacture. But solar demand is no longer looking only for affordability. Developers today want higher efficiency, lower degradation, better heat performance and longer and better energy generation.

This is where next-generation N-type technologies enter the picture.

Unlike conventional P-type cells, N-type solar technologies lose less energy, perform better under high temperatures and offer longer operational life. This makes them particularly attractive for countries like India, where harsh climatic conditions often affect panel performance.

Now, the industry’s attention has shifted toward three names:

- TopCon

- HJT

- Perovskite

Each technology carries its own promise. Each comes with its own challenge.

And each could shape the future differently.

TopCon: The Commercial King of Today

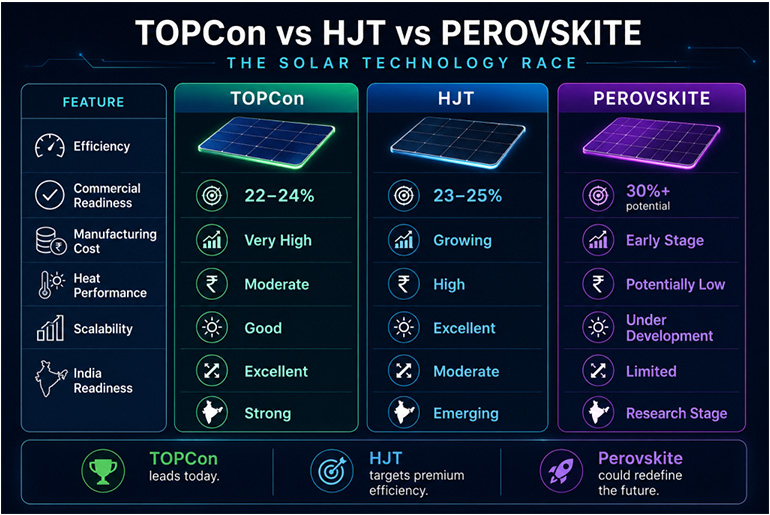

If the solar industry had to choose one technology dominating the current global market, TopCon would probably take the crown.

TopCon, short for Tunnel Oxide Passivated Contact, is essentially an upgraded version of existing silicon solar technology. Instead of completely reinventing manufacturing, it improves efficiency by reducing electron loss inside the cell.

- In simple words, it helps capture more electricity from the same sunlight.

- That single improvement has changed the global manufacturing landscape.

Today, China is aggressively scaling TopCon production, and India is rapidly following the same path. Indian manufacturers including Waaree, Adani, Vikram Solar, Premier Energies and Fujiyama are increasingly focusing on TopCon-based production expansion.

One major reason behind TopCon’s success is practicality.

Manufacturers can upgrade older PERC production lines into TopCon facilities without rebuilding everything from scratch. This lowers capital expenditure and accelerates scalability. For an industry where margins are constantly under pressure, that matters enormously.

Commercial TopCon module efficiencies generally range between 22% and 24%, while laboratory efficiencies are moving closer to 26%. The technology also performs better under high temperatures compared to older PERC modules, making it highly suitable for Indian conditions.

And India’s policy ecosystem is further strengthening this transition.

According to the Ministry of New and Renewable Energy (MNRE), India achieved 100 GW of solar PV module manufacturing capacity under the ALMM framework in 2025 — a massive rise from just 2.3 GW in 2014.

This expansion is not happening accidentally.

It is being pushed by:

- Production Linked Incentive (PLI) schemes

- Basic customs duties

- ALMM regulations

- Domestic Content Requirement (DCR) demand

- PM Surya Ghar rooftop expansion

The upcoming implementation of ALMM-II for solar cells from June 2026 is expected to further increase demand for domestically manufactured solar cells and modules.

For now, TopCon appears to be the industry’s safest and strongest commercial bet.

But there is another challenger waiting quietly.

HJT: The Premium Performer

If TopCon is the practical winner, HJT is the Elite athlete.

HJT, or Heterojunction Technology, combines crystalline silicon with ultra-thin amorphous silicon layers. This reduces energy losses even further and allows the module to achieve exceptionally high efficiency levels.

In the solar industry, efficiency is everything.

Higher efficiency means:

- more electricity generation

- lower land usage

- better long-term output

- improved project economics

This is why HJT has become one of the most discussed premium solar technologies globally.

Commercial HJT module efficiencies are already crossing 23–24%, while global manufacturers continue pushing new records. Reuters recently reported that Trina Solar achieved a record HJT module efficiency of 25.44%, highlighting the growing competitiveness of the technology.

HJT also performs extremely well in high-temperature environments.

For countries like India, where solar modules often operate under intense heat conditions, temperature coefficient becomes critical. HJT modules generally experience lower performance losses under heat, helping maintain stronger power output during peak summer months.

Another major advantage is bifaciality.

HJT modules can capture reflected sunlight from the rear side more effectively, improving overall energy generation. This becomes especially valuable in utility-scale projects, desert installations and reflective rooftop environments.

Yet despite all these advantages, HJT faces one major obstacle:

Cost.

Manufacturing HJT modules is significantly more expensive compared to TopCon. The production process requires advanced equipment, sophisticated engineering and higher silver consumption. Scaling HJT manufacturing profitably remains difficult for many companies.

This is why HJT currently occupies more of a premium-performance segment rather than a mass-market position.

However, if manufacturing costs decline over the next few years, HJT could emerge as a serious competitor to TopCon in high-efficiency markets.

And then comes the technology everyone calls the “future.”

Perovskite: The Solar Industry’s Best Revolution

Perovskite solar technology almost sounds unreal when one looks at its efficiency growth.

In just over a decade, Perovskite solar cells moved from experimental low efficiencies to achieving record-breaking laboratory performance levels. Researchers worldwide now see Perovskite tandem cells (two layered) as one of the biggest breakthroughs in solar history.

Unlike traditional silicon cells, Perovskite uses a completely different crystal structure capable of absorbing sunlight extremely efficiently.

The real excitement comes from tandem technology.

In Perovskite tandem cells, multiple layers capture different wavelengths of sunlight instead of wasting them. This dramatically improves energy conversion efficiency.

Some Perovskite tandem efficiencies are already crossing 30% in laboratory environments, and researchers believe future efficiencies could move even higher.

That changes everything.

Higher efficiency means:

- fewer panels

- lower installation space

- reduced balance-of-system costs

- greater energy generation

Additionally, Perovskite has another revolutionary advantage:

potentially lower manufacturing cost.

Unlike traditional silicon production, Perovskite materials could eventually be printed or coated using simpler manufacturing methods. In theory, this could make solar manufacturing faster and cheaper in the future.

But there is one massive problem.

Perovskite struggles with stability.

Heat, moisture and UV exposure can degrade the material over time. Investors and developers still hesitate because the technology has not yet proven long-term commercial reliability on a large scale.

In other words, Perovskite looks brilliant in laboratories, but the commercial world still wants proof.

For now, the technology remains largely in research, pilot projects and experimental deployment stages.

India’s Manufacturing Race Has Already Begun

India’s solar ambitions are no longer limited to installations alone.

The country is now aggressively focusing on becoming a global manufacturing hub.

According to MNRE data, India’s cumulative solar power capacity crossed 154 GW by March 2026.

Other projections indicate domestic solar demand itself could approach 85 GW annually by FY2030 due to rising deployment across:

- utility-scale solar

- rooftop systems

- green hydrogen

- data centers

- battery storage integration

This explains why Indian companies are rushing toward backward integration.

The industry no longer wants dependence on imported wafers, cells and upstream materials forever. The next phase of competition will depend on who controls the entire value chain — from polysilicon and wafers to modules and advanced solar technologies.

Yet challenges remain serious.

China still dominates more than 80–90% of several global solar supply chain segments, including wafers and polysilicon manufacturing.

India is growing rapidly, but the country still relies heavily on imports for upstream materials and manufacturing equipment.

That dependency could define the next stage of the global solar race.

So, Who Will Win the Next Decade?

The answer is surprisingly layered.

In the short term, TopCon appears unstoppable. It is scalable, commercially mature, relatively affordable and already supported by massive global manufacturing infrastructure. In the medium term, HJT could capture premium high-efficiency markets if manufacturing economics improve and silver consumption declines. And in the long term, Perovskite tandem technology could completely transform the solar industry — but only if stability and large-scale commercialization challenges are solved successfully.

The future may not belong to just one technology.

Instead, the next decade could become a multi-technology era where:

- TopCon dominates volume,

- HJT leads premium performance,

- and Perovskite shapes the future frontier of ultra-high-efficiency solar.

One thing, however, is becoming increasingly clear. The solar industry is no longer merely about generating electricity from sunlight. It is now about manufacturing leadership, technological innovation and energy independence. And India has officially entered that race.