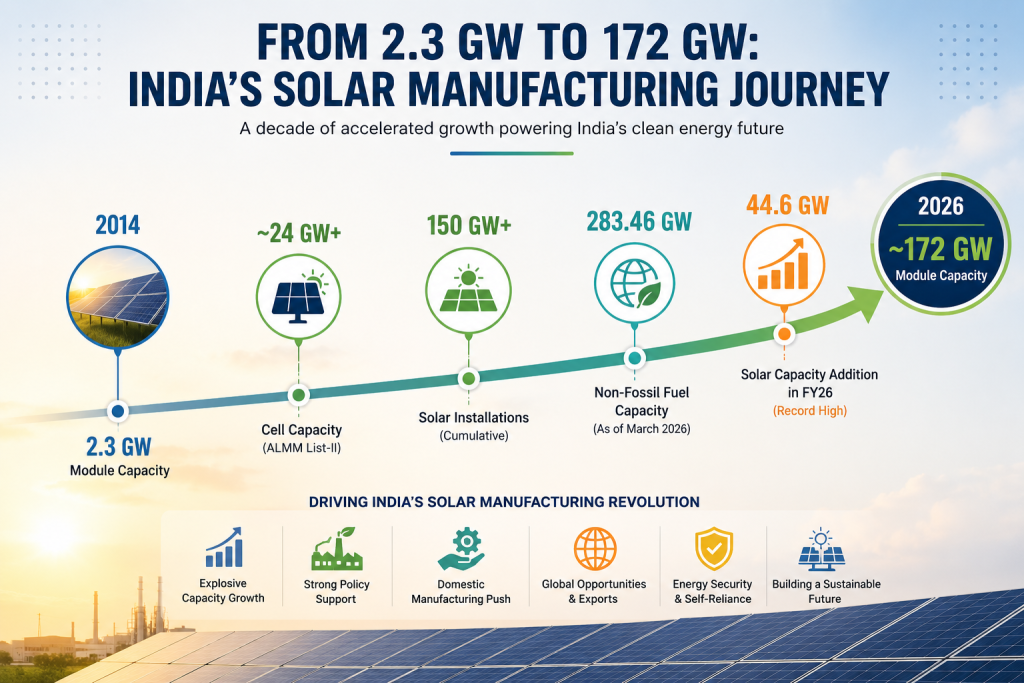

There was a time when India’s solar ambitions were powered largely by imported modules, overseas supply chains, and foreign manufacturing dominance. Today, that equation is changing at extraordinary speed. Backed by the national target of achieving 500 GW of non-fossil fuel energy capacity by 2030, India is rapidly transforming itself into one of the world’s most aggressive solar manufacturing destinations and setting Solar Gigafactories. As of March 2026, the country’s installed non-fossil fuel capacity stood at 283.46 GW, including over 150 GW of solar power capacity, according to official government data.

Across Gujarat, Tamil Nadu, Rajasthan, and Telangana, a new industrial ecosystem is rising — one defined by gigawatt-scale module lines, integrated cell manufacturing facilities, smart inverter plants, and next-generation technologies such as TOPCon and HJT. What began as a renewable energy transition is now evolving into a manufacturing revolution.

In this special feature, we journey inside India’s solar gigafactories and megaplants to explore the companies leading the expansion race, the technologies reshaping the sector, the billions fueling capacity growth, and the challenges that could determine whether India emerges merely as a large solar market — or as a true global manufacturing powerhouse.

Why Manufacturing Became India’s Biggest Solar Story

India’s solar rise was built on a striking contradiction. While the country became one of the world’s fastest-growing renewable energy markets, it remained heavily dependent on imported photovoltaic equipment—especially from China, which dominates the global solar value chain from polysilicon and wafers to cells and modules.

That dependence was exposed during the pandemic. Freight disruptions, container shortages, geopolitical tensions, and volatile raw material prices revealed the fragility of global supply chains. What began as a logistics crisis quickly became a strategic wake-up call. For policymakers and industry leaders alike, the message was clear: India’s energy transition could not continue relying on manufacturing ecosystems beyond its borders.

That realization triggered one of the most aggressive industrial policy interventions seen in the renewable energy sector. Through a combination of the Production Linked Incentive (PLI) scheme for high-efficiency solar PV modules, the Approved List of Models and Manufacturers (ALMM), Basic Customs Duty (BCD), Domestic Content Requirement (DCR) mandates, and import substitution measures, the government fundamentally altered the economics of domestic manufacturing. The objective was no longer limited to accelerating solar deployment — it was about building an end-to-end manufacturing ecosystem capable of supporting long-term energy security.

The scale of transformation since then has been extraordinary.

According to official government data, India’s solar module manufacturing capacity has surged from just 2.3 GW in 2014 to nearly 172 GW as of March 2026. Simultaneously, domestic solar cell manufacturing capacity under ALMM List-II has crossed approximately 24 GW, with multiple integrated giga-scale projects currently under expansion.

The manufacturing boom is also being driven by unprecedented domestic demand growth. India added a record 44.6 GW of solar capacity during FY26 alone, taking cumulative solar installations beyond 150 GW. Renewable energy additions touched nearly 51 GW in FY26 — the highest annual increase in the country’s history.

Several powerful forces are now converging simultaneously:

- Rapid utility-scale solar expansion

- Rooftop solar acceleration under PM Surya Ghar

- Rising storage integration

- ALMM-linked domestic procurement mandates

- Global “China+1” supply-chain diversification

- Export opportunities in the U.S., Middle East, and Europe

- The push for vertically integrated manufacturing ecosystems

India’s solar gigafactories journey is now as much about manufacturing as it is about energy. Solar Gigafactories, backward integration, automation, and AI-powered production are driving a race to localize the entire photovoltaic value chain. However, rapid capacity expansion brings new risks. With manufacturing growth potentially outpacing demand, the future may depend less on scale and more on technological innovation, supply-chain strength, financial resilience, and the ability to compete in global export markets.

Inside India’s Solar Gigafactories

India’s solar manufacturing landscape is rapidly evolving from basic module assembly lines into highly integrated gigafactory ecosystems. Across Gujarat, Tamil Nadu, and Rajasthan, manufacturers are investing in automated facilities equipped with AI-enabled inspection systems, robotic handling, laser cell stringing, and TOPCon-compatible production lines to improve efficiency and reduce defect rates. The focus is increasingly shifting toward backward integration — spanning cells, wafers, modules, glass, and storage systems — to reduce import dependence and improve supply-chain resilience. According to industry estimates, India’s module manufacturing capacity has crossed 170 GW, while integrated giga-scale projects continue to accelerate under PLI-driven expansion and rising export ambitions.

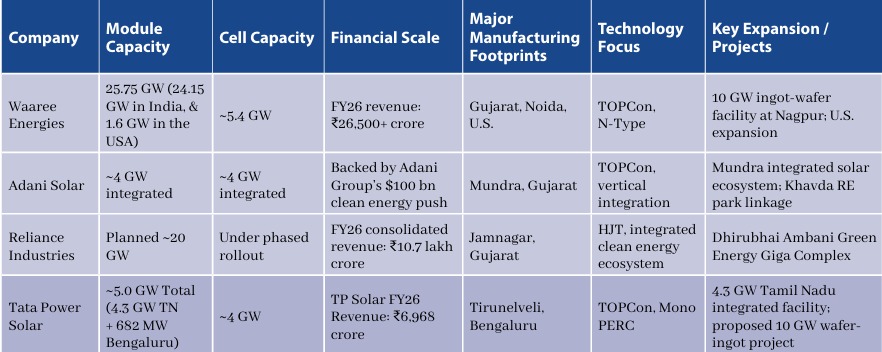

India’s Top 10 Solar Manufacturing Giants

The Companies Building the Industrial Spine of India’s Energy Transition

India’s solar manufacturing race is no longer being measured merely in gigawatts. It is increasingly being defined by integration depth, technology transition, capital strength, export readiness, and the ability to scale from module assembly into fully integrated energy manufacturing ecosystems.

Based on ALMM capacities, company filings, investor presentations, annual reports, manufacturing integration, expansion pipelines, and recent announcements, the following companies currently stand among India’s most influential solar manufacturing players in 2026.

The Technology Shift

Beyond PERC: India’s New Solar Efficiency Race

India’s solar manufacturing ecosystem is rapidly moving beyond conventional PERC technology as manufacturers race toward higher efficiencies, lower degradation rates, and improved long-term energy yields. The transition is now being led by N-type technologies, particularly TOPCon, which has emerged as the dominant technology route globally. According to InfoLink Consulting, TOPCon accounted for nearly 88% of global shipments among leading manufacturers in 2025.

Across India, companies including Waaree Energies, Premier Energies, and Vikram Solar are increasingly aligning new manufacturing lines toward TOPCon and N-type architectures, where commercial efficiencies have already crossed 24–25%.

Key technology shifts now shaping the sector include:

- TOPCon becoming the mainstream utility-scale technology route

- Rapid growth of bifacial modules, expected to capture ~95% market share over the next decade according to ITRPV projections

- HJT gaining traction for superior bifaciality above 90% and lower degradation rates

- Rising industry focus on tandem perovskite-silicon cells capable of pushing efficiencies beyond 30% in the coming decade

- Increasing shift from P-type to N-type manufacturing ecosystems

The technology transition is also intensifying competitive pressure. According to ICRA, only 70–75% of India’s current manufacturing capacity is adaptable to next-generation technologies such as TOPCon and bifacial modules, signaling potential industry consolidation over the next 3–5 years.

In many ways, India’s solar manufacturing battle is no longer only about gigawatt expansion — it is rapidly becoming a race for efficiency leadership.

Industry Voices: Manufacturers Speak on India’s Next Solar Gigafactories Growth Phase

To understand how India’s leading manufacturers are preparing for the next phase of growth, The Battery Magazine spoke with senior industry leaders about capacity expansion, technology transitions, financing strategies, and India’s global competitiveness.

India’s module manufacturing capacity has expanded rapidly in the last two years. What is your roadmap for scaling from current capacity to the next gigawatt milestone, and what key challenges do you foresee in achieving it?

Sohan Lal Agarwal, Founder & MD, Websol Energy System Limited, said, “India’s solar manufacturing sector is witnessing a transformative phase, driven by strong policy support, rising domestic demand, and the global push toward supply chain diversification. At Websol Energy Systems, our roadmap is centred on building a technologically advanced, vertically integrated manufacturing ecosystem that can support both domestic and international markets.

We are focused on scaling our manufacturing capabilities in a phased and sustainable manner, aligned with market demand, technology evolution, and operational efficiencies. Our expansion strategy goes beyond merely adding gigawatt capacity — it is about creating a resilient manufacturing platform with high-quality, high-efficiency products that meet global standards.

One of the key challenges in achieving the next level of expansion remains access to advanced manufacturing equipment, stable raw material supply chains, and maintaining cost competitiveness against global players, particularly China. In addition, infrastructure readiness, skilled workforce availability, and financing costs continue to be important considerations for the industry.

However, we believe India is now at a critical inflection point, and companies that invest early in technology, quality, and integration will be best positioned for long-term growth.”

Amit Barve – CEO – Rayzon Solar Ltd, said, “At RAYZON, scale is not the only objective by itself; running a business profitably and sustainably is the motto. We have already established a strong manufacturing foundation in solar modules and Aluminium extrusion/anodising, and our future roadmap focuses on creating a fully integrated solar manufacturing ecosystem rather than simply adding module capacity.

The next phase of growth is centred on expanding into solar cell manufacturing, which is already at an advanced stage of completion, and further strengthening backward integration with equivalent capacity in ingot casting and wafer slicing. This gives us greater control over quality, cost, and supply chain resilience while reducing dependence on imports.

The biggest challenge today is not building capacity—it is maintaining high utilisation rates and competitiveness in an increasingly crowded market. Capital efficiency, technology selection, skilled manpower, and supply chain localisation will determine who succeeds over the next five years. Manufacturers that can consistently deliver quality, bankability, and cost competitiveness at scale will emerge stronger.”

With global markets increasingly moving toward high-efficiency technologies like TOPCon, HJT, and eventually tandem cells, what technology upgrades are you prioritising to remain globally competitive?

Sohan Lal Agarwal, Founder & MD, Websol Energy System Limited, said, “Technology leadership will be one of the defining factors for future competitiveness in the solar manufacturing industry. Global markets are rapidly transitioning toward higher-efficiency cell architectures, and manufacturers must continuously evolve to remain relevant.

At Websol, we are actively prioritising advanced cell technologies such as TOPCON while evaluating next-generation technologies, including back-contact HJT and tandem structures, to ensure future readiness. Our focus is not only on efficiency gains but also on improving energy yield, reliability, and long-term performance.

We are investing in modern manufacturing processes, automation, and quality-control systems to ensure our products meet international benchmarks. At the same time, we recognise that technology transitions must be commercially sustainable. Therefore, our approach balances innovation with scalability, reliability, and market applicability.The industry is moving toward a phase where efficiency, lower degradation, and lifecycle performance will become critical differentiators, especially in export markets. We intend to remain aligned with these global trends while strengthening our R&D and technology partnerships.”

Amit Barve – CEO – Rayzon Solar Ltd, said, “Our immediate focus remains firmly on TOPCon technology. It has established itself as the global mainstream technology because it offers the right balance of efficiency, reliability, manufacturability, and commercial viability. We continue to invest in process optimisation, higher power outputs, lower degradation rates, and improved module performance through advanced TOPCon manufacturing.

At the same time, we are actively evaluating next-generation technologies, particularly IBC (Interdigitated Back Contact). IBC has significant potential for premium applications where maximum efficiency and superior aesthetics are critical.

As an industry, we often tend to chase every new technology cycle. Our philosophy is different. We adopt technology when it is close to commercially scalable and delivers clear value to customers, not simply because it is new. The goal is to stay ahead of the market while maintaining disciplined capital allocation.”

As manufacturers move toward backward integration and larger integrated facilities, how are you planning to finance the next phase of expansion — through private equity, IPOs, strategic investors, debt financing, or government-linked incentives?

Sohan Lal Agarwal, Founder & MD, Websol Energy System Limited, said, “The scale of investment required for solar manufacturing expansion today is substantial, particularly as the industry moves toward backward integration and advanced technology adoption. We believe a balanced and strategic financing approach is essential for sustainable growth.

At Websol, we are exploring multiple avenues for financing future expansion, including strategic partnerships, institutional investments, debt financing, and government-supported incentive mechanisms. India’s production-linked incentive (PLI) schemes and other policy initiatives have created a strong foundation for manufacturing growth, and such programmes will continue to play a significant role in enabling scale.

At the same time, attracting long-term strategic capital will be equally important, especially for technology upgrades and integrated manufacturing expansion. Investors today are increasingly recognising the long-term potential of renewable energy manufacturing, particularly as global supply chains diversify beyond traditional markets.

Our focus remains on ensuring that expansion is financially disciplined, technologically aligned, and capable of generating long-term value for stakeholders.”

Amit Barve – CEO – Rayzon Solar Ltd, said, “We believe growth should be supported through a combination of internal accruals, strategic debt, government incentives, and access to public markets. Each funding source serves a different purpose, and the objective is to maintain financial discipline while supporting long-term expansion.

India’s solar manufacturing sector is entering a phase where scale, integration, and technology leadership require substantial investments. Companies that maintain strong governance, operational excellence, and financial transparency will naturally attract capital.

For us, financing is not just about raising funds. It is about ensuring that every rupee deployed generates long-term competitive advantage and strengthens our position in the global solar value chain.”

Do you believe India can emerge as a global manufacturing alternative to China in solar equipment, and what policy or ecosystem gaps still need to be addressed to make that happen?

Sohan Lal Agarwal, Founder & MD, Websol Energy System Limited, said, “India certainly has the potential to emerge as a significant global manufacturing hub for solar equipment. The country possesses strong domestic demand, a growing industrial base, supportive policy direction, and increasing investor interest in renewable energy manufacturing.

However, competing with China requires more than capacity expansion alone. China’s dominance has been built over decades through deep supply chain integration, infrastructure readiness, lower financing costs, large-scale manufacturing ecosystems, and strong export competitiveness.

For India to become a credible global alternative, several ecosystem gaps still need to be addressed. These include strengthening upstream manufacturing capabilities, improving access to affordable financing, ensuring stable policy implementation, enhancing logistics and infrastructure, and accelerating skill development for advanced manufacturing technologies.

Additionally, long-term policy consistency will be critical. Manufacturers require visibility and confidence to make large-scale investments in technology and capacity expansion. Encouraging R&D, fostering industry-academia collaboration, and supporting innovation-led manufacturing will also play an important role in building global competitiveness.

We believe India is moving in the right direction. With sustained policy support and ecosystem development, the country can establish itself as a major global player in solar manufacturing over the coming decade.”

Amit Barve – CEO – Rayzon Solar Ltd, said, “Yes, absolutely. India has all the ingredients required to become a major global solar manufacturing hub, large domestic demand, a growing industrial base, supportive policy direction, and entrepreneurial capability.

However, replacing China is not the right benchmark. The objective should be to build India’s own globally competitive manufacturing ecosystem.

To achieve that, three areas require continued focus. First, deeper supply chain localisation across the entire value chain, particularly upstream materials and components. Second, stable long-term policy visibility that enables manufacturers to invest with confidence. Third, continued investment in manufacturing infrastructure, logistics, R&D, and workforce development.

China built its dominance over decades through scale, ecosystem development, and execution. India has made significant progress in a short period of time, but sustained commitment from industry and policymakers will be necessary to build a globally competitive solar manufacturing ecosystem.

The opportunity is real. The question is no longer whether India can become a global manufacturing leader. The focus now should be on how quickly and efficiently we can build the ecosystem to achieve it.”

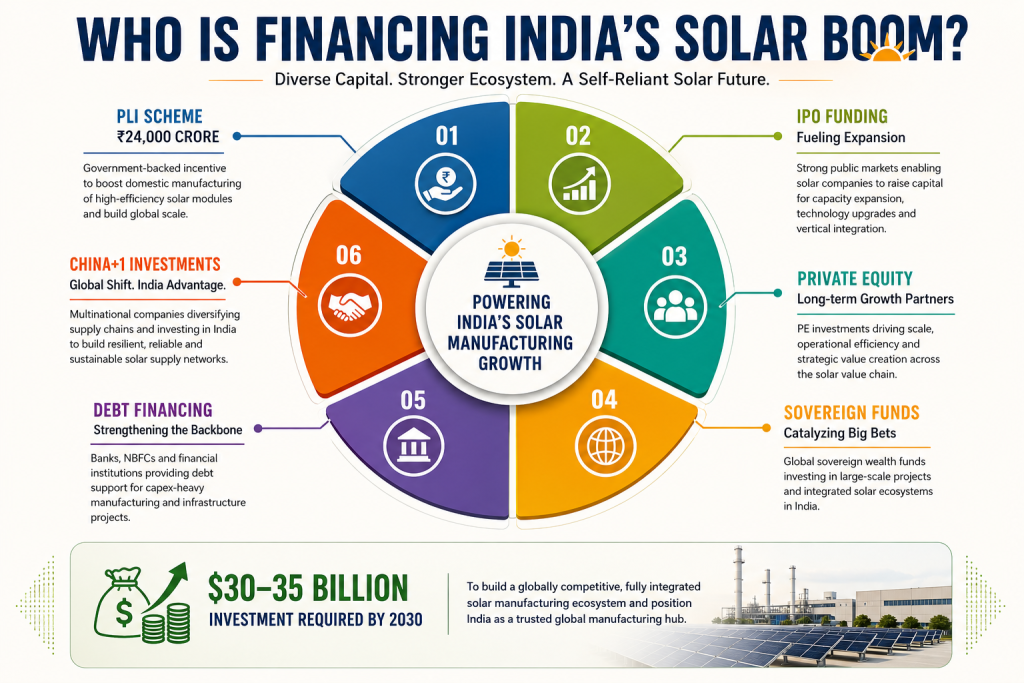

Who Will Finance India’s Solar Gigafactories Ambitions?

A manufacturing gold rush is underway across India’s solar sector, fueled by an unprecedented convergence of government incentives, IPO capital, strategic investments, private equity, and international financing. At the center of this expansion lies the government’s ₹24,000-crore Production Linked Incentive (PLI) scheme, designed to support nearly 48 GW of integrated domestic solar PV manufacturing capacity spanning cells, modules, wafers, and ingots.

Key funding drivers shaping the sector include:

• IPO-led manufacturing expansion

• PE/VC and sovereign-backed clean energy investments

• Debt financing for integrated giga-scale projects

• PLI-linked manufacturing incentives

• Rising international “China+1” capital inflows

Industry estimates suggest India may require over $30–35 billion in solar manufacturing investments by 2030 to build a globally competitive integrated ecosystem.

The Smart Inverter Revolution

The Digital Brain of the Storage Era

India’s solar industry is increasingly shifting beyond panels to the intelligence and power-conversion layer. The solar inverter market, currently valued at nearly $743 million, is projected to reach around $2.62 billion by 2034, growing at a CAGR of almost 15%. Demand is being driven by hybrid, bidirectional, and BESS-ready inverters, alongside AI-powered energy management and smart-grid technologies.

Key trends include the rise of storage-compatible inverters, predictive diagnostics, grid-forming architectures, export-focused compliance, and greater localization of power electronics manufacturing. Supported by domestic production growth and global China+1 sourcing strategies, Indian inverter makers are evolving from hardware suppliers into providers of intelligent, smart-grid-ready energy solutions.

Industry Voices: Building the Next Generation of Smart Inverters

As India targets higher renewable penetration along with storage integration, how do you see inverter manufacturing evolving over the next 3–5 years, and what capacity expansion plans are currently underway?

Raman Bhatia, MD, Servotech Renewable Power System Ltd., said, “The solar and energy storage industries have witnessed exponential growth over the past few years, and we can clearly see this trend reflected in our own sales numbers and customer demand patterns. This growth indicates that India is steadily moving towards a hybrid energy ecosystem where consumers are looking beyond conventional grid-tied solar systems and adopting solutions that combine solar generation, battery storage, and grid connectivity. The appeal is obvious that is hybrid systems offer the flexibility of both on-grid savings and off-grid backup, ensuring energy availability even during outages.

As renewable energy penetration increases, grid stability and reliability will become increasingly important considerations. We are already seeing instances where growing electricity demand is placing additional stress on distribution infrastructure, making energy storage and intelligent power management essential components of the future energy landscape.

This transition is not limited to residential consumers. Industrial and commercial users are also expected to adopt Battery Energy Storage Systems (BESS), decentralized energy architectures, and advanced multi-MPPT inverter technologies to maximize energy generation, improve efficiency, and reduce dependence on the grid.

As a result, inverter manufacturing is poised for significant growth over the next three to five years. Government initiatives such as the PM Surya Ghar Muft Bijli Yojana are accelerating adoption, and while overall inverter production will rise substantially, we anticipate hybrid inverter manufacturing to witness the most significant growth as storage-integrated solar systems become the new industry standard.”

Rajesh Kaushal, VP, BG Head, Power & Energy Solutions at Delta Electronics India, said, “India is at a genuinely exciting inflection point. When you look at where the country was even five years ago — somewhere dependent on imports for critical power electronics — and where it is heading, the transformation is remarkable. India has already crossed 200 GW of installed renewable capacity, and the ambition to reach 500 GW by 2030. It means the pressure on inverter manufacturing is only going to intensify. That is actually a good problem to have.

What we are seeing is that the inverter is no longer just a box that converts DC to AC. It is becoming the brain of the entire solar-plus-storage ecosystem — managing grid signals, optimizing dispatch, responding to fluctuations in real time. This shift from commodity hardware to intelligent control platform is where the next five years will be defined.

From our side at Delta, we are expanding our manufacturing footprint in India and actively working on localizing supply chains for key sub-assemblies. We are not interested in just assembling products here — we want to engineer them here. That means investing in R&D that is designed specifically for Indian grid conditions, not simply adapting a global product.

Our hybrid inverter platforms, which handle both solar and storage in a single integrated system, are a particular area of focus because that is where demand is growing fastest in both utility and commercial-industrial segments.

The PLI scheme has given the sector a meaningful push, and we are seeing the industry respond. But the next phase of growth will depend on how quickly we can build depth — not just capacity — in domestic manufacturing.”

Smart inverters, hybrid systems, AI-enabled energy management, and grid-support functionalities are becoming critical globally. Which next-generation technologies is your company investing in to stay ahead in both domestic and export markets?

Raman Bhatia, MD, Servotech Renewable Power System Ltd., said, “Solar and renewable energy are the future, and we are witnessing significant technological advancements in the sector with each passing day. As the industry moves towards smarter, more resilient energy systems, the role of inverters is evolving far beyond power conversion to become the intelligence hub of the energy ecosystem.

We are currently focused on developing advanced hybrid inverter technologies, intelligent energy management systems, and storage-integrated solutions that can address the growing demand for reliable and efficient renewable energy. We strongly believe that battery energy storage systems will be a key element of the energy transition. Accordingly, we are continuously expanding our lithium battery and energy storage manufacturing capabilities to cater to the rapidly growing market demand.

The opportunities in energy storage are immense, and the need will only increase as renewable energy penetration rises globally. Our R&D team is working continuously on integrating advanced monitoring, energy optimization, and future-ready technologies with existing systems to deliver smarter, more efficient, and scalable solutions for both domestic and international markets.”

Rajesh Kaushal, VP, BG Head, Power & Energy Solutions at Delta Electronics India, said, “Five years ago, grid-support functions like reactive power control, fault ride-through, and voltage regulation were considered premium features. Today, any serious grid operator or project developer expects them as standard. That tells you how fast the bar is moving.

We are actively investing in AI-enabled energy management platforms that can optimise power dispatch in real time — not based on pre-set schedules, but by reading live grid conditions and responding intelligently. For large solar farms and commercial installations, this kind of dynamic control can meaningfully improve yield and reduce curtailment losses.

Hybrid solar-storage systems are another major investment area. As battery storage deployments accelerate in India — and we are already seeing significant momentum, with over 10 GWh of storage capacity being tendered in recent years — the need for inverter platforms that seamlessly manage both generation and storage becomes critical. This is not a future requirement; it is a present one.

Delta’s global R&D network spanning Taiwan, Europe, and the US gives us access to a deep technology pipeline. But we are committed to localizing that pipeline for Indian conditions — grid behaviour, dust and heat profiles, load patterns — because a product built for Germany or California will not automatically perform optimally in Rajasthan or Tamil Nadu.

Remote diagnostics and predictive maintenance are also becoming as important as hardware efficiency. A solar plant that goes offline for days because of a fault that could have been predicted is a real economic problem. Our investment in digital intelligence is aimed directly at solving that.”Global supply-chain diversification is creating opportunities for Indian manufacturers. Which international markets are you targeting for expansion, and what investments are required to position India as a global inverter manufacturing hub?

Raman Bhatia, MD, Servotech Renewable Power System Ltd., said, “Global supply-chain diversification is creating a significant opportunity for Indian manufacturers to establish themselves as reliable alternatives in the renewable energy value chain. We are actively expanding our presence in the Middle East and exploring opportunities across key African markets, where the demand for solar energy, energy storage, and reliable power infrastructure is witnessing strong growth.

To support this expansion, we are investing considerable resources in research and development to better understand the unique requirements of different geographies and develop solutions that are tailored to local grid conditions, regulatory frameworks, and consumer needs. We believe that entering international markets strategically with the right technology and product offerings is critical for long-term success.

For India to emerge as a global inverter manufacturing hub, continued investments in advanced manufacturing capabilities, component localization, R&D, supply-chain resilience, and skill development will be essential. A stronger domestic ecosystem, supported by consistent policy measures and innovation-driven growth, can significantly enhance India’s global competitiveness.

Rajesh Kaushal, VP, BG Head, Power & Energy Solutions at Delta Electronics India, said, “The global shift away from single-source supply chains presents a major opportunity for India, with buyers across Southeast Asia, the Middle East, and Africa actively seeking reliable alternatives to China-manufactured equipment. Delta is strengthening its India operations as part of its long-term Asia-Pacific manufacturing strategy, viewing the country as both a key market and an export hub.However, for India to become a true global manufacturing center, it must move beyond assembly and invest in domestic component ecosystems, engineering talent, and world-class testing and certification infrastructure. While initiatives such as the PLI scheme have created a strong foundation, extending similar support to critical components will be essential for building a globally competitive and self-reliant manufacturing ecosystem.”

Do you believe India can emerge as a global manufacturing alternative to China in solar equipment, and what policy or ecosystem gaps still need to be addressed to make that happen?

Raman Bhatia, MD, Servotech Renewable Power System Ltd., said, “India certainly has the potential to emerge as a strong global manufacturing alternative to China in solar equipment, particularly given its rapidly growing domestic market, improving manufacturing capabilities, and strong policy focus on renewable energy. However, China’s leadership is built on decades of investment in scale, technology, supply-chain integration, and manufacturing efficiency.

While India has made notable progress, challenges remain, including dependence on imported raw materials and components, the need for deeper localization, stronger R&D capabilities, and globally competitive costs. Going forward, consistent policies, greater support for innovation, enhanced export competitiveness, and investments across the entire value chain will be essential. The opportunity is significant, but realizing it will require sustained long-term efforts from both industry and policymakers.”

Rajesh Kaushal, VP, BG Head, Power & Energy Solutions at Delta Electronics India, said, “Yes—but only if India is realistic about what it will take. China’s solar leadership was built over two decades through deep vertical integration, consistent policy support, patient capital, and relentless cost optimization. Simply adding assembly capacity will not be enough.

India, however, has significant advantages, including a large domestic market, strong engineering talent, software expertise, and growing policy support for manufacturing. Initiatives such as the PLI scheme and ALMM framework have laid a strong foundation.

The remaining challenges are strengthening domestic component manufacturing, reducing dependence on imports, upgrading testing and certification infrastructure, and ensuring long-term policy stability. India does not need to replicate China’s model; it needs to build its own path by combining manufacturing scale with engineering excellence. The foundation is in place—now the focus must be on building a complete and globally competitive ecosystem.”

Can India Compete with China?

India’s solar manufacturing expansion is impressive, but China’s dominance remains overwhelming. China controls over 80% of the global solar value chain and operates more than 1.5 TW of integrated manufacturing capacity across polysilicon, wafers, cells, and modules. In comparison, India has reached nearly 144 GW of module capacity and around 35 GW of cell capacity, while wafer and ingot manufacturing remains limited at about 2 GW.

The challenge is not just scale but integration. Chinese manufacturers benefit from highly integrated industrial ecosystems supported by low-cost financing, affordable power, advanced automation, and strong infrastructure. Indian manufacturers continue to rely heavily on imported wafers, polysilicon, and production equipment, while also facing higher financing and logistics costs. Domestic TOPCon modules still cost nearly 37–38% more than Chinese alternatives. However, growing geopolitical tensions, anti-dumping measures, and global China+1 sourcing strategies are creating a significant opportunity for India to emerge as a trusted alternative manufacturing hub, particularly through its expanding N-type and TOPCon ecosystem.

The Next Decade of Solar Manufacturing

From Gigawatts to Geopolitics: India’s Emerging Energy Industrial Age

India’s solar transition is rapidly evolving from a deployment story into an industrial transformation story. Having already crossed the 50% non-fossil fuel capacity milestone ahead of schedule, the country is now positioning itself as a future global manufacturing and export hub for integrated clean energy infrastructure.

The next decade will likely be defined by four major shifts:

• Rapid emergence of India as an export-oriented solar manufacturing base amid global “China+1” diversification

• Convergence of solar, Battery Energy Storage Systems (BESS), smart inverters, and AI-driven grid management

• Evolution of solar gigafactories into integrated energy industrial hubs combining solar, storage, green hydrogen, and power electronics

• Manufacturing-led energy security through localization of critical supply chains

The shift is already visible. India’s solar exports surged sharply in recent years while imports declined amid ALMM-linked localization and Basic Customs Duty (BCD) protections. Simultaneously, giga-scale industrial ecosystems are emerging across Gujarat, Tamil Nadu, Andhra Pradesh, and Rajasthan, where companies are increasingly integrating cells, modules, storage systems, inverters, and advanced power electronics within single manufacturing clusters.

In many ways, the next decade may no longer be decided only by who generates renewable energy — but by who controls the industrial architecture behind it.

And increasingly, India wants to build that architecture itself.