India enters 2026 at a decisive inflection point in its clean energy journey. Over the past decade, the country has announced some of the world’s most ambitious energy transition goals—500 GW of non-fossil capacity by 2030, leadership in green hydrogen, rapid electrification of transport, domestic battery manufacturing at scale, and a circular economy for critical minerals.

What makes this moment different, however, is not ambition—but evidence.

By the end of 2025, nearly every major ministry shaping India’s energy future has released detailed progress updates through official dashboards, parliamentary replies, scheme disclosures, and press releases. For the first time, India’s energy transition can be assessed not through targets or projections, but through what has actually been delivered on the ground.

This report takes that pause. Drawing exclusively from official government data, it asks three fundamental questions:

- What did India promise?

- What has been delivered so far?

- And where does execution now matter more than policy?

MNRE Scorecard: Renewable Energy Has Delivered—Now the Grid Must Catch Up

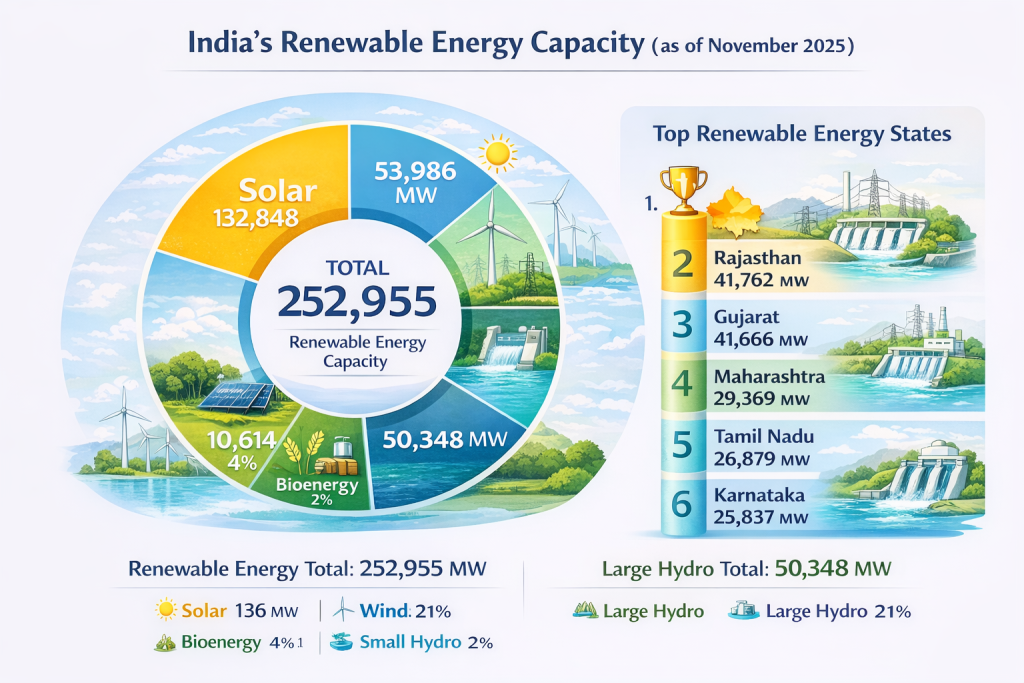

The Ministry of New and Renewable Energy (MNRE) remains the backbone of India’s clean power expansion. As of November 2025, India’s installed renewable energy capacity crossed 250 GW, spanning solar, wind, bioenergy, and small hydro—placing the country among the world’s largest renewable markets.

Solar continues to dominate capacity additions, with installations exceeding 132 GW, driven by large utility-scale projects and accelerating rooftop adoption. Wind power has reached nearly 54 GW, while bioenergy and small hydro play a crucial role in providing regional balancing and rural energy access.

State-wise deployment reveals both leadership and imbalance. Rajasthan, Gujarat, Maharashtra, Tamil Nadu, and Karnataka together account for a significant share of India’s renewable capacity—highlighting strong regional momentum, but also underlining the uneven distribution of clean energy growth across the country.

Yet the nature of the challenge has changed.

India is no longer constrained by its ability to add megawatts. The real test has shifted to integrating megawatts reliably—ensuring grid stability, flexibility, and dispatchability as renewable penetration rises.

Crossing the Non-Fossil Threshold: A Structural Power System Shift

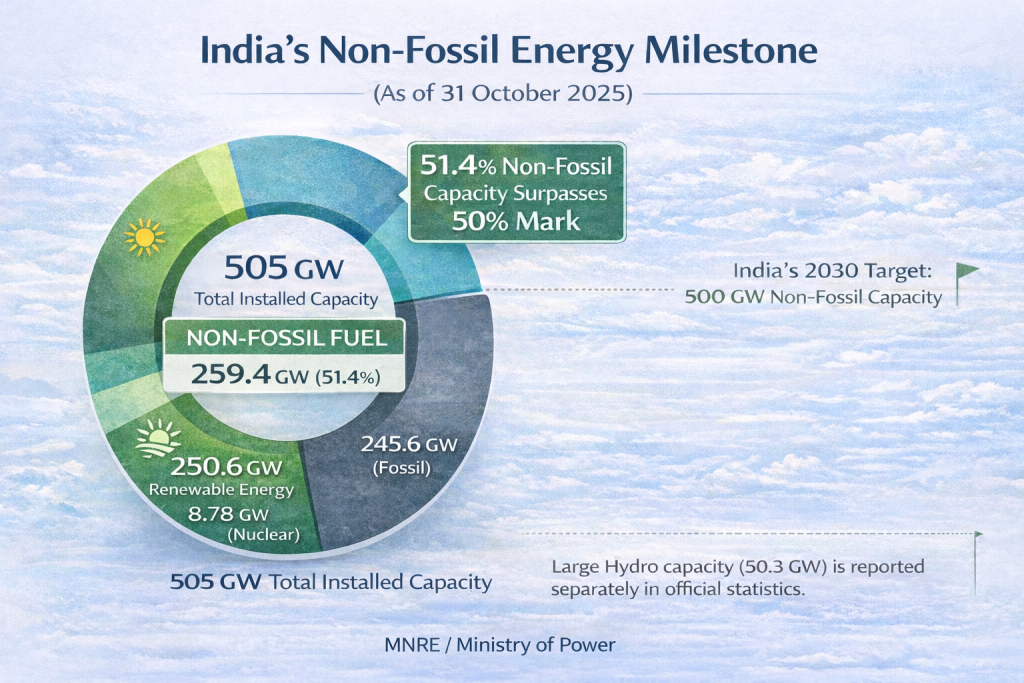

In October 2025, India crossed a symbolic and structural milestone. Total installed electricity capacity reached 505 GW, of which 259.4 GW (51.4%) came from non-fossil fuel sources—renewables, hydro, and nuclear combined.

This achievement came years ahead of India’s stated 2030 target, marking the first time non-fossil capacity surpassed fossil capacity in the national power mix.

But capacity share alone does not guarantee system resilience. The implications of this transition are now being felt most acutely not in generation statistics—but in grid operations.

Green Hydrogen: Policy Architecture Is Ready, Production Is Not

Few sectors capture India’s future energy ambitions as clearly as green hydrogen.

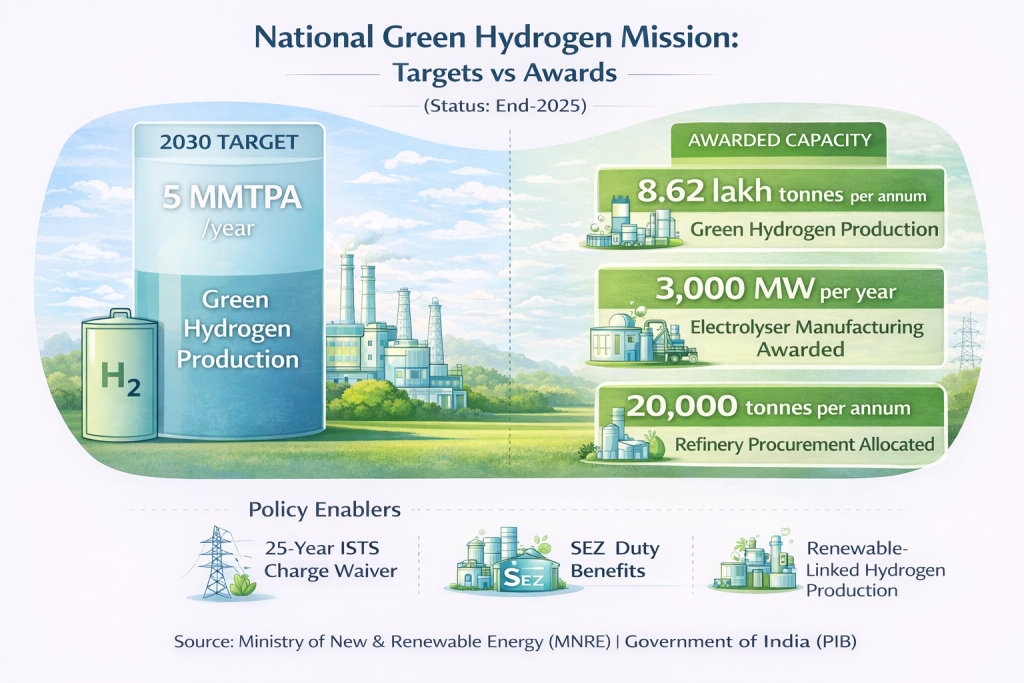

Under the National Green Hydrogen Mission, India has set a target of producing 5 million metric tonnes per annum (MMTPA) of green hydrogen by 2030, positioning itself as a global production and export hub.

By the end of 2025, tangible progress had been made on the policy and allocation front:

- Electrolyser manufacturing incentives were awarded for 3,000 MW per year

- Green hydrogen production capacities totalling over 8.6 lakh tonnes per annum were allocated

- Refinery-linked procurement entered early execution, with 20,000 TPA awarded under a dedicated support scheme

- Long-term enablers—including 25-year ISTS charge exemptions and SEZ duty benefits—were formally notified

These measures establish a robust policy foundation. Yet actual hydrogen production at scale remains nascent. Electrolysers are still being commissioned, offtake contracts are evolving, and renewable-linked hydrogen ecosystems are only beginning to take shape.

For green hydrogen, 2026–27 will be the execution window that determines credibility.

Ministry of Power: Grid Strength Is Rising, Flexibility Is the New Constraint

As renewable penetration accelerates, the Ministry of Power (MoP) has quietly become the anchor of India’s energy transition.

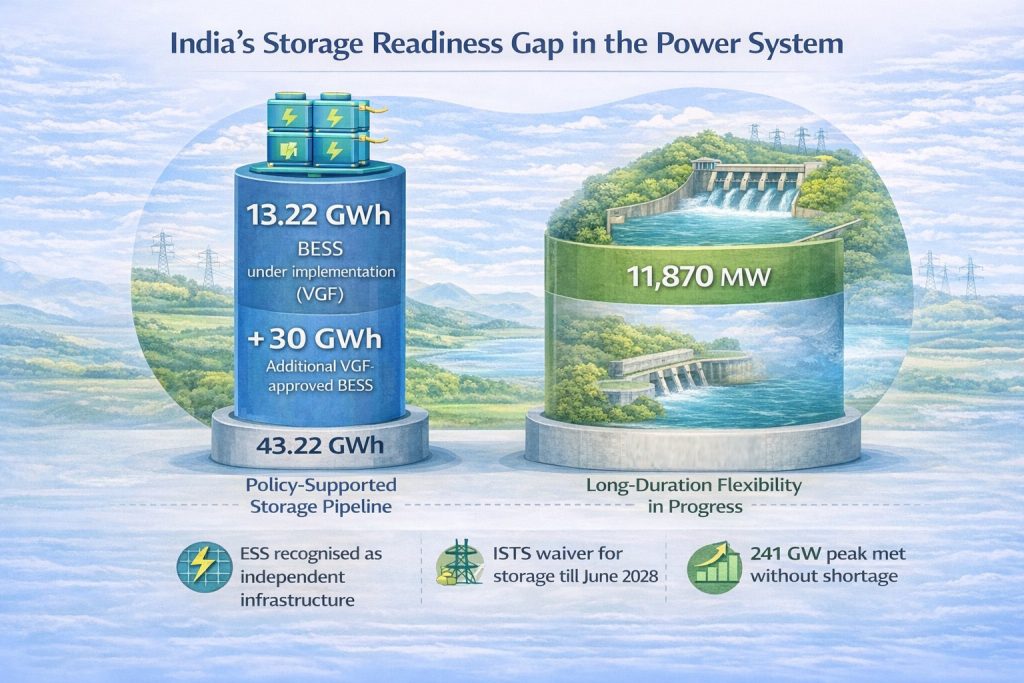

Over the past decade, India’s transmission network has expanded dramatically. Inter-regional transfer capacity has crossed 100 GW, enabling renewable power to flow across regions and helping the grid meet record peak demand—including 241 GW in June 2025 without any power shortage.

Yet variability from solar and wind has exposed a deeper structural challenge: dispatchable flexibility.

Recognising this, the Ministry of Power has taken a decisive step by formally classifying Energy Storage Systems (ESS) as independent infrastructure under electricity rules. This shift is not symbolic—it enables storage to be planned, financed, and deployed as a core grid asset.

Key execution milestones include:

- 13.22 GWh of Battery Energy Storage Systems under implementation through Viability Gap Funding (VGF)

- An additional 30 GWh VGF-backed BESS tranche approved in 2025

- ISTS charge waivers extended till June 2028 to reduce grid-access costs for storage projects

- 11,870 MW of pumped storage projects currently under construction, strengthening long-duration flexibility

Despite this momentum, commissioned storage capacity remains modest compared to announced and tendered volumes—highlighting a growing gap between policy readiness and physical delivery.

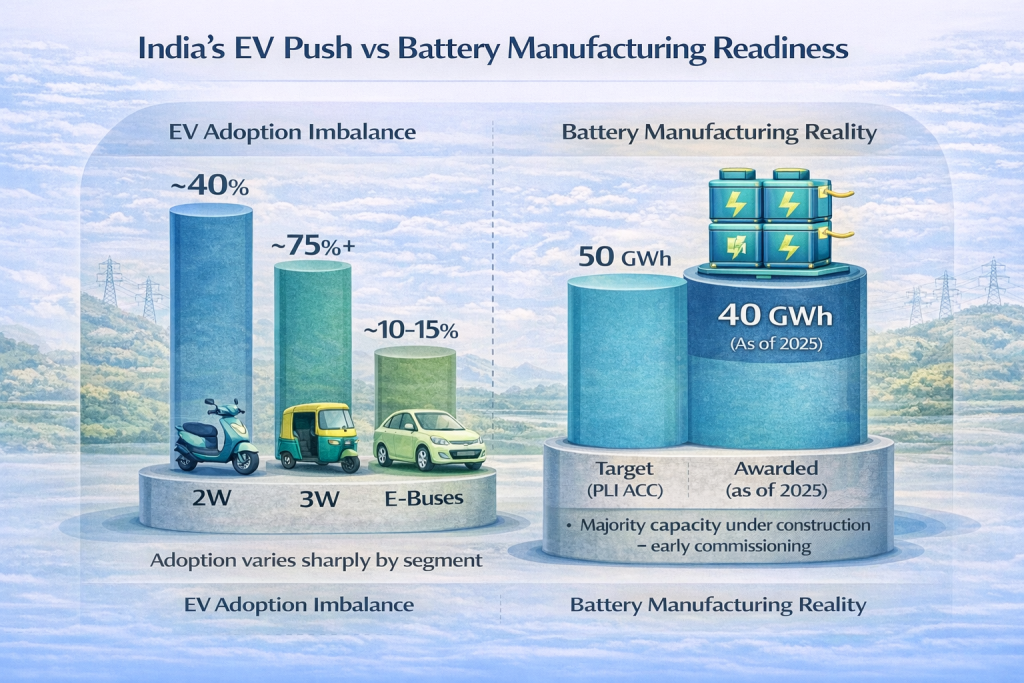

MoHI: EV Growth Is Real—Battery Manufacturing Is the Bottleneck

The Ministry of Heavy Industries (MoHI) sits at the intersection of demand creation and industrial localisation.

Under FAME II, ₹10,000 crore was sanctioned to support electric two-wheelers, three-wheelers, buses, charging infrastructure, and pilot battery-swapping projects. By FY 2024–25, a significant portion of this outlay had already been utilised—driving visible EV uptake, especially in light-mobility segments.

EV adoption, however, remains uneven:

- Electric three-wheelers now dominate new registrations

- Two-wheelers have achieved meaningful penetration

- Passenger electric cars and electric buses continue to scale more slowly, shaped by cost, charging availability, and fleet procurement cycles

On the supply side, the PLI Scheme for Advanced Chemistry Cell (ACC) Battery Storage, with an outlay of ₹18,100 crore, represents India’s largest industrial push in battery manufacturing.

As of early 2025:

- 40 GWh of ACC capacity has been formally awarded under signed programme agreements

- Against a national target of 50 GWh

Crucially, most of this capacity is still under construction or early commissioning. The widening gap between EV demand growth and operational battery output underscores a hard truth: execution speed and supply-chain readiness now matter more than incentives.

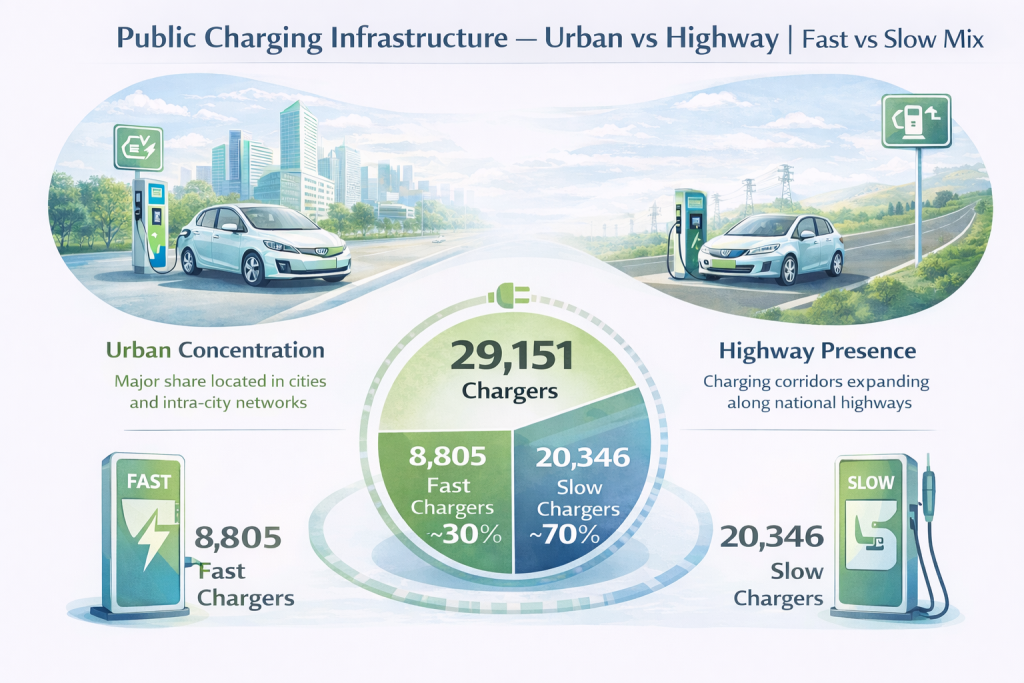

Charging Infrastructure: From Numbers to Reliability

India’s public EV charging network has expanded rapidly, supported jointly by MoHI and the Ministry of Power.

As per official disclosures:

- 29,151 public charging stations have been installed nationwide over the last five years

- Central scheme support includes 479 stations under FAME-I and 9,097 under FAME-II

- Charging has been classified as an unlicensed activity, enabling private deployment

- ₹2,000 crore has been allocated under the PM E-DRIVE Scheme to accelerate rollout

Yet as EV adoption scales, the narrative is shifting. The question is no longer how many chargers exist—but how reliably they function. Uptime, charging speed, grid integration, and payment interoperability are emerging as the true adoption constraints.

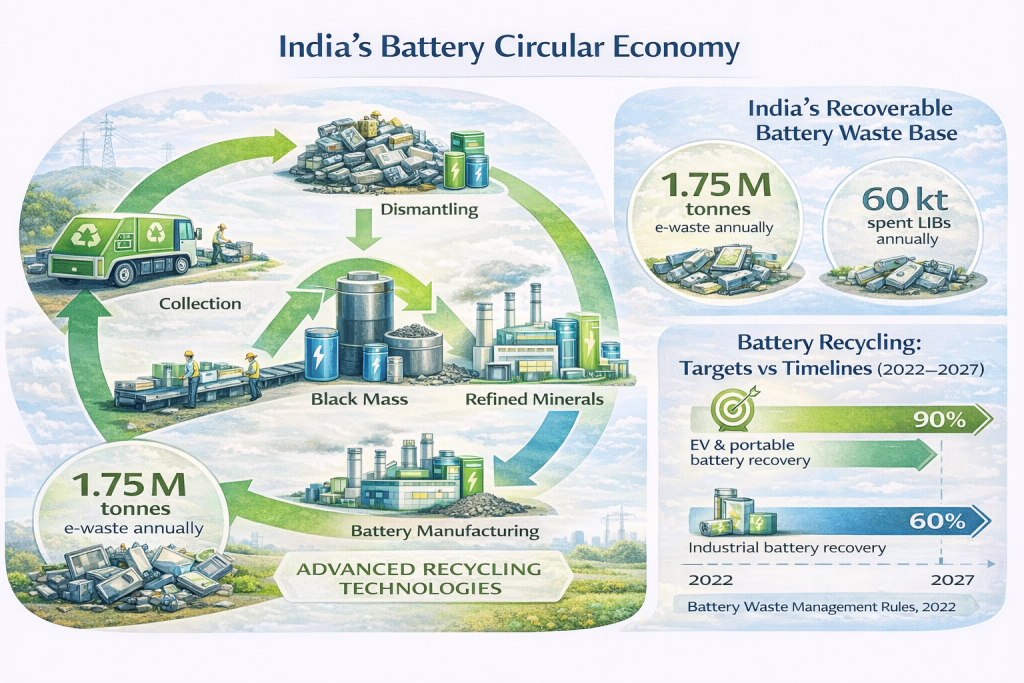

Critical Minerals & Circularity: Strategy Meets Necessity

India’s clean energy transition is increasingly shaped by access to critical minerals—lithium, cobalt, nickel, copper, and rare earth elements.

Recognising this vulnerability, the government has moved decisively toward a circular materials strategy. The ₹1,500 crore Critical Minerals Recycling Incentive Scheme, approved in September 2025, aims to recover up to 40,000 tonnes annually from e-waste, spent batteries, and end-of-life vehicles.

Supporting measures include:

- Battery Waste Management Rules, 2022 mandating up to 90% recovery for EV batteries

- Customs duty exemptions on battery scrap

- NITI Aayog recommendations for recycling-linked PLI frameworks

With 1.75 million tonnes of e-waste and ~60 kilotonnes of spent lithium-ion batteries generated annually, circularity is no longer optional—it is strategic.

Conclusion: The 2026 Execution Test

As India steps into 2026, policy architecture is no longer the constraint. Targets are clear. Incentives are notified. Institutional roles are defined.

What now matters is execution discipline.

The coming phase will test whether:

- Storage scales ahead of renewable volatility

- Battery manufacturing converts approvals into operating capacity

- EV charging prioritises uptime over headline counts

- Circularity frameworks deliver measurable recovery volumes

India’s energy transition has entered its most unforgiving phase—where delivery, not ambition, defines success. The choices made between 2026 and 2030 will determine whether India emerges as a global benchmark for clean-energy execution—or a cautionary tale of momentum outpacing readiness.define the decade ahead.