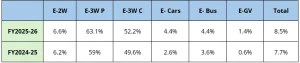

The number of electric vehicles (EVs) registered in India continued to rise in FY2025–26, reaching more than 25 lakh units, a 24% increase from the previous year. EVs made up about 8.5% of all vehicle registrations, up from 7.7% in the previous fiscal year. Even though things are getting better, the market still isn’t close to the government’s long-term goal of having 30% of cars be electric by 2030.

Segment-Wise Growth Trends

Growth across EV segments varied, with each category driven by different factors:

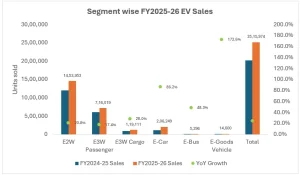

- Electric two-wheelers (E-2W): Continued to dominate the market, accounting for nearly 58% of total EV sales.

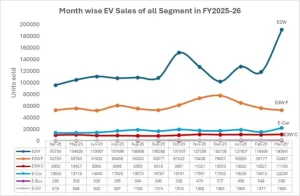

- Electric three-wheelers – Passenger (E-3W P): Reached a peak of 78,057 units in December 2025, supported by mandatory e-rickshaw registrations in West Bengal. Sales declined afterward as PM E-Drive incentives for the L5 category were exhausted.

- Electric three-wheelers – Cargo (E-3W C): Recorded steady growth, driven by total cost of ownership (TCO) advantages for last-mile delivery operations.

- Passenger EVs (E-cars): Emerged as the fastest-growing segment with an 86% year-on-year increase, despite being excluded from PM E-DRIVE purchase incentives, indicating strong organic demand.

- Electric goods vehicles (E-GV): Witnessed a sharp 172% year-on-year growth, with penetration rising to 1.4% from 0.6% in FY2024–25. This was driven by the inclusion of e-trucks under PM E-DRIVE incentives and increasing fleet electrification by logistics and e-commerce companies.

Table 1: % EV Penetration YoY Growth

Key Market Trends

- Legacy OEMs such as TVS Motor, Bajaj Auto, and Hero MotoCorp collectively held 61% of the electric two-wheeler market, supported by strong dealer networks, after-sales service, and brand trust.

- In the passenger EV segment, Tata Motors remained the market leader, though its share declined from around 57% to 39% due to rising competition from JSW MG Motor, Mahindra, and Hyundai.

- New entrants such as VinFast and Maruti Suzuki intensified competition, especially in the ₹12–25 lakh segment, a key category for urban SUV demand.

- Charging infrastructure expanded significantly, with public charging stations exceeding 27,000 by March 2026, improving EV usability for both city and highway travel.

Record-Breaking March 2026

March 2026 recorded the highest-ever monthly EV registrations at 2.8 lakh units. This surge was driven by year-end discounts, anticipation of price increases, and increased fleet procurement. Many buyers also rushed to avail benefits under the PM E-Drive scheme before incentive deadlines.

Outlook for FY2026–27

The strong performance in FY2025–26 gives us a solid base for more growth. By FY2026–27, the number of electric vehicles on the road is expected to be between 9.5% and 10%. Extended PM E-DRIVE deadlines for electric two-wheelers and three-wheelers (L3 category), as well as ongoing improvements in charging infrastructure, domestic manufacturing, financing options, and new product launches, back up this outlook.