The Battery Industry in India is entering a new era. Earlier the main focus was on cell manufacturing, adoption or Electric Vehicles and Integration of BESS in the recent projects. But one thing where the Country is still lagging and which is the most important ingredient of cell making – the Critical Minerals.

Lithium, cobalt, nickel, graphite, manganese, and rare earth elements have become the backbone of the global battery and clean energy ecosystem. Without these minerals, large-scale battery manufacturing, energy storage systems, EV production, and renewable energy expansion cannot move forward.

For India, this has become both an industrial and strategic issue.

Market Forecast

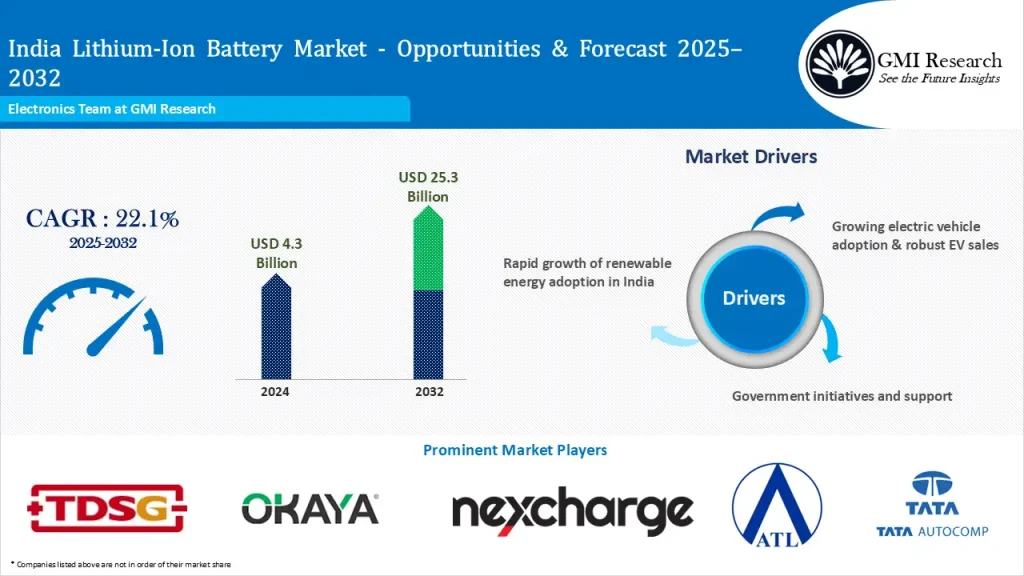

According to GMI Research – the Indian Li-ion market is expected to scale at a rate of 22 % by 2032, and a valuation of $25.3 billion

India is not only aggressively moving ahead with setting Gigafactories, adopting EVs and expanding Renewable Energy storage projects but it is searching for the drawbacks of the growth such as India’s dependence largely on the imports of critical minerals and processed battery minerals. Currently, the global refining and processing market is dominated by China, especially for lithium-ion battery raw materials.

This is exactly why the Government of India has started treating critical minerals as a national priority. Over the last one year, several major policies, recycling incentives, mineral auctions, and processing plans have been introduced to strengthen India’s position in the global battery supply chain.

One of the biggest developments came in January 2025 when the government officially launched the National Critical Mineral Mission (NCMM). The mission is expected to become the foundation of India’s long-term battery raw material strategy.

The Ministry of Mines stated that the mission aims to secure critical mineral supply chains for sectors such as clean energy, mobility, advanced manufacturing, electronics, and strategic technologies. The mission covers exploration, mining, processing, recycling, and overseas acquisition of mineral assets.

Under the mission, the government has approved an expenditure of around ₹16,300 crore, while additional investments from PSUs are also expected during the implementation period till 2030-31. The Geological Survey of India has been assigned nearly 1,200 exploration projects for critical minerals across the country.

This marks a major shift in India’s approach. Earlier, the country focused mainly on importing raw materials and building downstream manufacturing capacity. But now, the strategy is moving toward securing the complete value chain.

The main discussion now a days is revolving around the key mineral’s lithium and cobalt. Lithium ion- battery manufacturing depends on these two key minerals, and as EVs and grid-scale batteries are taking center stage now, the demand of these minerals is expected to increase significantly over the next ten years.

The Ministry of Mines has accelerated auctions of critical mineral blocks in different states. Several blocks containing lithium, graphite, cobalt, vanadium, nickel, and rare earth elements have already been offered for auction over multiple rounds.

Another important development is the government’s push to secure overseas mineral assets. India is talking steps ahead and exploring potential partnerships and collaborations with countries who are mineral-rich to reduce supply risks in the future.

Government-to-government talks over rare earth and critical mineral cooperation have already begun with nations like Brazil and the Dominican Republic.

This global outreach has become necessary because critical minerals are increasingly turning into geopolitical assets. Countries worldwide are competing to secure long-term access to battery raw materials as the energy transition accelerates.

Alongside mining and exploration, battery recycling is also emerging as a major pillar of India’s critical minerals strategy.

In one of the most important recent announcements for the battery industry, the Ministry of Mines completed the eligibility assessment for the Incentive Scheme for Promotion of Critical Mineral Recycling. The scheme has a total outlay of ₹1,500 crore under the National Critical Mineral Mission.

The scheme focuses on recovering critical minerals from lithium-ion batteries, e-waste, and industrial scrap. According to the government, 58 companies have already been approved as eligible participants under the recycling initiative. These companies together represent pledged investments of nearly ₹5,000 crore and a recycling capacity of around 850 KTPA.

This is an important development because battery recycling is no longer being viewed only as a waste management activity. It is now becoming part of India’s raw material security strategy.

As EV adoption increases, end-of-life lithium-ion batteries are expected to become a major source of recoverable lithium, nickel, cobalt, manganese, and graphite.

Recycling could eventually reduce import dependence and support a more circular battery ecosystem.

Another key milestone is that there is a newly opened integrated recycling plant in Uttar Pradesh for Li-ion Batteries and rare earth metals. This plant will be able to recycle 10,000 tonnes of lithium-ion batteries every year as well as process rare earth metals used in making magnets.

Another major trend emerging in India’s critical minerals landscape is the growing focus on processing and refining.

Mining alone cannot solve supply chain dependency. Even if minerals are extracted domestically, they still need to be processed into battery-grade materials before they can be used by cell manufacturers.

Globally, a large portion of lithium refining and critical mineral processing capacity remains concentrated in China. This has exposed several countries to supply chain risks and price volatility.

As part of long-term industrial strategy, India is now taking steps to build its domestic processing capability. The government is reportedly working on incentive mechanisms for lithium and nickel processing infrastructure as it aims to strengthen local refining capacity.

This could become one of the most important opportunities for the battery materials industry over the next few years. If India succeeds in developing refining and precursor material ecosystems, it could significantly strengthen domestic battery manufacturing competitiveness.

Rare earth elements are also becoming increasingly important in this transition.

Electric vehicle motors, wind turbines, electronic devices, aerospace systems, and advanced industrial technologies heavily depend on the rare earth permanent magnet industry. Presently, a large proportion of rare earth magnets are imported to India.

To meet the needs for domestic Rare Earth Permanent Magnet (REPM) manufacturing capabilities, the government approved the establishment of a comprehensive domestic ecosystem for REPM production under a ₹7,280 crore scheme. The implementation of this program will generate 6,000 metric tons per annum (MTPA) of new domestic manufacturing capacity and will create a complete REPM manufacturing value chain from rare earth oxide production to finished good (i.e., magnet) production.

The Union Budget 2026-27 also announced dedicated rare earth corridors in Odisha, Kerala, Andhra Pradesh, and Tamil Nadu to support mining, processing, manufacturing, and research activities.

For the renewable energy and battery sectors, this development is significant because rare earth magnets play a key role in EV drivetrains and wind energy systems. Building domestic capability could reduce future import dependence and support advanced manufacturing growth.

At the same time, India is also exploring the idea of strategic mineral reserves.

Reports suggest that the government is planning a National Critical Mineral Stockpile to safeguard against supply disruptions. Lithium, cobalt, nickel, copper, and rare earth elements are expected to become part of this strategic reserve framework.

This reflects how critical minerals are now being viewed in the same way as energy security assets.

Despite these developments, India still faces several major challenges.

Exploration projects take years before commercial production begins. Before producing commercially from an exploration project, it has to obtain environmental clearance; obtain finance; and have sufficient infrastructure in place to support your mining operation. Due to limited domestic refining capacity in many parts of the world and an ongoing reliance on imports, there is a significant dependency on imports of battery-grade materials.

Another important factor is technology capacity – it requires highly developed refineries and technical knowledge in order to refine battery minerals into high-purity materials. To create this entire ecosystem will take time, along with sufficient funds to be invested in the development of the supply chain, forming global partnerships, along with supportive policies.

Global mineral prices are also highly volatile. Lithium prices witnessed sharp fluctuations over the last few years, showing how quickly market dynamics can change. For battery manufacturers, this creates uncertainty in long-term raw material planning.

Still, the direction of India’s policy approach is becoming increasingly clear.

Critical minerals are no longer being treated only as a mining topic. They are now directly connected to industrial growth, battery manufacturing, renewable energy expansion, energy security, and global supply chain competitiveness.

The next stage of India’s battery growth may depend not only on how many giga factories are built, but also on how effectively the country secures, processes, recycles, and manages critical minerals.

For battery manufacturers, energy storage companies, recyclers, material processors, and renewable energy players, this could open a completely new phase of investment and industrial opportunities over the coming decade. The companies that move early into refining, recycling, processing, and mineral partnerships may eventually become key players in India’s future battery ecosystem.

As the global race for battery raw materials intensifies, India is now trying to build a more secure and self-reliant critical minerals ecosystem — one that supports both the country’s clean energy ambitions and its long-term manufacturing goals.